@dd1474 @fabregas The Stock is now available at 34 levels . Last year they paid dividend of ~12 and assuming it comes down to 8 this year due to 1months suspension of tolls…and stays at same levels for next 4years…we are getting our entire capital back in 4years!

NHAI has confirmed the extention of toll concession by 3-6 months depending on toll collection and it is a positive for IRB’s projects as NPV goes upto 1.3x for projects less than 5 years according to ICRA

Also news reports suggest that toll collections are ±5% to the pre covid months!

There is good risk reward at current valuations and a definite play on Unlocking the economy

Views Invited

@mahe9703

I see two broad as key consideration:

- With Rs 6-8 distribution (I assume nominal distribution during FHFY21 due to COVID and resulting economic slow down), even at Rs 6 distribution and price of Rs 34, it is trading at 16% current yield which can improve in future. Hence it is absolute value buy.

- If it is tradings as such attractive yield, why capital market is blind? Secondly, why we do not find major buying from insider if that is so real value trade! The limitation of funds at insider end could be one reason but market was reasonable correct in valuing IRB InvIT at declining from 70 to 30s in last one year (in expectation of lower distribution) and increasing price of good Stable India Grid InvIT Price from 85 to 100. After year, while distribution in India grid at worst likely to remain stable, IRB InvIT it could decline. Many investors who are looking at stable income may not like that factor and hence there could be higher supply in market. While price to a broad extent discount lower FY21 distribution in my opinion, I thought IRB InvIT as attractive investment at 70, further at 60 going down al the way to 30s. Lower price does not mean it can not decline further by 50% to ₹ 16-17 for short time.

One more point to consider no growth in future assets. At the valuation at which IRB trade, it is better to buyback units from borrowed fund then to expand the assets. None of assets in road till project is likely to give kind of 20% yield which IRB InvIT offer at time being. Managment has not done anything to support value.

Third point would be market particpant would wait for performance of IRB distribution over next 3 years. While 6-9 months is bad for everyone, IRB also have perceived issue of cashflow distribution sustainability. Bharuch Vadodara and Dahisar Surat project accounting for 40-50% of NCDF are likely to handed over by 2022. While valuation report projection of IRB showing improvement in other 5 assets cashflow to provide for future distribution, two of Major assets that is Pathankot Amritsar and Jaipur Deoli has failed to see traffic growth which was projected in past. Hence, despite everything attractive in valuation, there are project specific issue which increase volatility in distribution in IRB InvIT and hence lower price.

Whether one should buy at current level or wait or switch, it would purely depend on each individual risk profile and cashflow need. For certain livelihood expenditure in future, IRB is not appearing the best choice in my opinion. For a risky investor, it may be attractive but market is full of such opportunities in equity segment as well. So why risk with unproven structure in bad time?

Personally, I would wait and watch and continue to keep my holding with close monitoring. I may change my view without informing forum. Hence please do your own due diligence before investing

Discl: I hold units and added marginal quantity in last 3 months. My view may be biased. Not sebi registered analyst. Not recommending investment

@dd1474 I would like to understand why you feel it can’t go down lower than 30+ to below 20? Problem with IRB is clearly the management team running the show (they have proven to be highly incompetent).

The cash flow hit would get compensated with additional time period for toll collection. I feel something is more seriously wrong for market to value IRB at this price - just temporary reduction in cash flows is not the answer.

I missed critical NOT in my previous message which I have edited now. What I meant is further 50-60 or rather 99% decline is possible with various probabilities for IRB InvIT as well.

On management part, I agree with you partially. While there have shown to reactive and pretty mediocare (even unitholder request of putting disclosure of con call detail on BSE website which have been expressed in my presence in AGM and further Followed up on con call Is also not addressed), the structure provide some comfort to compensate incompetence of management. With 90% of NCDF need to compulsorily distributed to unit holder every 6 months stipulated in InvIT structure along with FasTag implementation reduce risk of cashflow understatement in my opinion. Only repair and maintenance part of expenditure is what management can decide. So to that extent investor is protected in my view. However, like anything multiplied with zero is zero, similarly whatever great structure, if it is intent issue then competence, investors (including me) would pay price. In my normal

INvestment process, I do not even enter in this type of management. In IRB InvIT I thought InvIT structure would protect my interest. Till now market is signaling other way round and probably I have become rigid to not book lose. May end up paying Further tuition Fees by way of further erosion in price and then book material loss. Only time would tell.

So appreciate your point about management, but also need to appreciate InvIT structure which provide limited cashflow for misappropriation. The second way was to buy expensive valuation assets is also appear to be not risk at current valuation in my opinion. The investor would insist proper distribution then issue of new unit to acquire assets in my opinion.

On your second point of efficient market and price is indication of uncertainty of market about the Managment Of IRB , I agree and also share example of Indiagrid InvIT (I am invested and may be biased) which moved exactly opposite way during last 12 months post KKR taking over control from sterlite group.

We both seem to sail in the same boat. I have invested money for my dad in both IRB Invit and India Grid. IRB I bought around 70s thinking with stable cash flows and Invit structure the risk of further drop in price was limited. I had projected ~15% yield at that time. Had similarly bought India Grid at average price of ~87 being fine with a 13% yield.

India Grid has been following a good strategy but IRB I feel has done few simple things wrong which I feel is due to management lacking foresight. Initially when IRB Invit was quoting at 16% yield they did a separate private deal with GIC which shouldn’t have been done. Should have got GIC to invest in the listed entity while transferring the assets to the Invit once they stabalized and they should have tried buying back units.

While SEBI guideline allowed buyback, there are certain limitation for InvIT to buyback units. First they need to distribute cashflow to the extent of 90% of operational inflow NCDF). So only 10% of business cashflow remain in InvIT trust. Second, they can not borrow funds to acquire units. Hence, there is only lmited trustee can do to protect InvIT value from buyback. It can happen only if sponsor or other investors show confidence and acquire unit.

Even Indigrid seen major decline from 100 to 81, till KKR and GIC entered. Since then, the other has been growth as well distribution which allowed other investors to hold on to their investment. That being not casse with IRB, many are waiting in sideline to exit.

yes, the SEBI guideline for buyback is a real damper. They should ideally use the 10% to buyback whatever small amount they can buyback from market to show confidence. In current yields, buying assets with Debt also should help in improving yields and help in stock price appreciation.

hi, thanks a lot for elaborate input, However i frankly think the price reflects all the negatives in fact beyond the most pessimistic scenario, i can not think why the distribution can below 6-8 at all for next 4 years, which means the capital is well protected, so upside is there while downside is capped

I dont think even you expect the toll collection to fall dramatically in FY22 from FY20 levels, even if its same we have a good risk reward at current price

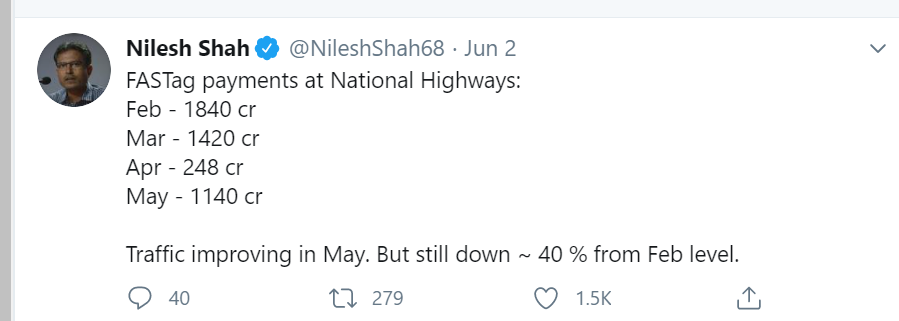

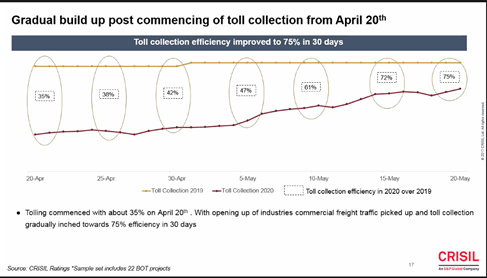

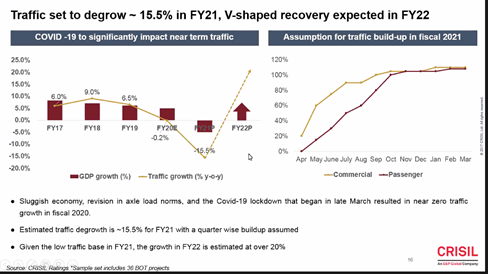

Today Crisil organised Webinar on Road sector prospect post COVID. Couple of slide provide very good insight about comparison of toll collection over last year for 22 Toll projects compiled by Crisil.

Based on above, one shall expect around 40-50% decline in toll revenue for IRB InvIT during Q1FY21, in case IRB InvIt follow Crisil sample collections,

Can you please elaborate the rationale behind 45-50% de growth numbers? Also whats your expectation for FY 22??

Based on Crisil Estimate of toll collection as per cent of last year same month, I guestimate Toll collection for IRB InvIT as % of Last year same month as enclosed :

![]()

So In my estimate, toll collection would be around 55% for Q1FY21 as a per cent of Q1FY20 for IRB InvIT if they follow estimated pattern of Crisil shown in webinar. Please note that it is more of guestimate and may vary by wide range as my understanding is very limited and only restricted to Crisil study.

Discl: Invested, may be biased, not a SEBI registered advisor, Not a recommendation

40-50% Decline for Q1 IMHO is not at all a bad number. From Q2 it can have good recovery. Overall for FY21 and FY22, what’s your base case and worst case DPU?

My stand of staying away form this InVit has paid off of course in hindsight. I had a very simple evaluation to make - it was committing a stable cash flow profile to its investors but its own cash flow is going to be volatile. As an average investor we have no ability to evaluate risks to cash flows since it depends on multiple factors beyond the operator’s control like virus impacting traffic. There WAS and IS no certainty of cash flows and these are suited for private equities rather than retail investors looking for stable yield. This mismatch in expectation was supposed to play out in the unit prices and it has. Blowing its capital in maintaining a stable yield is not a prudent capital allocation for the long term.

@mahe9703 I thought the same ever since the units were trading at around 70 levels. I kept investing as the unit price fell - at round 63, 56, 51, 46 and 40 levels.

These are some of the points, which I think the market is concerned about:

- Forming a private InvIT with GIC was a major dampener. This straightaway put 9 operational and soon to be operational assets off the table for IRB InvIT.

- The management comes across as very mediocre on the concalls. They have provided guidance for asset acquisitions 2 times in the past, which never materialized. A simple promise such as submitting the quarterly presentations to exchanges has not been fulfilled. If you are not aware, IRB InvITs only uploads the quarterly presentations on the company website. They are not sent to the exchanges, which is the usual practice among well managed companies. To me it looks like no one wants to take ownership of or be held accountable for the data being put in the presentations.

- No significant buying by promoters even as the unit price has fallen drastically. This may be due to the limited availability of cash with the promoters.

- They do not even maintain an asset pipeline for possible acquisitions. To give comfort to the investors when the InvIT has a declining revenue profile (some assets will be handed back to NHAI after completion of concession period), you atleast need to provide some guidance on future assets.

For me InvITs were a way to diversify into stable cashflow when the overall stock market valuations were high. So capital protection was of utmost importance to me. IRB InvIT provided neither stable cashflows nor capital protection. I finally decided to cut my losses and exited entirely at around Rs 36.

While at the current prices it may actually be a good buy, I think soon the equity markets will have many opportunities to earn a much higher return. So I have also completely exited my holdings in IRB InvIT as well as Indigrid, in anticipation of much better opportunities in the equity markets.

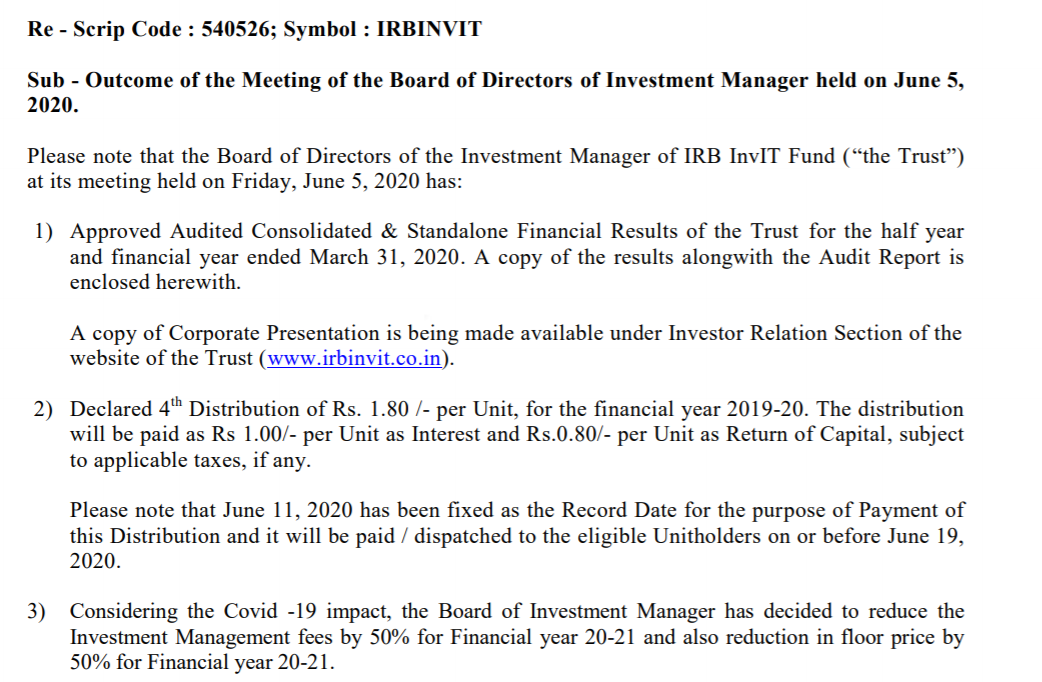

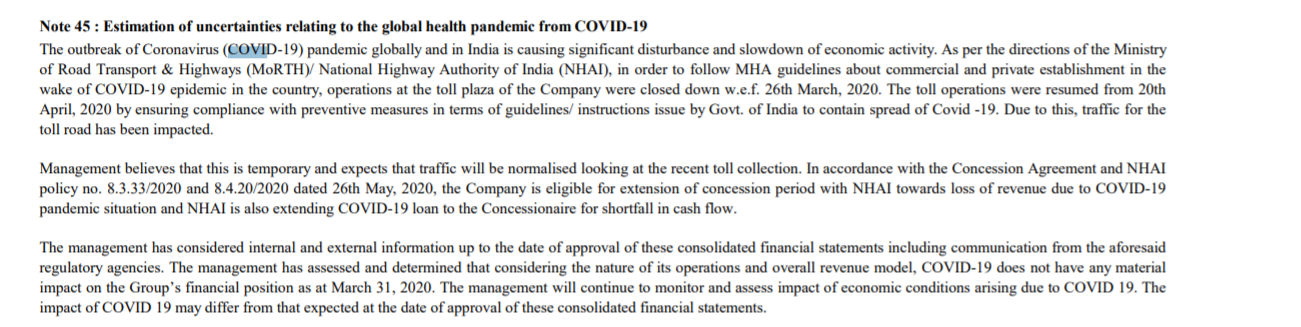

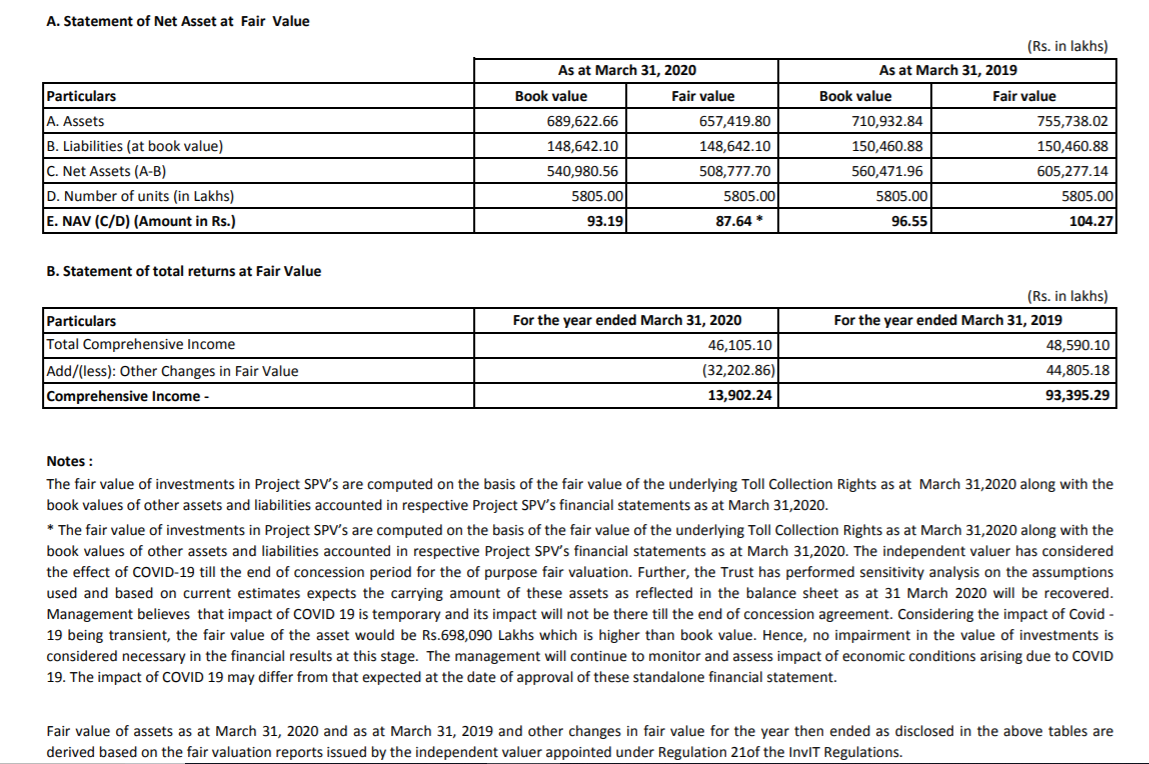

IRB Invit Results are out, Looks decent to me and they declared 1.8 dividend for Mar qtr (20% annualized Yield). Also snippets of Covid impact on fair value

@dd1474 Realy appreciate if you can shed some light on the latest valuation report and results (March quarter). I was expecting more than Rs1.8 distribution… with loss of toll revenue for 10-15 days, distribution has been reduced by ~30% compared to the previous quarter. Wondering if the INVIT can siphon off money using maintenance and other means if the management is unethical. In general, wondering what the downside risks are(at Rs 6 distribution looks attractive to me). Management has given distribution guidance similar to the March quarter. Is it feasible? (given June quarter is the worst).

Discl: Invested around Rs 34

Just working in updated sheet. Your sheet will help me to give heads up

Hi Praveen, anything on the updated sheet we can learn from?

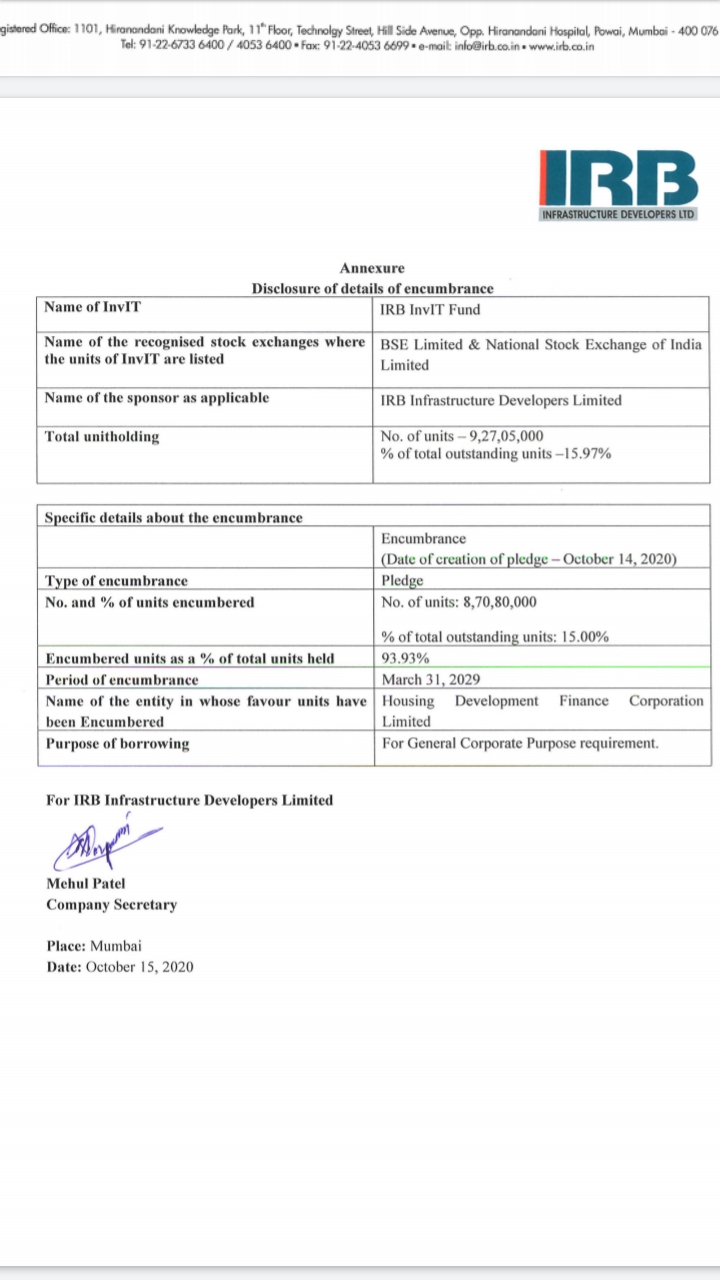

The promoter, IRB infra, has pledged 94% of its holdings in IRB Invit. It clearly shows the dearth of funds at promoter level, however, I want to understand what happens if these units have to be sold in the market by the pledger? In such a event, off course the units will sell at further discount, but how will the invit function without any sponser in such a scenario? How will it impact minority shareholders?

@dd1474 - can you through some light.