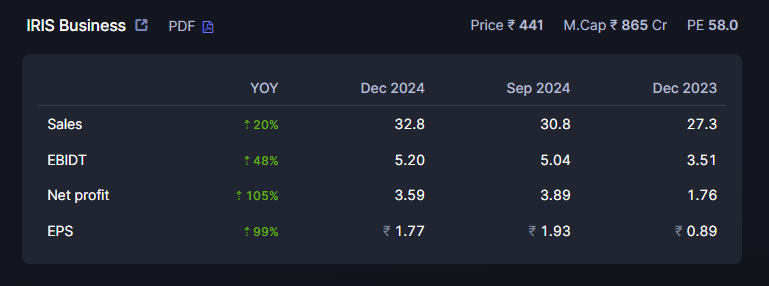

For the first half of FY25, total income grew by 33% year-over-year, with Q2 showing a 30% increase compared to the same quarter last year. This robust revenue growth drove a significant rise in profitability, with profit after tax nearly doubling and profit before tax up by approximately 78%. Despite an equity capital increase from a June-end preferential infusion, return on net worth improved from 21% to 22%. The company’s balance sheet remains strong with cash and cash equivalents totaling ₹31.5 crore as of September 30th.

Segment Performance:

SupTech (formerly Collect): Reported a 48% year-over-year revenue increase, mainly due to the South African Reserve Bank (SARB) contract implementation.

RegTech (Iris Carbon and Iris iDEAL): Achieved approximately 20% growth.

TaxTech: Recently expanded to Malaysia, this segment grew by about 15%.

Geographic Performance: Revenue from Africa now comprises over 36% of total revenue, attributed to the SARB SupTech contract.

Margin Guidance:

While no specific margin guidance was provided, the company benefits from operating leverage, evidenced by a 27% growth in total expenses against a 33% rise in revenue for H1FY25.

Management’s Future Outlook:

Management is optimistic about future growth, supported by strategic investments in sales and marketing. Key growth areas include:

SupTech Expansion: Aiming to capitalize on the demand for standardized regulatory reporting, especially across Africa, with new shared revenue business models.

RegTech: Plans to boost growth by converting clients to enhanced offerings like Disclosure Management and capturing market share from competitors.

TaxTech & DataTech: Although in the early stages, DataTech is viewed as a potential long-term growth driver, with more details to be shared as developments occur.

ESG Reporting: Focus on the Middle East, targeting energy-rich regions where ESG adoption is increasing.

Artificial Intelligence (AI): Exploring AI for productivity and product enhancement, particularly within the Litigation Management System to automate tax notice tasks and leverage case law.

Key Risks:

Competition: Potential intensification in both RegTech and SupTech from established and new players.

SARB Contract Dependency: Any decline in SARB contract revenue could impact financial performance.

New Business Models: Uncertainty surrounds the success of shared revenue models.

AI Implementation: Challenges may arise, and benefits may not meet expectations.

Regulatory Changes: Shifts in regulation could affect product demand.

Demand for SupTech: Increasing as global regulators adopt standardized reporting.

ESG Reporting: Growing adoption of ESG standards opens opportunities, particularly in regions like the Middle East.

AI’s Role: Expected to drive efficiency and enhance product capabilities industry-wide.

Early-Stage Focus: DataTech & TaxTech

The DataTech and TaxTech segments are in the “very, very infant stage,” with limited revenue impact currently. However, management has “high hopes” for DataTech’s potential to contribute to future growth. Specific strategies and details for this segment will be disclosed as the business develops.

Pricing Strategy:

In the RegTech segment, management is implementing pricing enhancements by adopting a consultative sales approach, demonstrating added value, and introducing features that justify premium pricing. An example cited in the concall highlights a customer willing to pay four times the initial rate for an expanded Disclosure Management solution.

Overall, Swaminathan’s tone throughout the call suggests a leader who is confident in the company’s direction, optimistic about its prospects, and committed to transparent communication with investors.

Disclosure: Invested & the above is AI generated transcript

Thanks @Lynch for sharing this . And many thanks for identifying this company too. I invested in this story after reading your detailed post some time last year and it has been quite rewarding.

CEO Mr. Swaminathan passes away. He was a knowledgeable and highly smart individual. This is a loss to the company . Over the time I have been following the company I have been enamoured by his intellect and straight talk in the con calls and investor interactions. I am sure some of the investors in this forum have had the good fortune to interact with Mr. Swami directly.

Absolutely devastated with this news. Mr. Swaminathan was an entrepreneur par excellence, and an individual i developed a deep respect for in interactions with him or hearing him. May he rest in peace and god give strength to family, friends and colleagues at this point. Mr Swami can be proud of the legacy he has left behind, not only in the company he created, but also in the way he was as an individual, incredibly smart, honest and with a wonderful sense of humour. He will be missed greatly.

Remembrance ceremony being hosted in NAVI Mumbai today from 5 to 7 pm. Also being broadcast on YouTube Live in case anyone wishes to join virtually. Link below.

After the unfortunate demise of Mr. Swaminathan, is the whole buisness continuity in question ?

I would like to believe that there are enough good team members to take the company ahead..

@Lynch invite your views here since you have deeply studied this company.

In my humble opinion Iris as a business has a decent MOAT, especially in Suptech. The several projects they have executed and great customer profile gives them vital experience as more of these projects come in. Plus product strengths and growth has already been covered above.

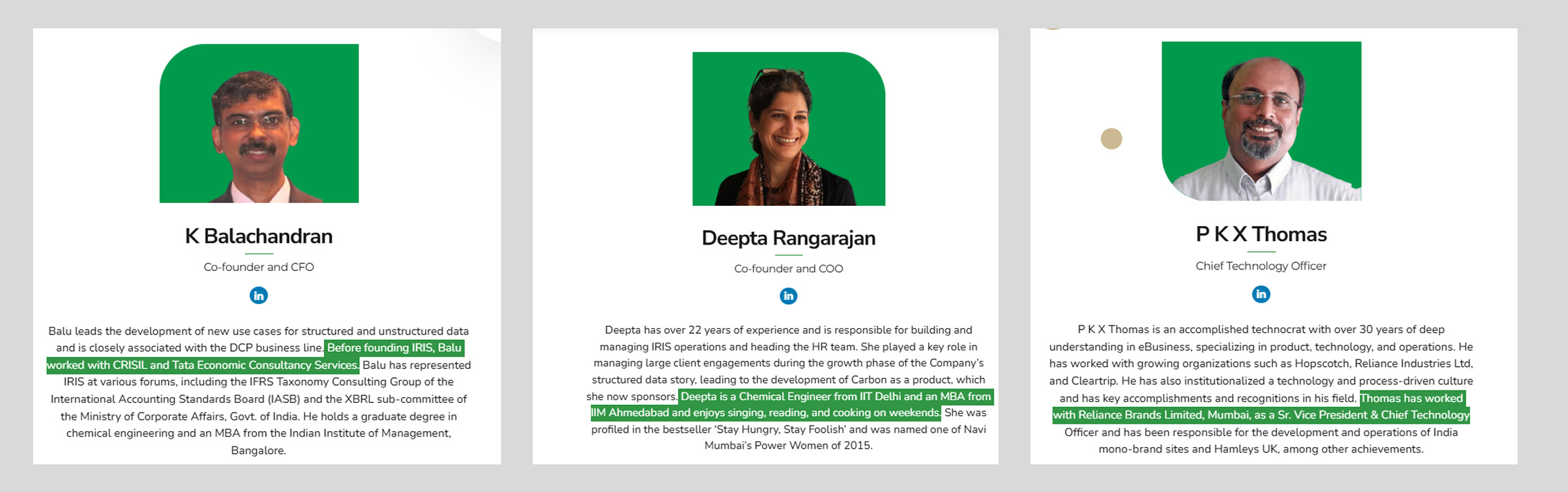

That said, Mr. Swami’s sudden loss is immense. Contracts being long running and the fact that the rest of the leadership team including Mr Balachandran and Ms Deepta all have been with the company since it was founded give comfort on the stability of the business. Whether they can bring in the strategic and leadership skills of Mr Swami is anyone’s guess.

For me, product / SAAS businesses like Iris are rare in the Indian market and they seem to have clean corp governance practices. Just the things said about Mr. Swami in his remembrance ceremony talk about how they built the company with governance and people as key facets. Business wise, I see a lot of demand for such a business in the investment framework if they can continue to grow. Considering the TAM here and the company’s expertise in a niche space, I continue to be positive on the business in the long term. I do expect growth to be lumpy starting this year and this leadership transition to be hard, but am happy to be a long term investor here considering my entry price and potential for this company.

On 18th April company has disclosed to exchanges that it has been selected by Accenture as the successful vendor for

a significant regulatory technology engagement – the XBRL Project.

I believe this is a major validation of expertise and capability.

they had conducted it because their founder and ceo, swaminathan, passed away suddenly. really sad. i loved his energy. they wanted to reassure everyone that the company is stable and moving forward smoothly.

the call took place during a silent period as the full-year audit had commenced. due to this, they couldn’t discuss financial numbers

key updates

iris is stable and in good hands.

all the key business lines (suptech, regtech, taxtech) are still doing well and growing.

experienced leaders are running each division with clear plans in place.

they have a strong sales pipeline and deepening partnerships

q4 and full year results will be announced mid-may after the audit concludes

recent win

they won a big project with the qatar central bank. they are delivering a regulatory data platform through a partnership with accenture.

it’s an 18-month project and it’s in their core expertise.

they didn’t disclose the exact size of the deal but said it’s in line with their previous central banking projects.

leadership transition and ceo appointment

mr. balachandran (co-founder and cfo) is overseeing daily operations on an interim basis.

the three co-founders are committed to carry forward the swami’s vision.

the board is planning to meet in may or early june to discuss and appoint a new ceo.

they’re considering both internal and external options, but they haven’t made the final decision yet.

shareholding

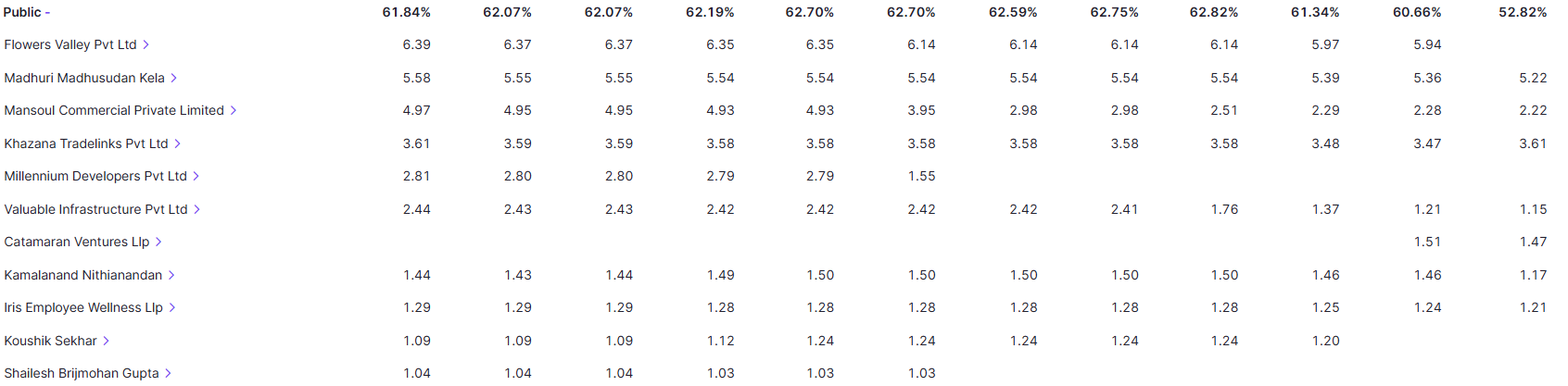

swaminathan’s shares have gone to his spouse deepa rangarajan, who’s also a co-founder, so no change in promoter holding.

a small decline in promoter percentage was because of private placements, warrant conversions, and esop allotments and not because of selling.

future outlook

growth in the next 3-5 years is expected to come from both the established suptech business and the create segment.

their priorities are very clear:

double down on their existing businesses.

improve profitability in three core businesses

build out newer initiatives like the msme lending platforms.

they’ll continue to explore partnerships across their business lines, but they’re not actively planning to sell. they want to build iris as per swami’s vision.

q&a summary

no cancellations of clients after swami’s passing.

product development and tech support are running smoothly under the cto.

update on the create platform’s growth in us and europe will come in the next earnings call.

datatech/msme initiatives are progressing. they’ve already signed up three states (telangana, goa, and karnataka); work is ongoing.

one interesting thing I noticed is that pratithi growth fund (Infosys co-founder Kris Gopalakrishnan’s family office) has increased its stake in IRIS from 1.91% to 3.7%

of course, this isn’t investment advice. Pratithi has invested in hundreds of startups and vc/ private investment firms follow a power law. only a few bets generate most of the returns. still, worth tracking.

What do we think could be great deal for the promoters - getting a new age CEO who might or might not align with company’s vision, getting bought out by a PE company or wait for a few years before making a decision.

There’s too much uncertainty along with selling pressure in this stock.

Iris’s current leadership team is highly qualified, so if the board decides to bring in an external CEO, it’s likely that person will be even more qualified than the existing team

Also the other concern is that during the concall when Deepa Rangarajan was asked if she would be selling the company, she responded with a ‘It Depends’. I am unable to find that transcript right now, any help for the source is really appreciated.

A categorical ‘No’ instead of that response would have alleviated the uncertainty.

Ankit Kanodia Sir from Zen Nivesh has written a really detailed blog on IRIS. For folks researching on the company and need a head start this is a must read.

All credits to Ankit Sir, just sharing from knowledge sharing perspective.

Disc: Invested (reduced position size from 6% to 2%, after sad demise of Mr. Swaminathan Sir.

There has never been any heavy talks of MSME initiatives, they have been clear since day-1 that MSME is very nascent stages

What money have they burnt on vague initiatives, core focus has been to scale Carbon since it’s the primary ARR accretive offering. If you want to see burn, you should look at some of the foreign competitors who spend so much on marketing and ads for a SaaS offering.