This is an interesting company in a field that will continue to grow, though clients will look at regulatory compliance as cost rather than investment that will generate revenue - therefore not easy to replace existing players.

A couple of questions I am trying to get my head around -

What does the depreciation consist of? Is it the cost of product development? It is significant amount.

why is the revenue/employee so low? TCS, a pure play volume service player has nearly double their revenue/employee.

Why is the management so conservative in projecting even a range of growth? They are not even answering questions around industry rate of growth. I am surprised they were not able to raise funds when there was glut in funding post COVID.

Probably due to the upfront cost of developing and launching their SaaS Carbon product, TCS, on the other hand is a service-based company directly marking up x% over their employee salary. Operating leverage should play out here if they’re able to sell the product - basically fixed costs remain the same while sales increase

Look at the con-calls, they have previously given a 20% revenue growth guidance over the next few years, though I feel the company should comfortably beat this (going by the Marketing JD on their careers page). For industry growth, you can look at other global players like Workiva. Not a direct comparison, since Workiva’s portfolio of products is much larger and their pricing is also much higher than IRIS Carbon

Management has repeatedly said the reason for not raising direct funds is because they don’t want to dilute at such a low market cap. Additionally, the management can’t participate in a rights issue due to their low salaries. Look at their credentials, folks from Ivy League, IIM-A working at 45 lpa + bonus. The highest paid employee is their CTO.

Company increased their YoY revenue by 40% compared to their 20% guidance which always looked likely.

Create segment:

Finally the growth has picked up a little bit QoQ growth 14% in Q4 compared to 11% in Q3

Also, we’re starting to see operating leverage kick-in. Margins in Q4 were 28% compared to just 16% in Q3. Looks like all the marketing and partnerships expenses are paying off now

YoY revenue growth is 21% which is my only peeve with the results. This is the segment which is expected to lead us to promised land and I would like to see rapid growth here so that company can capture market share which can convert into annually recurring revenue (ARR)

Collect segment:

Unexpected levels of growth here, sales up ~70% YoY and even margins improved by 100 basis points

It was a milestone Q4 for Iris not only in terms of fantastic results but they crossed 100 Cr revenue for the first time this year. It is not only the growth in top and bottomline for Iris which is impressive, but also the quality of the earnings which comes across clearly from the concall which has been uploaded.

With EBITDA margin being 20%+ this quarter versus typically ~12% earlier, it is evident here how growth is leading to clear operating leverage. Even if the company continues to grow at a slower pace from now on, I believe the recent re rating is only a part of what the company deserves for such a transformation. Differences in valuations versus global and industry peers have already been highlighted earlier, and now, there is the additional element of fast growth in this business.

Whilst tracking this company since my investment in Oct’23, I have been very impressed by the management especially Mr. Swaminathan and Mr. Balachandran. This continues as all initiatives planning including prudent ESOP pool creation and hiring of top management (detailed below) is being delivered on. Additionally, I find it comforting that they are so conservative in their guidance. Results over the last 2 Qs have shown that this they like to underpromise and overdeliver.

Growth is Collect is mandate driven but it is fantastic. In the concall Mr Swami mentioned how still a majority of the world’s regulators (I think 70 countries) still need to adopt XBRL reporting, and this itself is a massive TAM ahead for the company. Additionally very good points were raised on how as they do more countries, they become much faster with specific reporting requirements that need to be built into the product depending on specific regulator requirements, as they have probably done it in another geography before. A large partner that left them in Europe to build their own product has also just joined them back realising the product strength of Iris Carbon.

Growth has also come in for Create this quarter and that is exciting as the SAAS growth trajectory could define a totally different future for an earlier mandate driven business. Even Mr Balakrishnan who is always very conservative to guide on growth showed a certain level of positivity on the concall for next year.

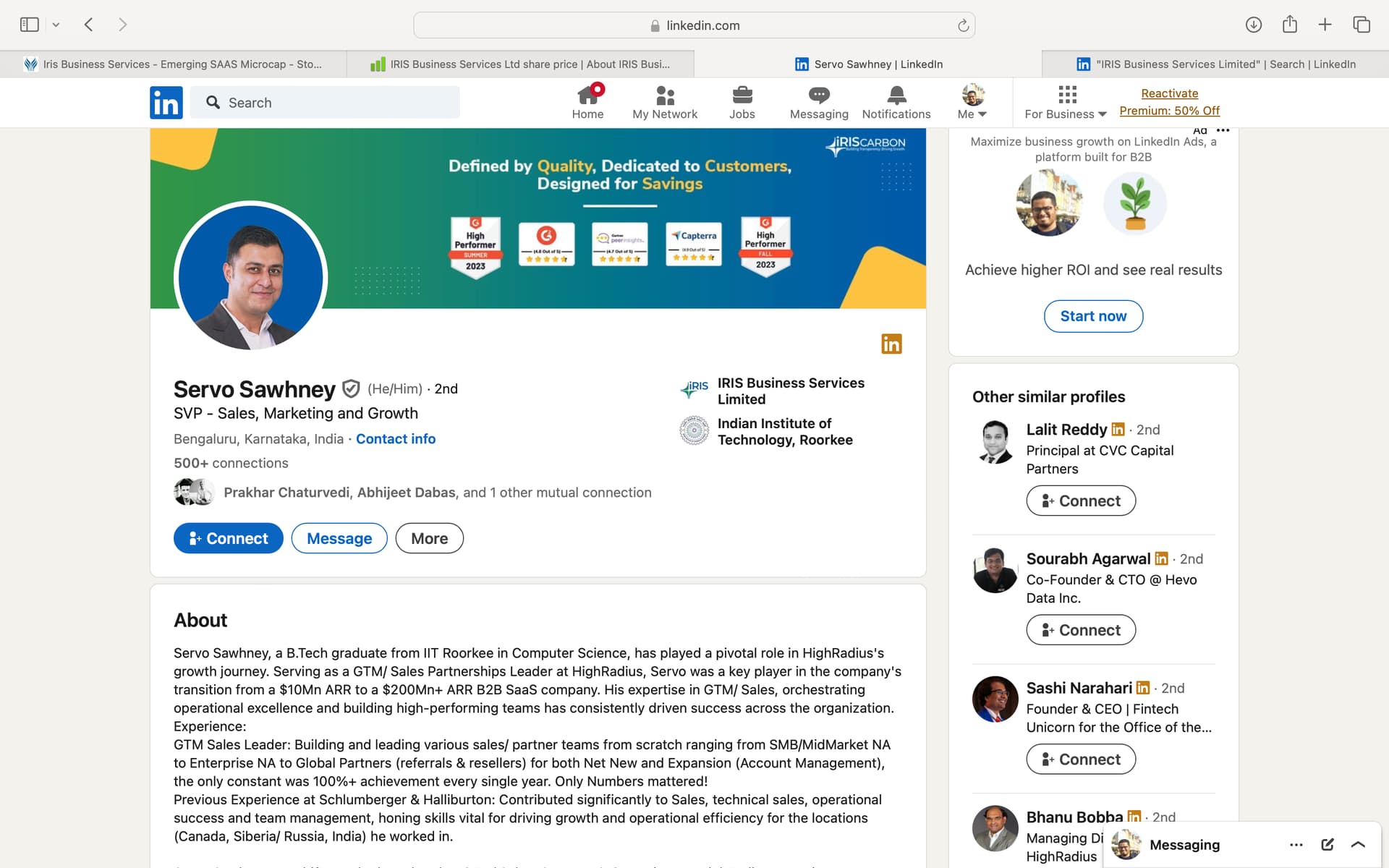

New senior leadership hire in Sales and Growth whose profile on LinkedIn looks impressive as per an initial glance and who was on the concall with some good answers. How he drives the business remains to be seen. Attaching a screenshot of his profile below.

Through the ESOP raising plan the company finally has a decent war chest to attract more leadership talent and expand. As the price has also seen significant appreciation, it finally also gives them headroom to raise capital when they need to as Mr. Swami was earlier rightly not doing so considering he did not feel market valuations at that time were ideal.

Apart from pricing and superior reviews on G2 which are very impressive, they also have a distinction versus Workviva which is they offer integration with MS Office for reporting which the competition does not. I like how the management thinks and differentiates and how they are gradually and surely tapping this niche growing market profitably.

Even at present this is at TTM 4.2x sales and TTM 26x EV/EBITDA for a niche product/SAAS business which has grown topline by 39% and EBITDA by 50% last year. Not as cheap as it was at 2.7x sales in Nov’23, but by no means does this seem crazily valued as well.

Disclosure : I continue to be fully invested in self and family accounts and have topped again slightly again today in family accounts. I am not a SEBI registered advisor and this is not investment advice. My view on the market is mostly to be in safety currently and be very careful at current valuations of several other companies, but considering that I value Iris higher in the long term, this is a rare case where in I continue to add to the investment rather than trimming.

Kris Gopalakrishnan, co founder of Infosys and the man behind Prathithi investments has got hold of 5,43,478 shares at Rs 184/share. Positive development.

Their new customer growth is relatively slow (6% new logos, ~10 new subscription sales from them) but they’re a retention behemoth! 98% GDR is out of this world for a company of their size and showcases the major fact that once you acquire a customer in this segment, they will stick with you.

Even with lower CAC, their operating margins are just ~3%. Look at how much they’re spending on Marketing. This is where Iris can struggle because they don’t have anywhere near the capital to spend on marketing.

Share price on issuance date was ~245 and issuance was done at 184. Not sure how positive a development was the fact that we got diluted at much lower prices. This is a risk due to lower financial capacity of promoters and might happen in future also.

One positive is that the company can now use these funds to fuel its sales as company will be able to attend more conferences and meet more local governments in US, EU, etc. where the money is

In suptech, main competitor is often the regulator developing in-house.

In create segment, many small local competitors globally. Largest global competitor is Workiva, a $600-700 million US-listed company.

Ongoing Projects:

South African contract still has a significant portion to be executed over next 2 years.

Forward-Looking Statements:

Targeting higher growth rates compared to historical performance.

2**. Aim to maintain 35% growth rate going forward.**

Expect to benefit from government initiatives on digitalization and MSME focus in medium term.

Plan to launch marketing campaigns to target replacement market customers.

Internal targets for growth, but not sharing specific projections publicly.

Aspiration to compete with larger global players like Workiva in long-term.

Concerns:

Unpredictability in collect segment due to dependence on regulatory tenders.

Challenge in providing forward projections due to nature of business segments.

Still early stages of market development, especially in developing countries.

Competition from both global players and local competitors in different markets.

Need to improve work-life balance for employees following recent loss of a key colleague.

Consume (data analysis) segment still underfunded and not a current focus for growth investments.

Potential for industry consolidation, with acquisitions happening in Europe and North America.

The management emphasized transparency, timely disclosures, and focus on improving fundamentals as key aspects of shareholder relations. They are cautious about providing specific growth projections due to the nature of their business segments and market dynamics.

Tone of the Promoters:

The promoters, particularly Swaminathan (CEO) and Balu Ganesh Ayyar (CFO), maintained a professional and transparent tone throughout the AGM. They were:

Candid about the company’s strategies and challenges.

Open to answering shareholder questions, even on sensitive topics like dividend policy.

Realistic about the company’s position in the market, acknowledging larger competitors.

Optimistic about future growth prospects while being cautious about making specific projections.

Appreciative of shareholders’ support, especially during challenging times.

Committed to maintaining high governance standards and transparency.

Disclosure: Invested & the above is AI generated transcript

Great set of numbers. Although my one concern remains is that their Create (Regtech) segment growth is still muted. They have hired several senior and junior people in Sales so this number needs to pickup going forwards as a majority of their TAM is in this segment. SupTech TAM and earning potential is limited.

I was a part of the concall yesterday. What is interesting is that Collect (now Suptech) we believe is low TAM, but is actually a very high potential business. It wont have the stability of revenues as the others, but its reasonably long term - i.e. the big South Africa contract is going on since Q2 and is still only half done. The management gave a good rationale for the renaming of these divisions and encouraged searching for the TAMs of the different divisions as per the new names so it is easier to estimate market size now.

Overall, hopefully a long way to go! Happy Diwali everyone.

Disclosure : Continue to be fully invested, biased