112560704.pdf (333.8 KB)

HDFC securities maintains a buy after 1QFY25 results.

Disc.: invested

Any information on Enertech Distribution Management Pvt Ltd holding 21% in IRM energy. Are they strategic shareholders? If so, what do they help the company with?

TIA

Disc. Tracking. Not invested

IRM Energy - Notes.pdf (2.7 MB)

Sharing my analysis notes and my thesis on this company. Would love to hear views of expert VPs here.

Thanks, I agree with your thesis

Some points I want to add based on my research

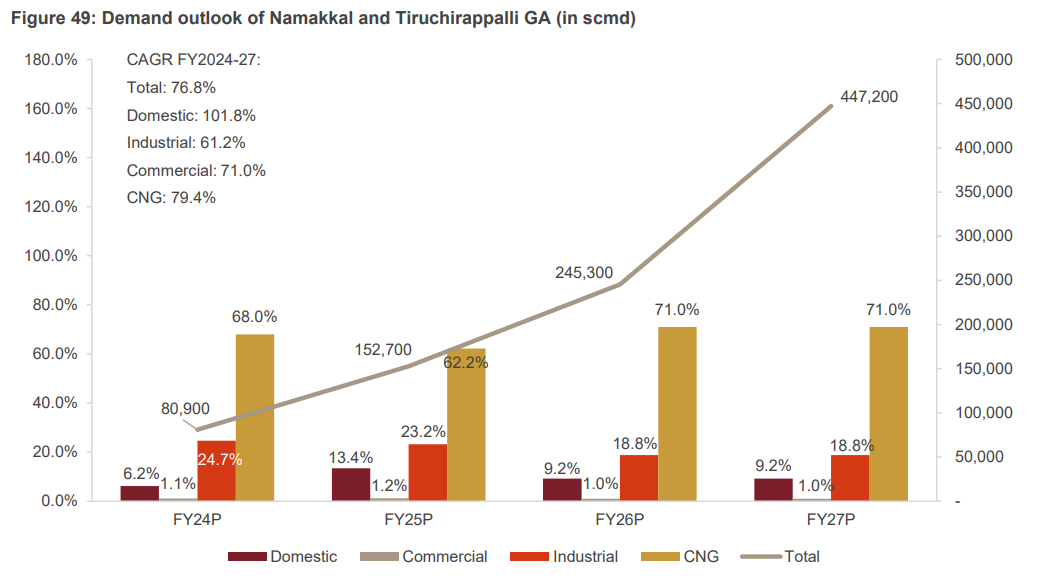

Trichy & Namakkal was the most hotly contested GA in the 11th round. It had the maximum number of bidders at 13, and IRM managed to edge out some heavy weights like Adani Total

I feel the subsidiaries also have a long runway (you can read more about them in the Industry report I shared above)

One piece I worry about is that fact that PNGRB has distributed almost 100% of the GAs…only islands are left. So once these 4 GAs that IRM has mature then where will the next leg of growth come from (there will likely be industry consolidation at that point)

Maheswar Sahu leaving at this point is not a problem I feel – the biggest value that he could have added was getting licenses to operate GAs…so he has done his job (as there are no GAs left on the table)

Enertech Distribution has 21% share in the company – one of the directors (and I guess shareholder) in this company is someone named Shilpa Sahu. I will not be surprised if she is related to Maheswar Sahu. So in an indirect way Maheshwar Sahu will have his skin in the game (I’m just connecting the dots)

If you track the sales of EV vs CNG cars, the latter are doing better in terms of sales…so the anti thesis that EV is going to kill CNG doesn’t hold water

Disc.: invested

Yes this is one of the main concern and applies to whole sector perhaps. Looks like only growth we can factor is be basically growth from existing GAs and not new GA expansion.

Agree with other points - thanks, will take a deeper look at subsidiaries too.

Does this impact irm as well? I guess so…

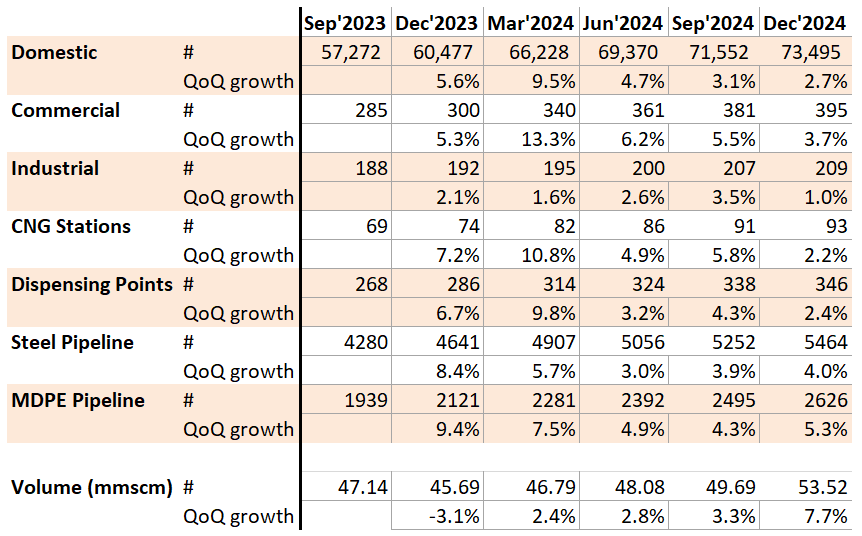

Decent uptick in revenues although profit margins are a concern. And, finally CEO has been appointed - hoping things turnaround with infrastructure developing and new initiatives around CNG vehicles penetration.

Disc : Invested. I have a feeling that this holding will test my patience but could be well rewarding. ![]()

Gas allocation under APM has been reduced by 20% for all CGD. Also promoter continues to suck cash out as royalty charges.

HDFC Sec has reduced the target to 545.

At one pint of time this looked like a very promising play. But promoter action and quitting or Founding chairman and CEO in quick succession changed the story.

IRMEnergy-CompanyUpdate15Nov24-Research.pdf (391.3 KB)

I think we are overindexing on the departure of CEO and the Chairman, and also on the royalty issue.

Positive developments:

Key monitorables:

Disc.: invested; this is not a recommendation, please do your own research

Who is working on behalf of minority shareholders.

Royalty is applicable when there is a contribution by way of Brand, Product or Technology. I see none there. No one will by CNG looking at three letters IRM.

It is not a dispute. It is loot by owner and minority shareholders are at their mercy to reduce the loot.

that is the reason shareholders dumped and makeing lows

Sir, you have a fair point… however (and I don’t know better), if the promoter wanted to siphon off money aren’t there 100 other ways to do it?Why do it so blatantly that it looks like a loot? Can we give them the benefit of doubt here that they did really think that their name is a brand that demands royalty.

This is legal way of siphoning off without getting into trouble.

This was only concern. But reduced domestic gas production and hence declining cheap APM gas allocation has broken the valuation model of CGD. They ought to settle at lower levels just like OMCs where there is 100% import.

This article explains this.

Typical risk of govt policy dependent businesses.

This was already announced - appointed new CEO has joined the firm. (It says for 3 years though)

Am hoping management has regular interactions with shareholders.

I wish IRM energy hosted earning calls for investors! In absence of which we need to speculate a lot of the details.

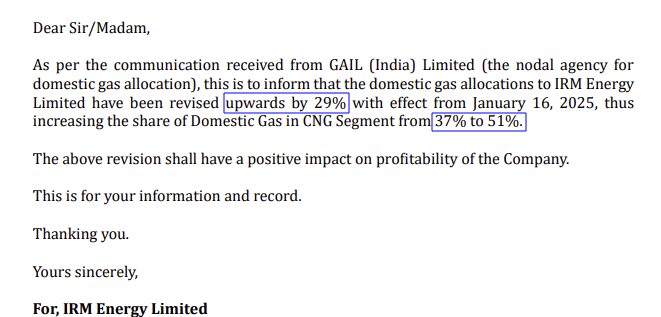

Operationally, can see progress basis in volumes & revenues however profitability seems to be impacted by the allocation - with changes announced in January on APM allocation hoping profitability will improve in upcoming quarters.

Some scuttlebutt based on company posts on Linkedin seems to be encouraging with recent updates. And, new CEO perhaps nudging company towards the milestones.

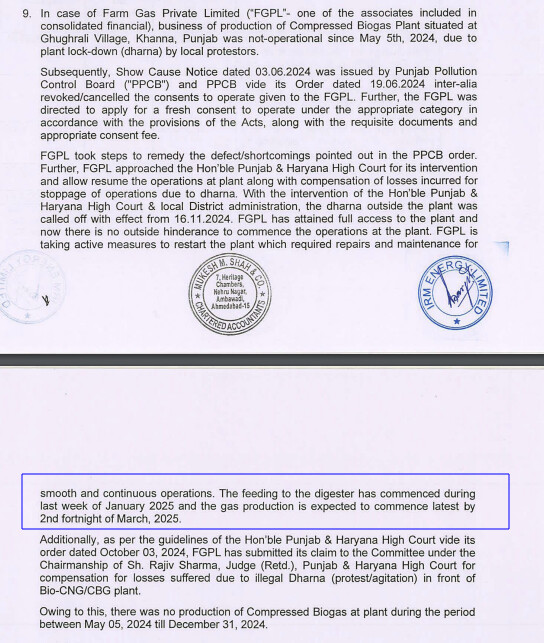

Subsidiary Farm Gas Private Limited issues seems to be resolved (wasn’t aware of this).

Lastly, MIT (Kenneth Andrade) investment in IRM give some validation!

Disc: Invested from higher levels and hoping business turnaround happens and price catches up!