Long term Credit rating drops

1 Like

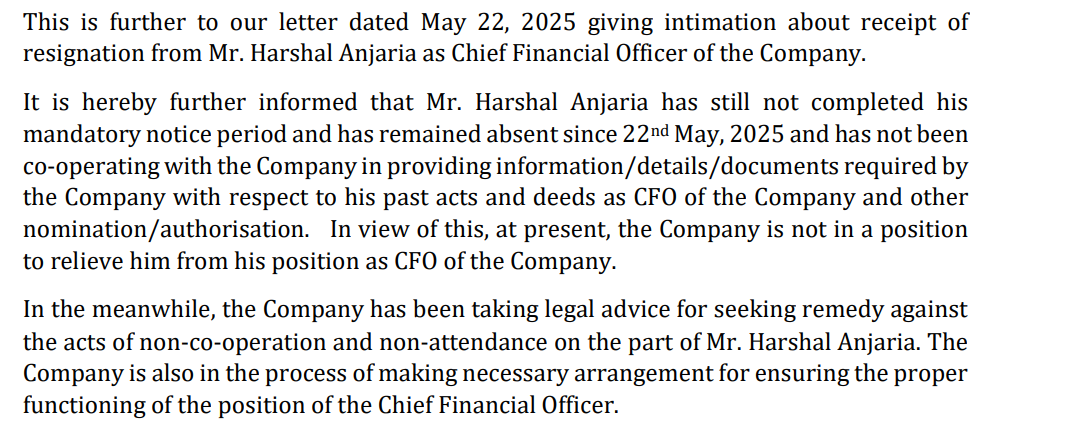

CFO resignation announced; notice period incomplete, cessation date pending company compliance.

Seems fishy. He was active during all IPO discussions along with the ex-CEO.

1 Like

I have the same questions as you do, and don’t know better.

Margins:

- Yes, they have been choppy, and also been under pressure because of the APM allocation and global geopolitical issues

- The long-term contracts they signed with Shell should make the margin less volatile, if not better

- They are adding CBG (compressed bio-gas) to the mix; I guess that should be margin accretive (?)

Valuation:

- I would look at P/B…and if we go by that, it looks to be trading at cheap valuations

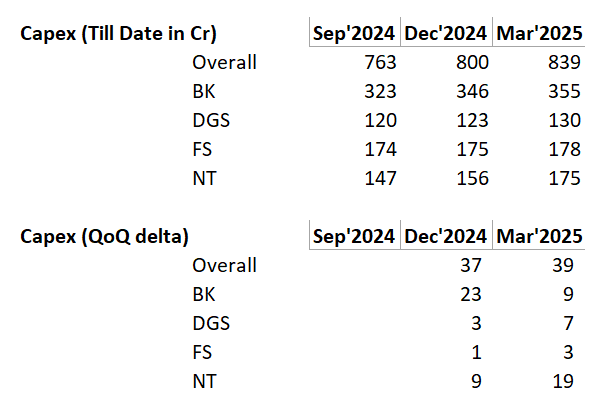

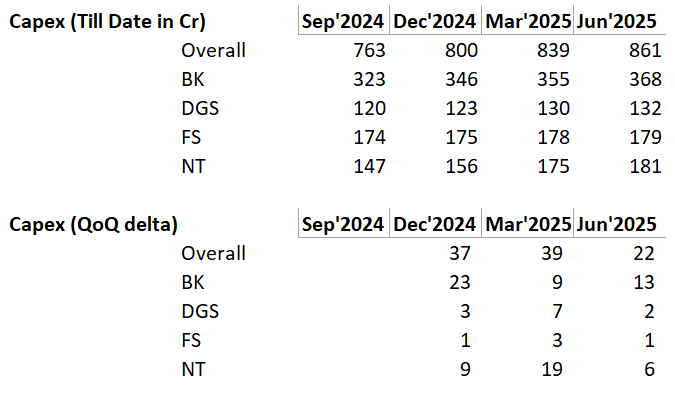

Capex status of NT:

- I have been trying to estimate if they are going as per plan or running behind for NT

- So the total Capex planned for FY25 for NT per DRHP {using both the IPO proceeds + internal accrual} was: ~109/0.8 Cr i.e. 136 Cr {divided by 0.8 because IPO was making up for 80% of what they needed}

- But they actually did a total capex of ~55 Cr in FY25 in NT (see the latest investor presentation)

- Going by above calculations (136 planned vs 55 actual) – they seem to be fumbling and running way behind

- DRHP says they needed 388 Cr for further development of NT (however, some Capex was already done in NT by the time they came for the IPO…and that number cannot be found anywhere).

- Further, they have started reporting Capex spent by GA since the last three quarters…and based on that NT has had a quarterly Capex run rate of 15 Cr (this 15 Cr is not super-unreliable but that’s the best estimate I can think of).

- Further NT has had a Capex of 175 Cr till date (based on the latest investor presentation)

- Going by run rate of 15 Cr per quarter, they should have spent about 90 Cr in NT since the IPO…and they wanted to spend 388 at the start of the IPO

- So, they still need to spend about 300 Cr in NT…and with a quarterly run rate of 15 Cr it will take them another 20 quarter that is 5 more years i.e. end of FY30 to complete NT Capex (three years behind schedule!)

- ^ there are a lot of assumptions in this calculation, and I could be way off the mark…but the sense I get is that they are running behind

4 Likes

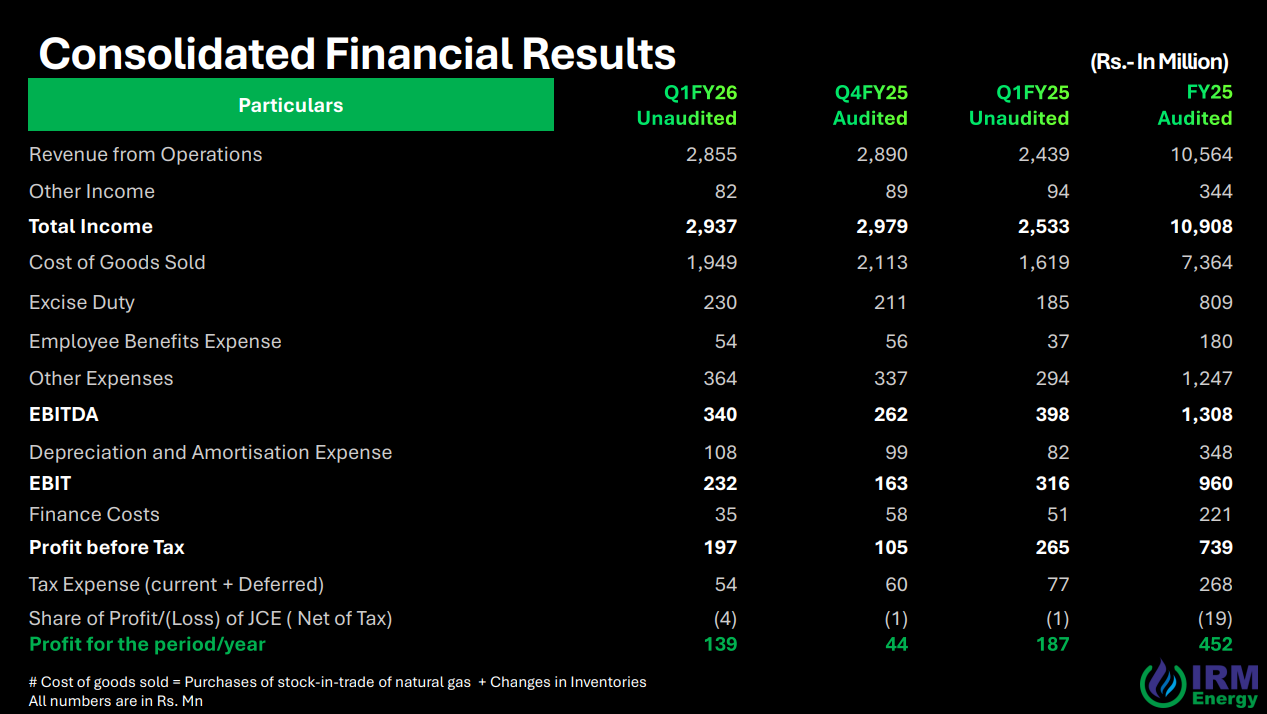

- Good to see some recovery in margins (long-term contracts kicking in this quarter)

- Volume growth muted

- Royalty fee issue persists

5 Likes

Any reason it hit UC today? Nothing I see in the news

HDFC Securities drop

Key takeaways from HDFC Securities latest report on IRM Energy

- CNG segment to drive growth: IRM expects robust volume growth in its CNG business for FY26. The company is confident it will add 50 new CNG stations in FY26.

- Strategic partnership: IRM has partnered with Red Taxi to incentivize cab drivers to switch to CNG in the Tiruchirappalli area.

- EBITDA per unit to increase: The company expects EBITDA per unit to expand to INR 5.25-5.50/scm for FY26, up from INR 4.7/scm in Q1FY26. This is due to the growing share of the higher-margin CNG business and stable crude oil prices.

- PNG segment faces headwinds: The PNG (Piped Natural Gas) business is expected to have slow volume growth as some industrial customers are switching to cheaper alternative fuels like coal.

2 Likes

Found it on X

1 Like

huge volumes can be seen from last few session, stock has made good base after good correction, fundamentally we have check why suddenly market re rated the stock and now PE is 36.

1 Like

Couple of things from the report that do not bode well:

- Royalty fee is going to continue

- FS GA will continue to use alternative fuels like coal

Will be interesting to see the shareholding pattern next month.

Disc.: I exited today with some minor profits.

3 Likes

From the AR notes (Related Party disclosure section):

License Fees Expenses jumps from 36.35 Mn INR to 195.11 Mn INR over 5x, whereas revenue has not grown that much, what gives?

Disc: No holdings, studying

1 Like

It is because License fees was waived off till Dec 23, so FY24 includes just 1 quarter of license fees vs 4 quarters for FY25

1 Like

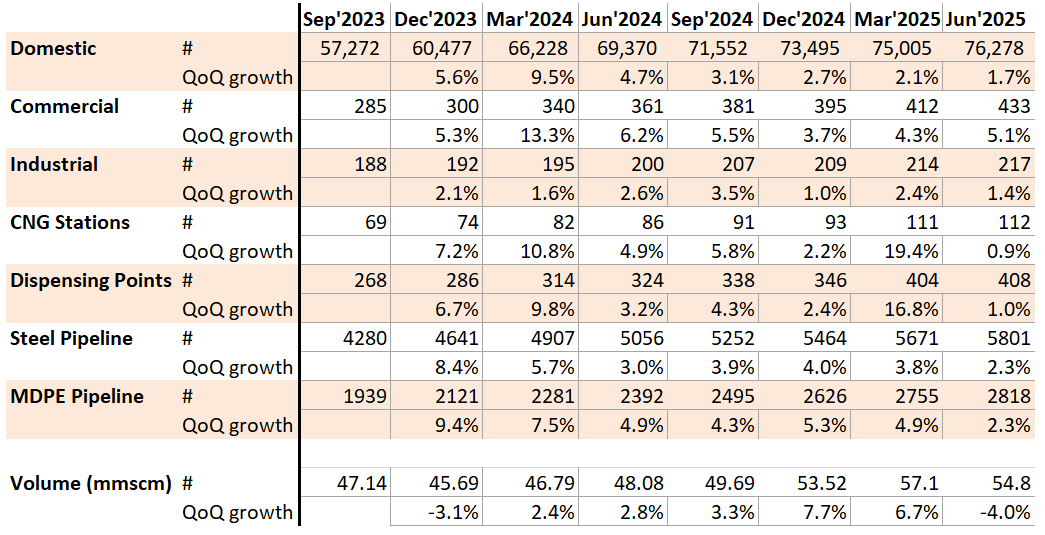

Q3 results are out and margins are better. Added 2,773 domestic customers, 18 commercial customers, 11 CNG stations, and 4 industrial customers

PNG industrial volumes going down and unpaid recoverables from sub is a worry.

Also, hosting investor call after quarterly results first time. Will be fun to tune in!

2 Likes

I had been maintaining this tracker – updated it with the latest info. Good to see continuous capex roll out and the concall.

Disc.: not invested

1 Like

Scheme of amalgamation with Enertech is not value accretive to IRM.

After amalgamation, share price could go down.

1 Like

Why do you say that? What’s the basis?

This is a summary of the IRM Energy Limited Q3 FY2025-26 Earnings Conference Call held on February 5, 2026. The call was led by CEO Mr. MK Sharma and CFO Mr. Arun Kumar Saluru.

Financial Performance Highlights

-

Revenue: Reported at ₹787 crore for the first 9 months of FY26 (11% YoY growth). Q3 revenue was ₹265 crore (6% YoY growth) [04:34].

-

EBITDA: Reached ₹82 crore for the 9-month period (4% YoY growth). Q3 EBITDA was ₹30 crore, representing a 34% YoY increase [04:44].

-

Margins: The company maintained an EBITDA margin of 11.2% in Q3 FY26 [05:16].

-

Balance Sheet: Remains strong with a low term loan of ₹54 crore and a healthy cash/bank balance of over ₹255 crore [06:01].

Operational Segment Updates

-

CNG (Compressed Natural Gas): This is the company’s primary revenue driver, contributing 61% of total operating revenue. It saw a 21% YoY volume growth [06:09].

-

PNG (Piped Natural Gas): Domestic and commercial PNG volumes grew by 25% and 21% respectively. However, industrial sales in the Fatehgarh GA saw a 7% decline due to some steel industries switching back to coal or liquid fuels [07:29].

-

Infrastructure: As of December 2025, the company operates 127 CNG stations and serves over 80,000 domestic customers [03:36]. They plan to cross the 150-station landmark by March 2026 [32:12].

Future Outlook & Strategic Initiatives

-

Capex Plans: The company has an ongoing capex program, having spent ₹103 crore in the first 9 months. They plan to spend approximately ₹250 crore over the next 15–18 months, specifically focusing on the Namakkal and Tiruchirappalli (Tamil Nadu) regions [27:45].

-

Gas Sourcing: Due to declining government APM (Administered Pricing Mechanism) gas allocations, IRM is shifting toward long-term contracts and HPHT (High Pressure High Temperature) gas tenders to maintain margins [20:58].

-

Growth Targets: The management expects a sustainable volume growth of 12–15% annually and aims to improve the EBITDA margin to a range of ₹5.25–₹5.50 per SCM (Standard Cubic Meter) [30:32].

-

Regulatory Support: Management expressed optimism regarding a pending NGT (National Green Tribunal) judgment in Punjab, which could force industries to switch back from coal to natural gas, significantly boosting industrial volumes [41:40].

Key Investor Concerns Addressed

-

Management Stability: The CEO addressed previous management churn, stating the current team is now fully professionalized and cohesive [54:39].

-

License Fees: Clarified that a 2% license fee on gross revenue is still paid to the promoter trust, as disclosed in the IPO [57:03].

-

Joint Ventures: Addressed auditor remarks regarding JVs (Farm Gas, Venuka Polymers), noting that while some provisioning was required due to operational delays, they maintain close control over these investments [01:09:12].

Video URL: https://www.youtube.com/watch?v=eSORH1bCqR4

-

Disc.: ^ Generated using Gemini Pro; hold no position

2 Likes