Iris Business Services is a company headquartered out of Navi Mumbai, and they define themselves as a RegTech SAAS company. Iris provides technology services/SAAS solutions in the regulatory compliance space.

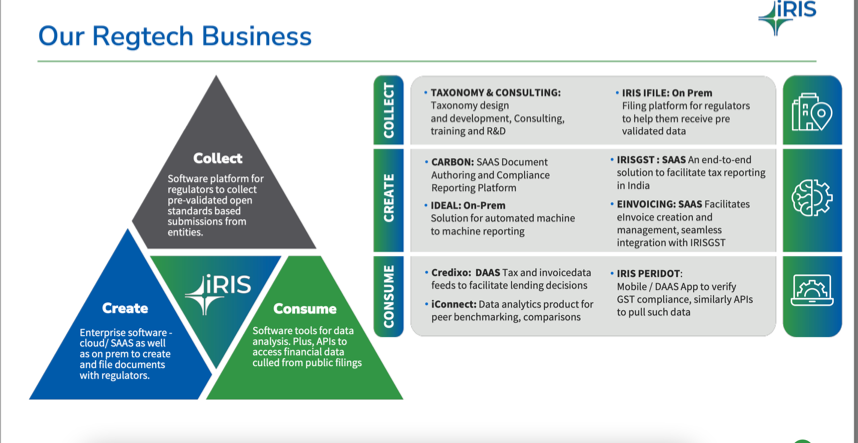

Create is 59% of revenues : Iris Carbon under this vertical is a SaaS software to help companies create & generate their compliance and financial disclosure reports and submission to regulators in XBRL/iXBRL format

Collect is 36% of revenues : Iris iFile provides a software platform for regulators to collect submissions from those that they regulate

Consume (5% of revenues) : Mainly trying to develop software products addressing data analysis as a need

Customer base seems impressive with a large list of marquee clients both in the regulators space and in the enterprise/company filers space

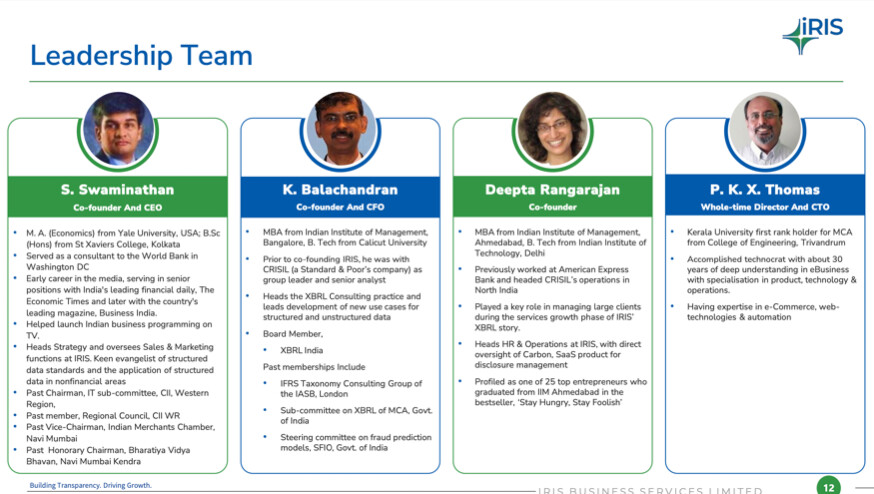

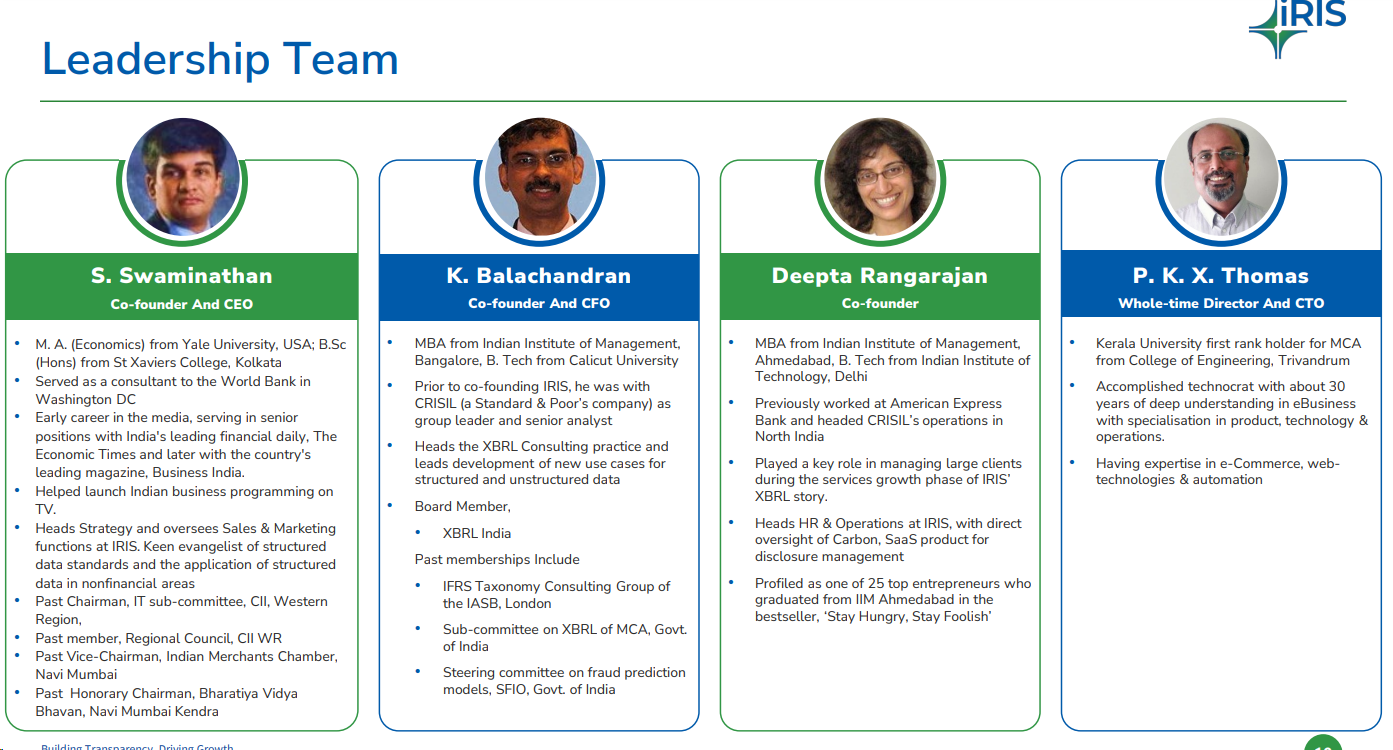

Iris is led by a technocrat team with the 3 co-founders. Credentials of the management are well detailed in the below slide from the latest investor PPT.

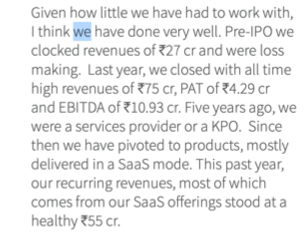

On how the company has transitioned from a services to a SAAS products dominated company:-

On the fast growing RegTech space they operate in:-

My rationale for investing here:-

I have been looking at SAAS companies with interest being already invested in Rategain, and beyond a certain point if these companies can grow then there is a massive amount of operating leverage at play which can bring in disproportionate bottom line growth. With >50% revenue through Create and that also being the faster growth vertical, Iris fit the bill.

They are operating in a market which I expect to grow further given the importance of technology and data in the regtech space and already have proof of concept through marquee clients. Additionally, they seem to be vying for the right growth triggers now, with the focus on Carbon and new products like the enterprise based disclosure management tool mentioned in the last concall. Going forward, increase in scale is expected to be supported by the expansion of Federal Energy Regulatory Commission (FERC) mandate wherein IBSL has the second largest market share and environmental, social and governance (ESG) reporting mandates by regulators across the globe along with increasing interest in various regulators towards XBRL for other regulatory reporting (Source : ICRA credit report Nov’2022)

There are quite a few interviews of the management online + AGMs, and to me they came across as conservative + smart. Employee reviews are reasonably good on Glassdoor.

Valuations were very reasonable versus Rategain (~2.7x sales vs ~9x sales, big gap in other metrics too). Obviously Rategain is a company with a totally different market, but comparisons are limited in the space currently.

Potential Risks:-

Inherent risks of being a microcap investment

Some part of the growth (regulator side) would be mandate driven and hence demand presumably could be lumpy and less predictable

Elongated receivable cycle (Source : Nov’22 ICRA credit report)

Disclosure : I am invested in self and family accounts and am biased. Transactions in the last 30 days. I am not a SEBI registered advisor and this is not investment advice.

Great write up! Business seems interesting but few things are concerning;

They are paying interest of more than 1 Cr on borrowings of 5.3 Crs. Interest rate comes to around 20%. Isn’t that too high ?

Their margins are not stable. They are fluctuating too much. Do we know what the average margin profile of the company is?

Promoter holding which is already low is decreasing even further. It seems like they had some VCs and seed investors who might have cashed out after the IPO.

Thanks @Lynch for bringing this company to the notice . Nice find.

Disc : I have started a tracking position in this company. Not very sure how Large Language AI models might disrupt their business though , since they are into XBRL compliance and automating disclosures .

Adding - Interesting finds from FY23 Annual Report

CEO - Perhaps there are some insights that

investors can glean from Workiva which

is listed on NYSE. For us they are the

company to emulate. The company chalked up revenues of USD 538 million last year but is loss making. I would

recommend to our investors to study

Workiva to appreciate what is possible at

IRIS if we had the resources.

Create Segment - Clients subscribe to our

software to generate their regulatory

submissions. This is our fastest growing

part of our business, the products are

largely delivered as SaaS offerings.

Then there is CRILC, a household name

in the Indian banking system, developed

by us for the RBI. I cannot overstate the

importance of CRILC in transforming

the Indian banking system, rendering

it the strongest it has ever been since

independence

P&L

other Exp 28% of Revenue - 19.5 Cr

Partner Fees 4.4 Cr - need to understand this

bank charges and processing fees towards borrowing facility - 2 Cr

XBRL is used for reporting worldwide because it offers a number of advantages over traditional reporting methods, including:

Accuracy: XBRL data is machine-readable, which means that it can be easily checked for accuracy and completeness. This is important for regulators, investors, and other users of financial information.

Consistency: XBRL reports are consistent in format and structure, regardless of the reporting organization. This makes it easier for users to compare data from different companies and industries.

Efficiency: XBRL reports can be processed and analyzed much more quickly and efficiently than traditional reports. This is because XBRL data can be automatically extracted and aggregated by software applications.

Interoperability: XBRL reports can be easily exchanged between different software systems. This makes it possible for users to access and analyze XBRL data from anywhere in the world.

As a result of these advantages, XBRL has been adopted by regulators and companies in over 100 countries around the world.

Here are some specific examples of how XBRL is being used for reporting worldwide:

The US Securities and Exchange Commission (SEC) requires all public companies in the US to file their financial statements in XBRL format. This helps the SEC to more easily and efficiently monitor the financial health of public companies.

The European Union (EU) has mandated the use of XBRL for reporting by certain types of companies, such as banks and insurance companies. This helps the EU to promote financial transparency and reduce the risk of financial crises.

The International Accounting Standards Board (IASB) has developed a global taxonomy for XBRL reporting. This taxonomy is used by many countries around the world to standardize the reporting of financial information.

In addition to financial reporting, XBRL is also being used for reporting in other areas, such as environmental reporting, sustainability reporting, and risk reporting.

Overall, XBRL is a powerful tool that can be used to improve the accuracy, consistency, efficiency, and interoperability of reporting worldwide.

XBRL, PDF, and Excel are all widely used formats for reporting financial information. However, they have different strengths and weaknesses.

XBRL

Advantages:

Machine-readable data

Consistent format and structure

Efficient processing and analysis

Interoperability

Disadvantages:

Requires specialized software to create and read

Can be complex to implement

PDF

Advantages:

Easy to create and read

Portable and versatile

Can be used to include images, charts, and other multimedia content

Disadvantages:

Not machine-readable

Can be difficult to search and analyze

Not as efficient for processing large amounts of data

Excel

Advantages:

Easy to create and edit

Versatile and powerful

Can be used for complex calculations and analysis

Disadvantages:

Not machine-readable

Can be difficult to share and collaborate on

Not as efficient for processing large amounts of data

Comparison table

Feature

XBRL

PDF

Excel

Machine-readable

Yes

No

No

Consistent format and structure

Yes

Yes

No

Efficient processing and analysis

Yes

No

No

Interoperability

Yes

Yes

No

Easy to create

No

Yes

Yes

Easy to read

No

Yes

Yes

Portable and versatile

Yes

Yes

Yes

Can include images, charts, and other multimedia content

No

Yes

Yes

Can be used for complex calculations and analysis

Yes

Yes

Yes

Easy to share and collaborate on

No

Yes

Yes

Efficient for processing large amounts of data

Yes

No

No

drive_spreadsheetExport to Sheets

Advantages of XBRL

Accuracy: XBRL data is machine-readable, which means that it can be easily checked for accuracy and completeness. This is important for regulators, investors, and other users of financial information.

Consistency: XBRL reports are consistent in format and structure, regardless of the reporting organization. This makes it easier for users to compare data from different companies and industries.

Efficiency: XBRL reports can be processed and analyzed much more quickly and efficiently than traditional reports. This is because XBRL data can be automatically extracted and aggregated by software applications.

Interoperability: XBRL reports can be easily exchanged between different software systems. This makes it possible for users to access and analyze XBRL data from anywhere in the world.

Conclusion

XBRL offers a number of advantages over PDF and Excel for reporting financial information. It is more accurate, consistent, efficient, and interoperable. However, it is important to note that XBRL requires specialized software to create and read.

Which format is best for a particular reporting need will depend on the specific requirements of the users. For example, if users need to be able to easily share and collaborate on reports, then PDF or Excel may be a better choice. However, if users need to be able to process and analyze large amounts of data quickly and efficiently, then XBRL may be a better choice.

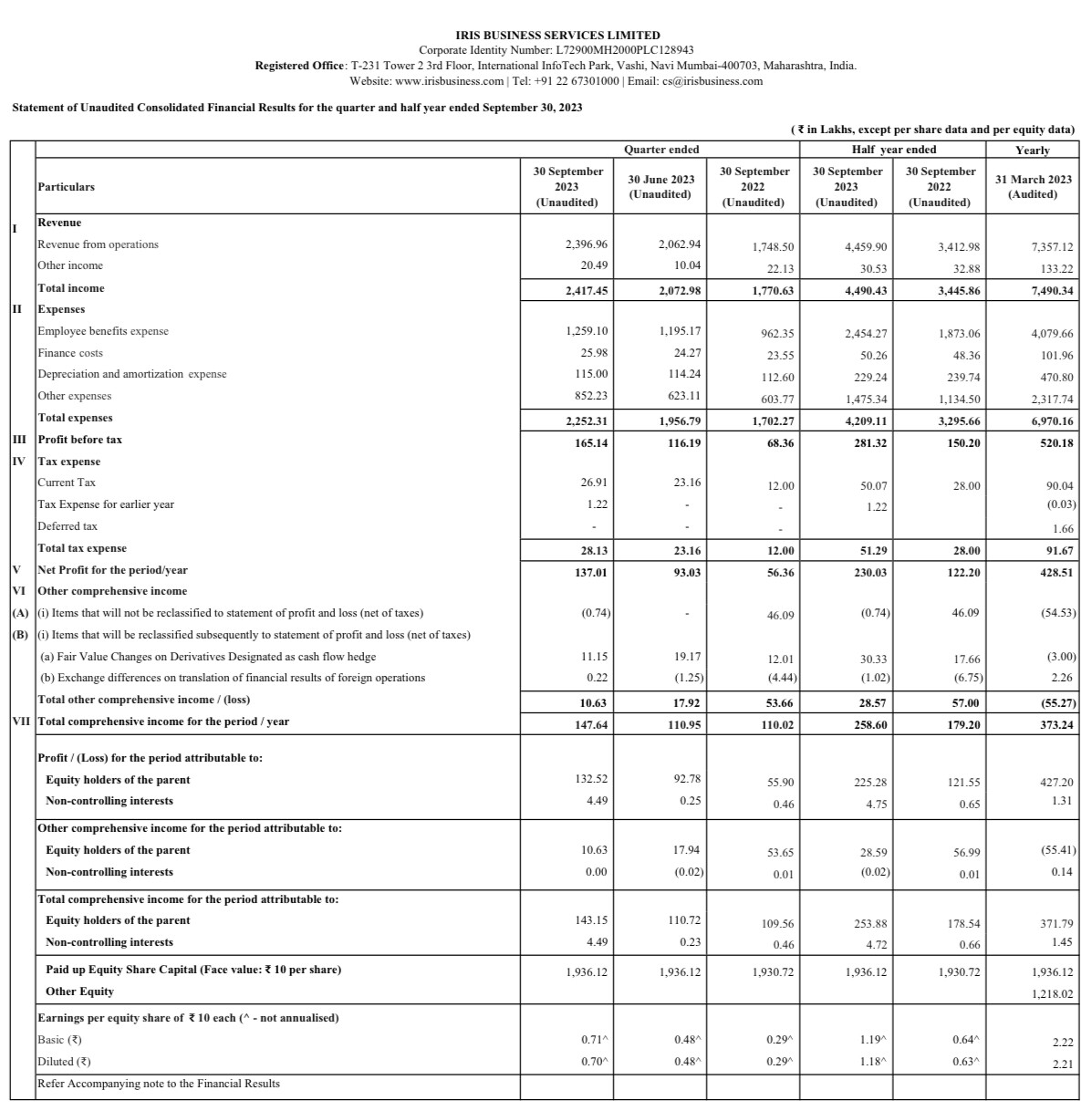

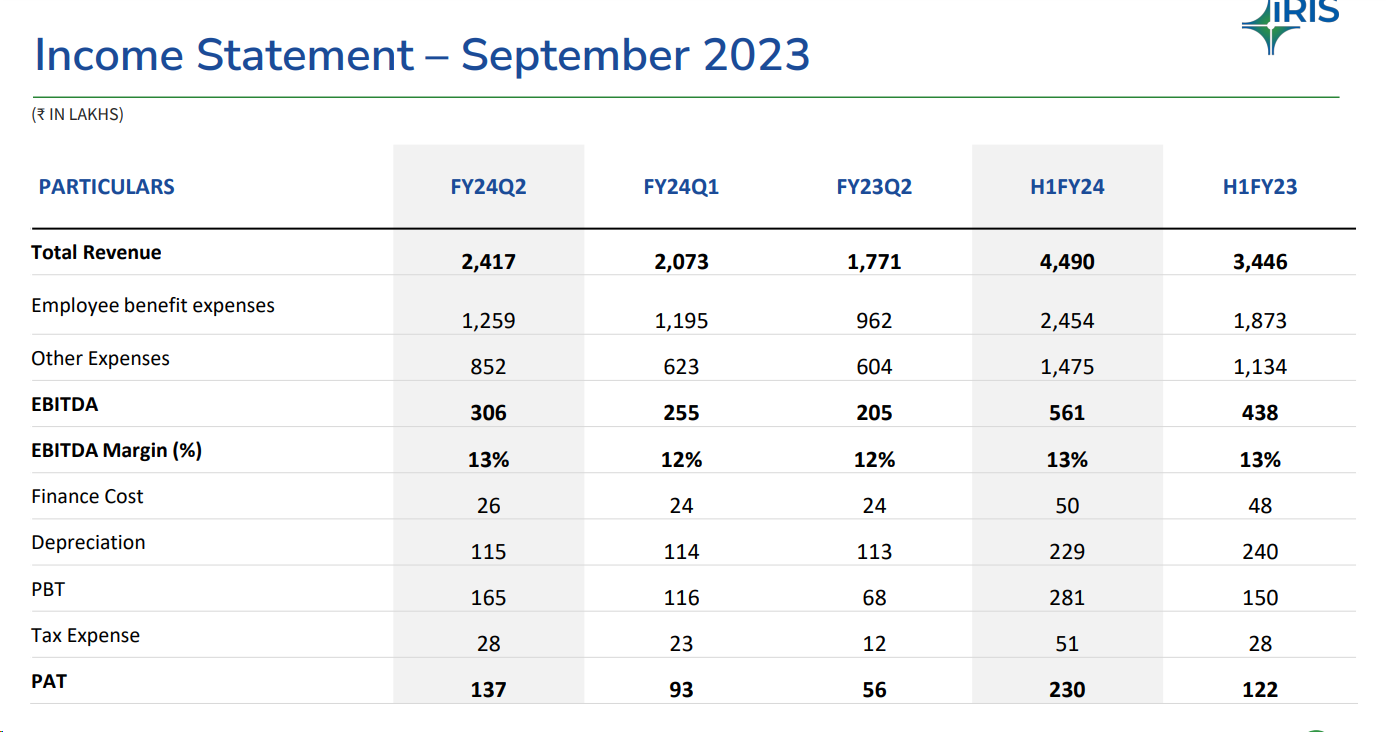

What I find especially investment worthy in these SAAS businesses is the operating leverage which comes into play - YOY the growth in topline is 37% whereas in EBITDA the growth is 142%!

Mr Swaminathan had alluded to this benefit of being a SAAS growth story in the Q1 concall as well. Main contributor this time was the collect business for which the order book continues to look strong. I had also attended the concall this time where again management was very clear in certain aspects, I will share some of the details once the transcript is released.

The promoters have indicated over the AGM and again in the latest concall that they do not wish to dilute further at these valuations (even though they really wish to raise capital to build on the growth for Create).

In the AGM as well, the management was asked regarding the possibility of a rights issue and they expressed that they do not prefer to dilute at such valuations and might explore a convertible note.

AGM video below is as it is quite informative.

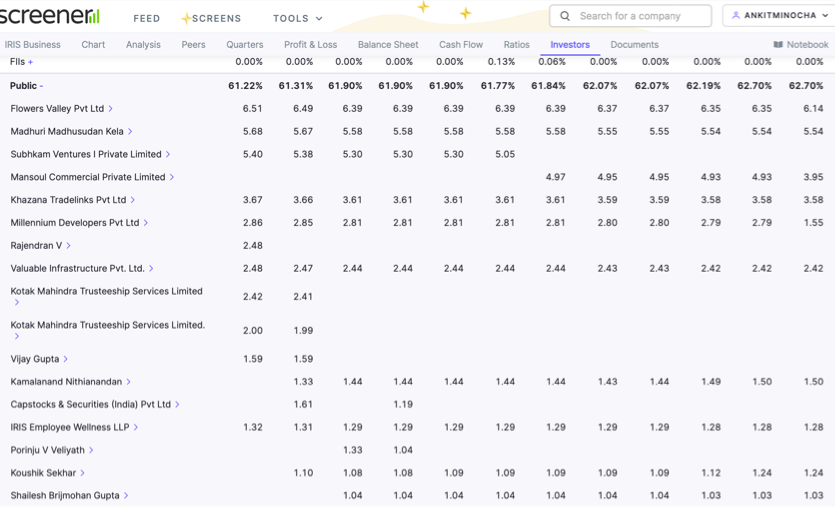

Regarding FII/DII holding, for a company with a market cap of ~250 Cr, I don’t think its the most relevant aspect. One would hope it builds up over time!

Interestingly though, a simple glance at shareholders in the public space shows that Madhuri Madhusudan Kela owns over 5% of the company for a long time.

S & M Spends - Customer outreach and marketing is where a significant increase in spending occurred

Employee - finding difficult to get quality talent at the work. Paying more (Risk)

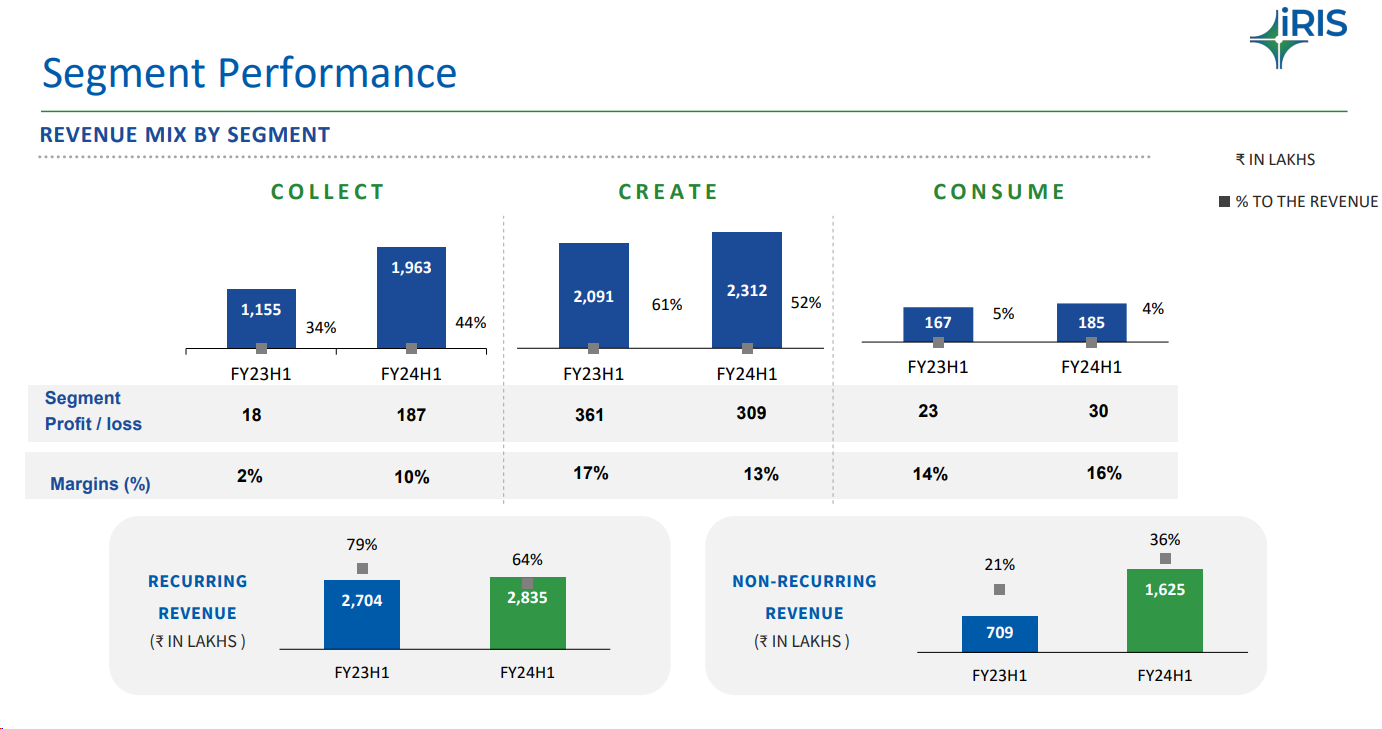

Performing well in Collect Segment (70% growth YoY H1FY24 - H1FY23)

Create Segment (10% growth YoY H1FY24 - H1FY23)

Non Recurring Rev (36% growth YoY H1FY24 - H1FY23)

Increase in export revenue (Indian revenues have come down to about 30% of the overall pie)

Improved order book position compared to the previous year

Establishment of another development centre in Surat. Surat, being a location abundant with skilled professionals, has provided us with a significant boost in

expanding our product offerings and product lines

Collect Business - The iFile business, which is the Collect segment, is primarily driven by RFPs (Request for Proposals). The challenge here lies in engaging with regulators, making them aware of our presence, and positioning ourselves to ensure that RFPs come to us. We actively participate in conferences, engage with regulators, and present our credentials, ultimately bidding on their RFPs. It’s a competitive process, and we win some and lose some

Create Segment - iDEAL is a mandate-driven opportunity where banks are mandated to connect to the Reserve Bank of India. It’s more of an inbound process, requiring minimal sales and marketing efforts and we have a near monopoly, with more than a hundred financial institutions using the product. It’s primarily an inbound process. (iDEAL - 100 customers)

On the other hand, in the highly competitive GST business, within the Indian SaaS and tax tech landscape, we have a dedicated sales team led by our India sales head and regional sales managers covering North, South, and West regions. They are supported by a marketing team and an inside sales team, which is part of the marketing function, responsible for lead generation

CARBON, being an enterprise SaaS product, is targeted at international markets, and navigating the challenges of sales and marketing is crucial, especially during ramp-up. Our approach involves multiple strategies. Firstly, we collaborate with partners, with a significant focus on partners and channels. Additionally, we engage directly with customers. (5K+ customers)

Increase in Authorized Capital - Creation of ESOP Pool - The ESOP consideration is quite different this time compared to the last time we had ESOP before the IPO. Currently, our aim with the ESOP scheme is twofold. Firstly, for existing employees, and secondly, to attract new talent. Many potential hires have placed compensation expectations beyond our current cash range. To bridge this gap and entice the right talent, we are looking at a combination of cash and ESOP. The increase in authorized capital was also linked to the ESOP. Since we are currently in the market raising funds, combining the money raised and the ESOP would surpass our operating capital

The order book has two components – recurring and one-time. INR 110 Cr recurring & INR 10 Cr one time. One large implementation order that we have, from the South African Reserve Bank

Collect Business Outcome - there are countries moving towards bigger XBRL implementation. At the same time, some of them are not necessarily willing to work with us for various reasons. There’s a language barrier, for example. Africa, specifically Morocco, had an RFP some time ago, and it seems we may end up losing it based on the current outlook.

Favorable Regulations for Co: SEBI said that you must report related party

transactions, and that becomes an add-on to what we’re already doing. So, there are adjacent opportunities in terms of products, which also gain their customers as the people working with customers and delivery are also taking ownership for revenues

ESG opportunity is there for sure, there are talks going from the market that it might get postponed by 1 year or so

Disclosure Managements: Disclosure management is going to be the mainstay of our business going forward. This is where our biggest growth is going to come from. Ultimately, companies want to benefit from digital reporting, and they want to find an integrated filing platform. Companies want to go digital, regulators want to go digital. And what we’ve been able to do by combining Collect and Create will actually come home to roost in a very positive sense

I like the business, the technical capability & the customer support (the reviews are extremely positive with a large mention of customer support), my only concern is the aggression of the management.

Mr Swaminathan has been saying this for a while now that they need money to spend on marketing & sales. With every new mandate coming up, a fresh market is created & is ripe for the first year or two before the deadline. The companies need to comply & are open to anyone who’d reach out. This is a much easier way to get a client. The other way is to try & convert a client who uses a competitor’s solution. This is way more difficult as the client’s compliance team has gotten used to the existing solution & there is a training effort etc, that too only when the competitor doesn’t offer to reduce the prices himself to retain the client.

In the current environment, with new mandates springing up, I think the management can spend heavily on sales & marketing. Once a customer is signed up, the SaaS model is such that the cost of incremental clients is extremely low & only sales the meaningful cost. The LTV for each customer would be quite high.

The management has talked about issuing rights to fund this but seems way too focused on not diluting at these valuations. IMO the focus should be growing the business. Having said that, I hope the money generated from the windfall growth in collect business gets redeployed here.

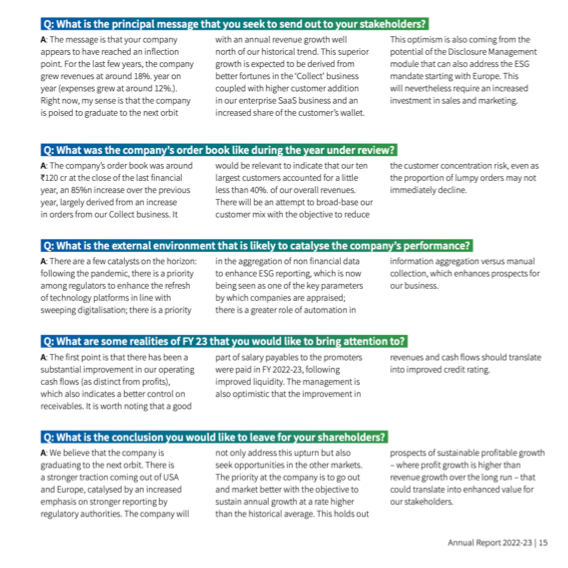

I tried to check this statement out from the CEO and he does seem to have a point. I was quite surprised by the vast gap in the way Workiva is valued on the NYSE and between the Iris valuation here. Just for context:-

Workiva (https://www.workiva.com/en-in/) is valued at ~5.1 Bn USD today, whilst guidance for FY 23 revenue is ~USD 627-628 million

This means that Workiva is being valued at >8x sales, 1 year forward, more in line with SAAS company Rategain (~10x sales). Even after the recent run-up, Iris is still quoting at 3.2x sales.

Big differences : Iris is profitable whilst Workiva is loss making. Iris is miniscule as compared to the established Workiva though.

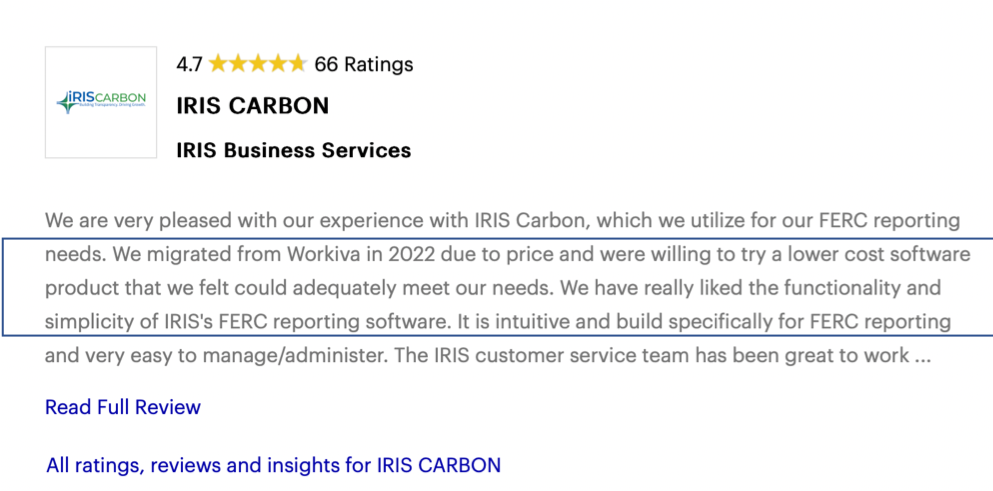

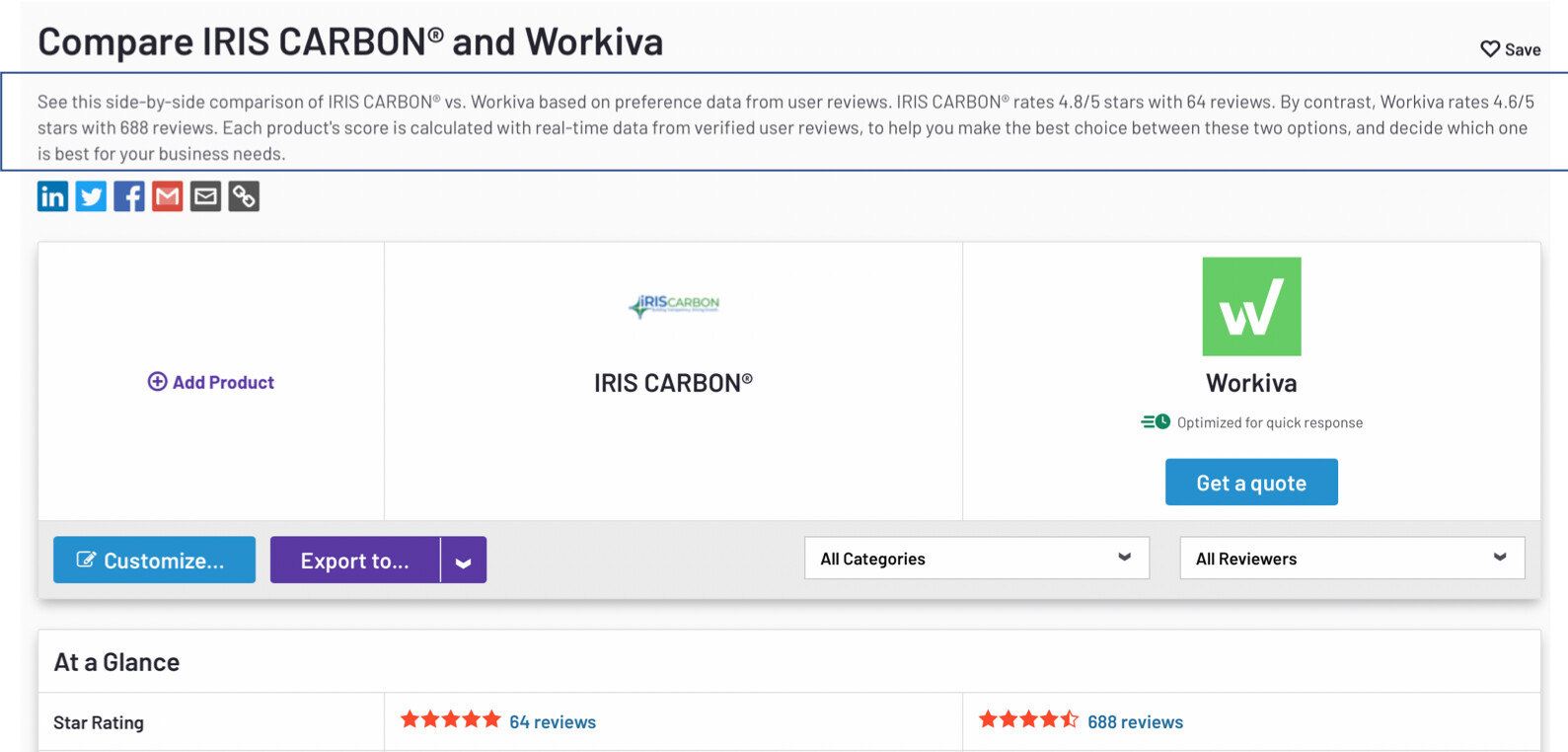

Workiva is a giant in the business, but still growing fast. This does show that the TAM could be large for Iris, and at the same time, competition is strong. Could Iris be the price competitive Indian alternative? I found this review especially interesting

Iris Carbon has some really good ratings on G2review which looks promising, at 4.8 is slightly better than Workiva at 4.6. But we need to understand that Workiva has a much wider review base, and also I have a feeling could be the better product being so much larger in terms of revenue.

Disclosure : I am invested in self and family accounts and am biased. I have made transactions in the stock in the last 30 days. I am not a SEBI registered advisor, not an expert and this is not investment advice.

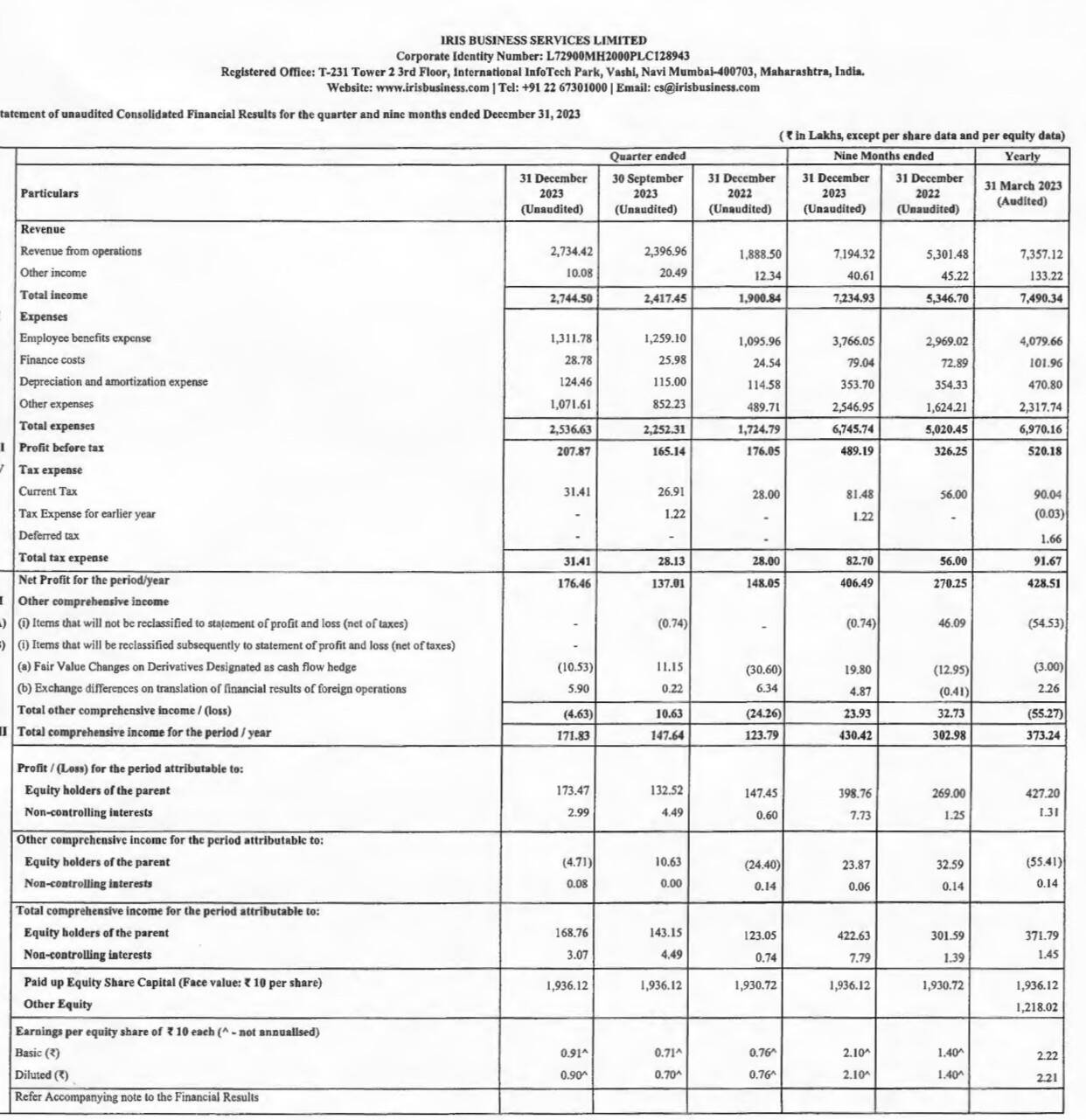

EBITDA grew 24% QoQ and 16% YoY. Reason for lower EBITDA growth is that company has recently increased its partnerships in US and LATAM as a result of which partnership fees has 2x QoQ and 6x YoY. Also, travelling costs have increased which is a good indicator for their potential SAAS product marketing in US.

Segment-wise revenue growth and contribution is as below

Sales

Q3 FY24

Contribution (%)

Q2 FY 24

Contribution (%)

QoQ

Q3 FY 23

Contribution (%)

YoY

Regulators

Collect

12.52

46%

10.8

45%

15.82%

6

30%

120.42%

Filers

Create

13.65

50%

12.3

52%

10.62%

12.28

65%

11.16%

GST, Analytics

Consume

1.16

4%

0.8

3%

45.00%

0.91

5%

27.47%

With regards to segment-wise revenue, Collect has been the driver which is a low growth RFP-driven segment where company already holds 10% of world’s XBRL market share.

However, keep in mind that the major potential growth driver, which is the Create segment is based on SAAS model where billing typically happens at the end of financial year. So, the 11% YoY growth in this segment is not a good indicator

Need to keep a close eye on Create segment growth in Q4 results to assess the full growth trajectory.

Also, the company has shared Segment results, anyone has any idea what they are? Operating profit?

Basically “Create” primarily includes IRIS Carbon which is their core SaaS offering which works on a subscription model meaning clients pay on a periodic basis.

I might have been wrong here as I think this actually should be looked at from a QoQ basis considering the recurring nature of revenue. Ideally, this segment should be driving growth and not just the collect segment where there’s limited addressable market (by my rough estimates, company already holds >20% of world’s XBRL market share amongst regulatory bodies).

From their Nov con-call: Recurring revenue declined to 64% from 79% in FY24 H1 (on track for 54 Cr in FY-24) because of Collect implementation which has a one-time implementation fee. It should hover around 75%

If you compare it to the global leading player like Workiva, there’s still a ways to go considering Workiva’s subscription revenue is ~88% and gross dollar retention is ~98%