Hi there everyone,

In our IPO discussion thread we had posts prior to listing of IRCTC. I could not find a thread on IRCTC therefore I am starting one. Request VPers to start contributing ![]()

I intended to have a very crisp start to this thread by framing 3 simple questions which should set us on the path to understanding more about the company. I was inspired by the thread started by @Donald to have this framework approach to understand businesses. Aside I think IRCTC is a relatively easy business to understand. Please correct me if I am wrong.

Inputs and participation welcome from @dd1474 , @yourraj , @bheeshma , @Vivek_6954 , @rathi.saurav , @himanshupant , @jhasuraj , @pmehta , @bhaskarjain and others

The 3 questions:

1. How do they make money

2. Why do they make this money

3. How will they make more money

How does IRCTC make money?

IRCTC makes money via 4 business lines

- Internet Ticketing

- Catering

- Packaged Drinking Water

- Travel & Tourism

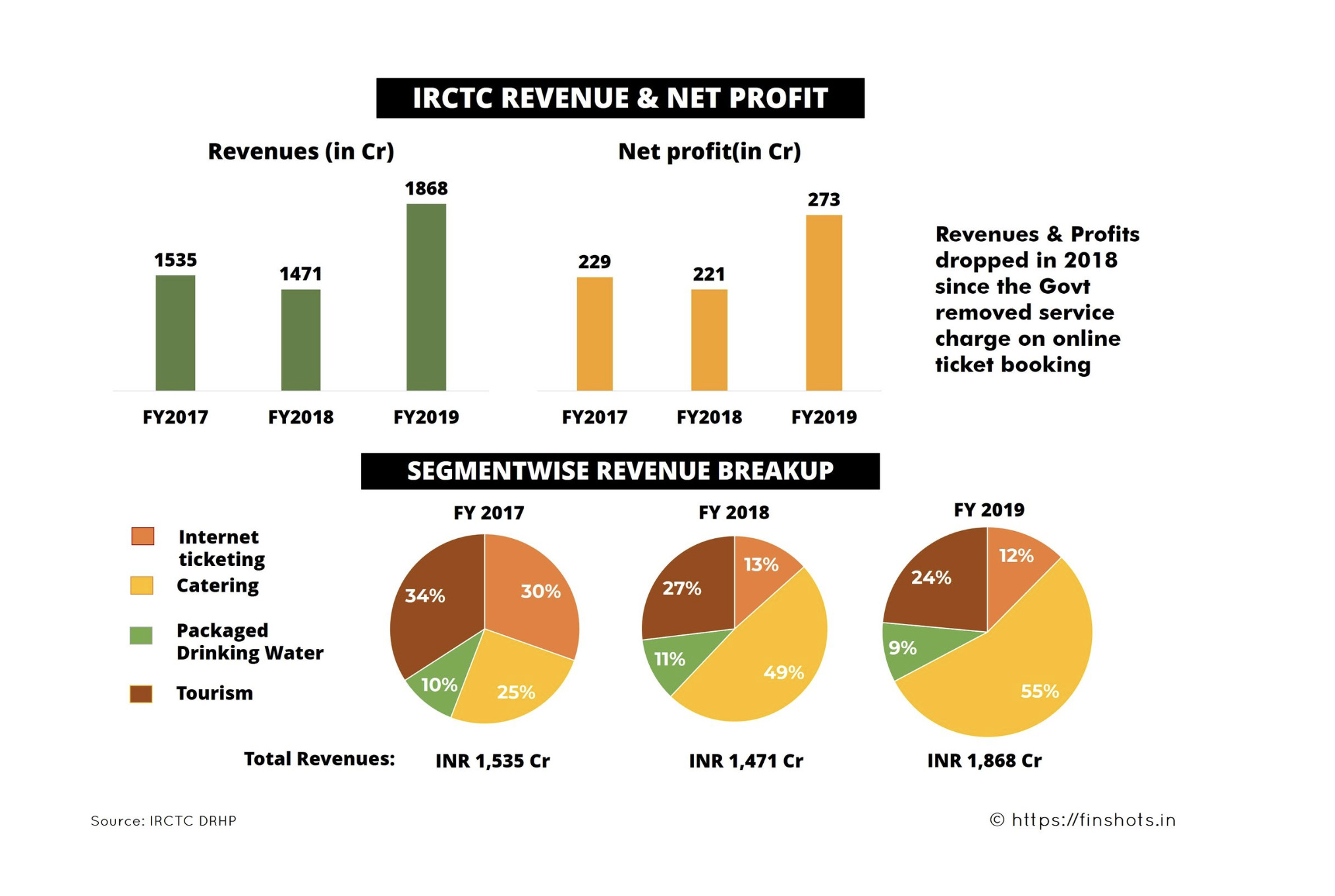

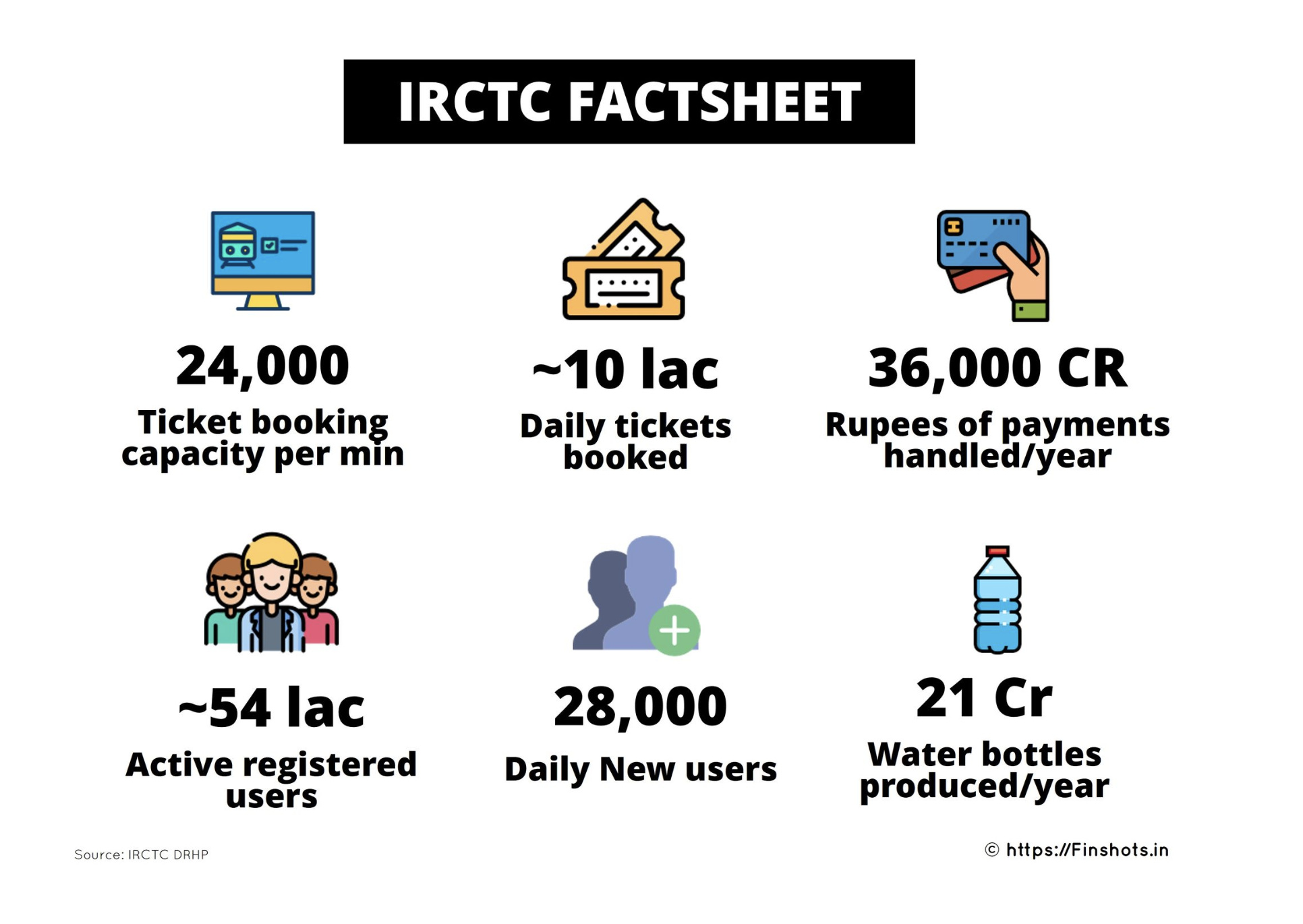

Finshots has a nice infographic capturing the numbers.

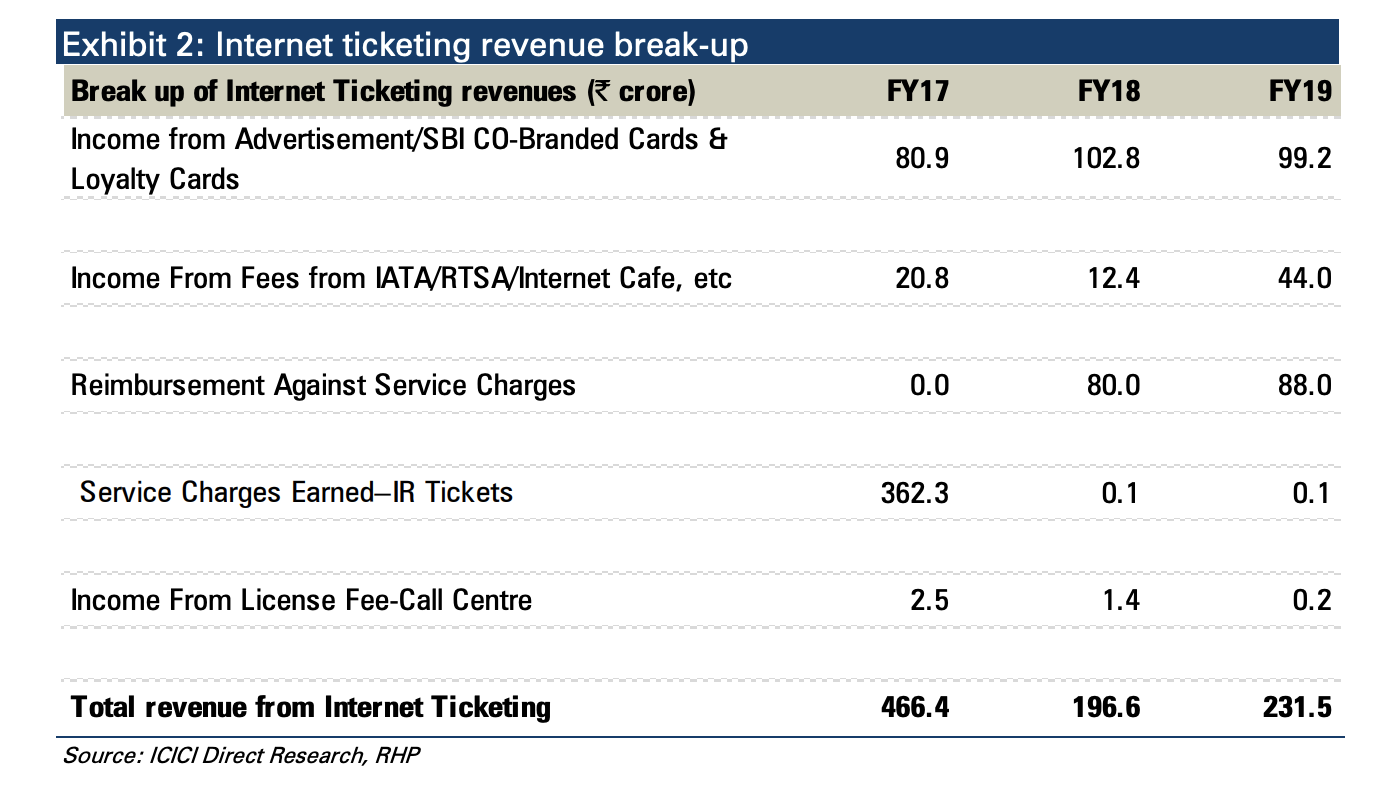

Internet Ticketing:

- The only entity authorized by Indian Railways to offer railway tickets online via website and mobile apps

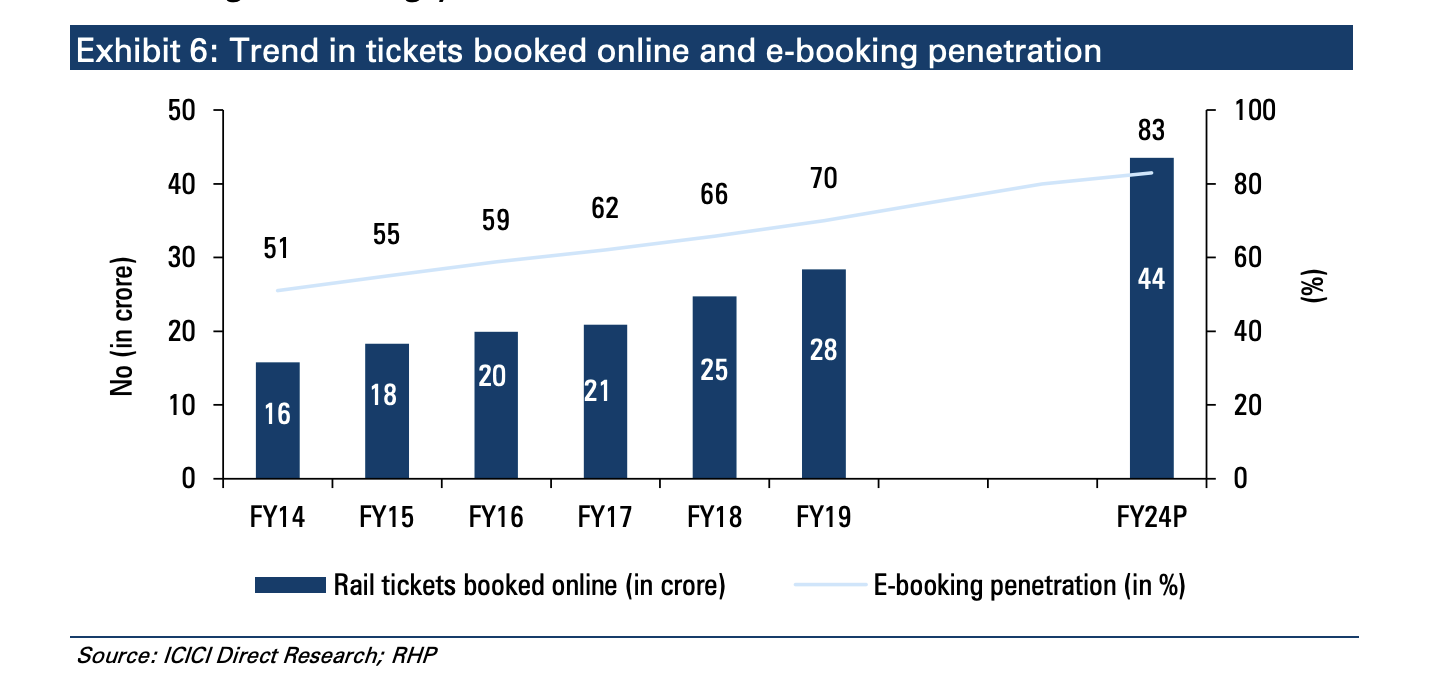

- 1.40 million+ passengers travelled on Indian Railways on a daily basis, which consisted of approximately 71.42% of Indian Railways’ tickets booked online (June '19)

- More than 0.80 million tickets booked through irctc.co.in and Rail Connect on a daily basis

- Transaction volume of more than 25 million per month and 7.2 million logins per day

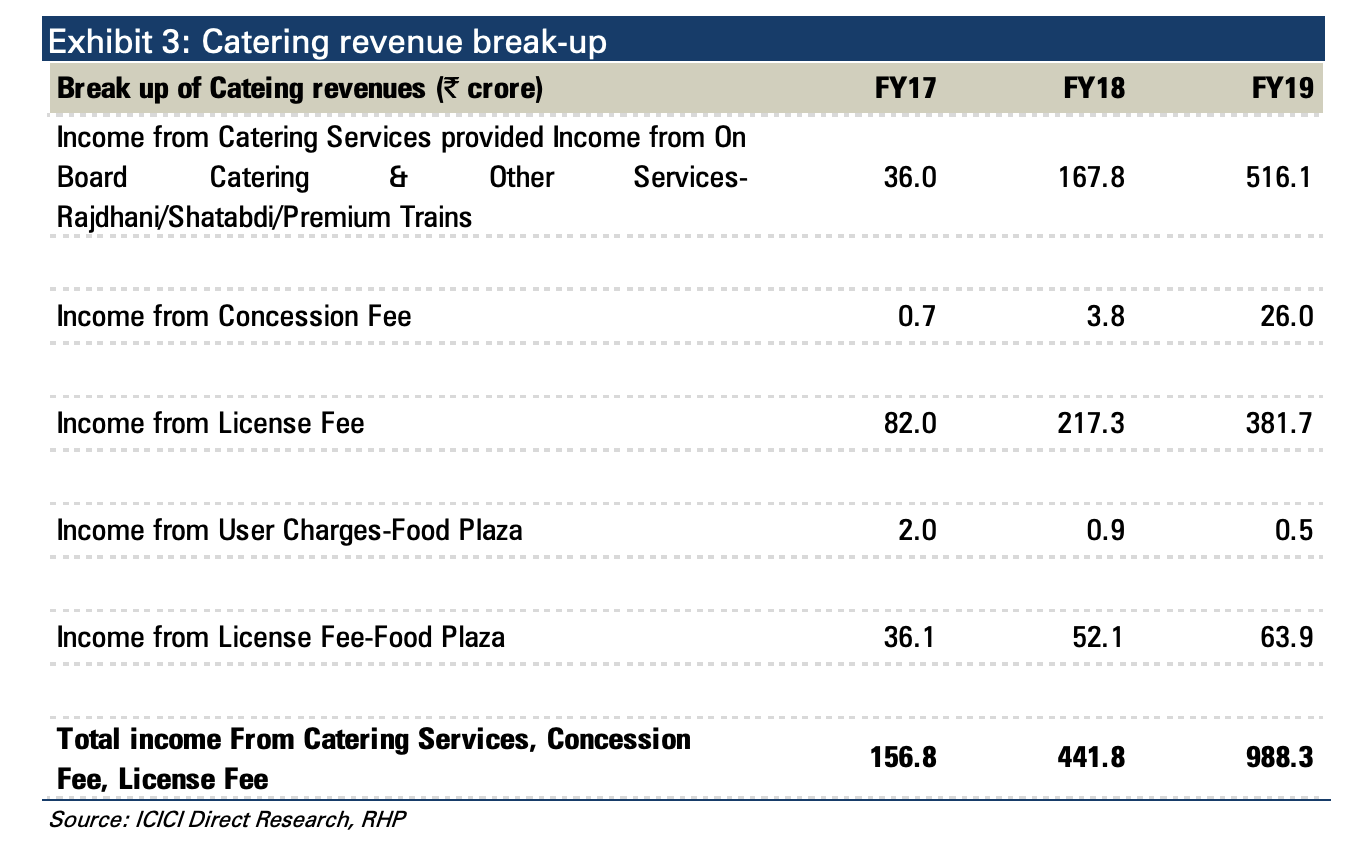

Catering:

- Food catering services to Indian Railway passengers on trains and at stations

- On-board catering services are referred to as mobile catering and catering services at stations are referred to as static catering

- Provide catering services for approximately 350 pre-paid and post-paid trains and 530 static units

- Catering services through mobile catering units, base kitchens, cell kitchens, refreshment rooms, food plazas, food courts, train side vending, and Jan Ahaars over the Indian Railways network

- Offer e-catering services to passengers through mobile application Food on Track and e catering website, ecatering.irctc.co.in

- Operate executive lounges, budget hotels, and retiring rooms

Packaged Drinking Water:

- Only entity authorized by the Ministry of Railways to manufacture and distribute packaged drinking water at all railway stations and on trains under brand ‘Rail Neer’

- 10 Rail Neer plants located at Nangloi, Danapur, Palur, Ambernath, Amethi, Parassala, Bilaspur, Hapur, Ahmedabad and Bhopal, with an installed production capacity of approximately 1.09 million litres per day, which caters to approximately 45% of the current demand of packaged drinking water at railway premises and in trains

- Setting up new Rail Neer plants at Sankrail, Jagi Road, Nagpur, Bhusawal, Jabalpur, and Una and further plants at Vijaywada Ranchi, Vishakhapatnam, and Bhubneshwar

- Installed water vending machines at railway stations to provide purified, chilled and portable drinking water

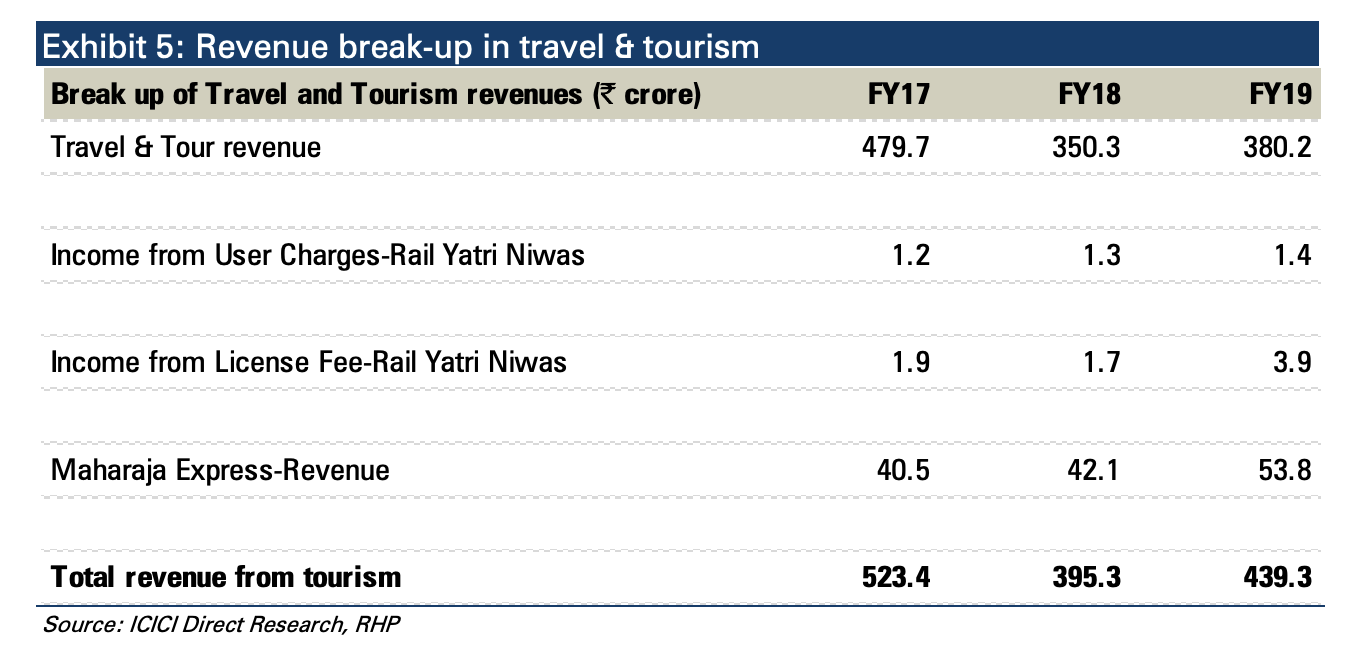

Travel and Tourism:

- Presence across all major tourism segments such as hotel bookings, rail, land, cruise and air tour packages and air ticket bookings

Why do they make this money

Regulatory advantage:

The second question has a straightforward answer - In 3 of the 4 business lines they hold a monopoly owing to regulations. They sell roughly 8-10 lakh tickets online daily which constitutes 3/4th of all the tickets sold in the country daily. In catering which constitutes the chunk of the revenue they are at an advantage owing to the Catering Policy of 2017. For packaged drinking water it is the only entity allowed to sell in rails and on stations. Though this is the smallest revenue contributor. The tourism segment is where they make quarter of the revenues but face competition. This segment has had a decline over the last 4 years. They have Rail Tour Packages which has seen major de growth and Land Tour Packages which has seen an uptick.

Pricing Power:

They truly dont have pricing power. Someone can correct me if I am wrong. This is one of the risks called out in the DRHP also. For instance during demonetisation they had to remove convenience fee on the directive of the government. Another instance is that they have a tender process for in rail delivery for which they charge 12% which is also fixed as per directives.

Network effects in ticketing business:

This business line reaps revenues without much increase in costs. It is directly linked to passenger numbers and adoption of online ticketing. IRCTC is also a very sophisticated payments player and has a lot of advantages owing to its monopolistic position.

A snapshot again by Finshots below

How will they make more money

Growth in rail passengers:

- Passenger traffic on the suburban network is likely to grow at a 0.5-1.5% CAGR till 2024 while non-suburban passenger traffic remain flat

- Within non-suburban passenger traffic, share of upper class reserved ticket bookings in total railway passenger traffic is expected to grow slightly from ~2% in fiscal 2019 to ~3% in fiscal 2024, with the segment growing at a 5.5-6.5% CAGR during the period on account of growing preference for convenient travel

- Share of second class mail/express ticket bookings (reserved) is expected to inch up from ~17% in fiscal 2019 to ~18% in fiscal 2024, with the segment growing at a 1.5-2.5% CAGR

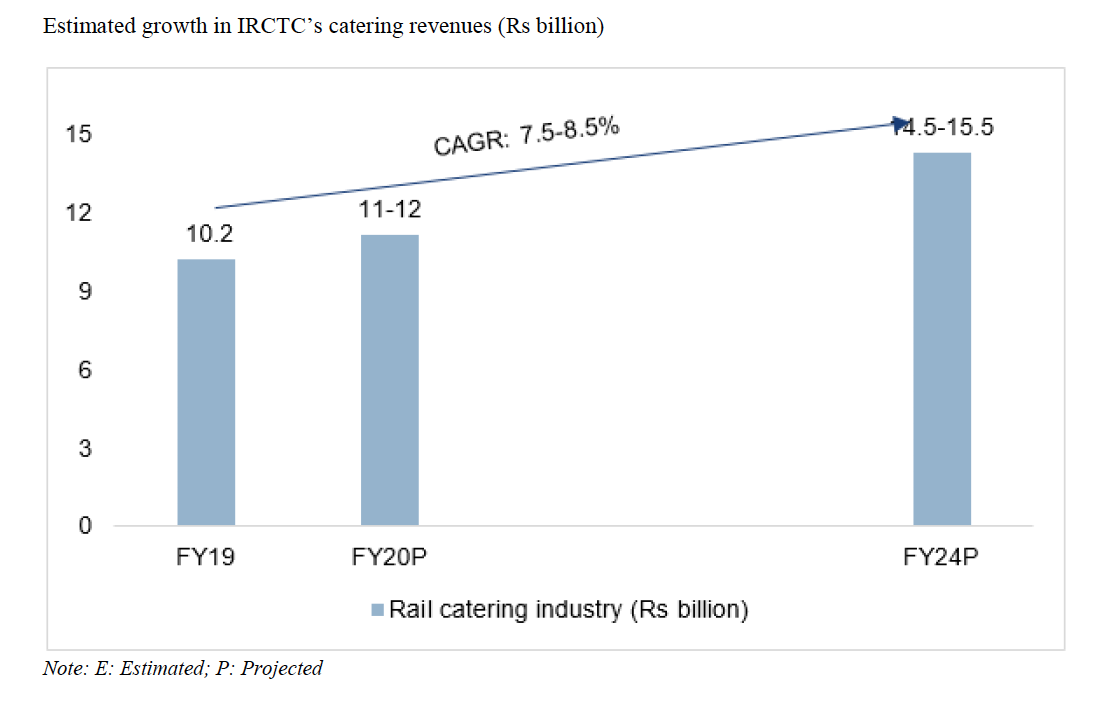

Catering Revenues:

Catering revenue is expected to grow at 7.5-8.5% CAGR between fiscals 2019 and 2024 The growth in IRCTC’s catering revenues is expected to be driven by:

- Likely increase in passenger traffic due to addition of new non-suburban trains i.e. long distance trains

- Rising affordability and variety of food items available in catering services

- Increasing coverage of catering services through addition of base kitchens and static catering units

Packaged Drinking Water:

Rail Neer distributes water to only a few Railway establishments in India due to constraints in capacity Rail Neer is expected to increase coverage to majority of Railway establishments in the country via PPP

Market size of railway establishment for the packaged water is estimated to grow at 2.1%-2.2% till '24

Travel, Tourism & e-booking:

- Domestic and foreign tourists expected to grow at 9%-10% CAGR till '24

- Government initiatives to promote tourism via improved infrastructure, easing of visa regime, assurance of quality standards in services of tourism service providers, projecting the country as a 365 days tourist destination and so on

- India contributes more to South Asia tourism than the average levels for the region

- Currently 50% of ebooking is for airlines, 30% for hotels and 20% for rails. IRCTC has complete market share in rails due to regulations. Overall growth till 2024 is expected to be 16%-17% on a CAGR basis

- IRCTC does not offer international hotels, buses and cabs in its ebooking product portfolio. So that is a scope of expansion

- IRCTC has special train tourist packages based on certain themes. Also luxury train rides

- All government entities book their airline tickets via only 3 entities and IRCTC is one of them

- They have their own wallet which I am not sure is actually making any revenues or not. They have a partnership with SBI to issue co branded cards. I believe this is quite popular

The achilles heel for IRCTC is what makes it a good investment today and that’s its monopoly. Any change in regulations with respect to opening up of

a) Ticketing to other players

b) Bringing in 3P vendors for catering

c) Allowing other packaged drinking water suppliers to sell at railway establishments

will take away revenues from IRCTC. It is in a very comfortable position as of now. And with growth in travel and online ticketing the numbers should keep coming in. This is something which I believe retail investors will have to keep gauging and reacting appropriately.

I am not touching anything on valuations. Feel free to do so in the posts below. Also lets ask 2nd and 3rd order questions. That is the key.

Regards

Deepak

Disc: Invested. Transactions in last 30 days. Not a registered advisor.

Sources: DRHP, Isec, Finshorts, HDFC sec