Hi Amit

This is a worst case scenario !

If IRB goes under/Mahiskars go under…IRB Invit is in trouble.

But pledge revocation due to default is a remote possibility

In my opinion, it would have same impact as equity pledge by promoter. In worst case, the pledged can be invoked and promoter group may change. However, given the reputation of promoter group, I do not see it as a major negative. Since IRB InvIt is a trust structure, which has limited insolvency (since the trust own road assets along with debt), I would not see material negative impact. Only role currently management play is to manage maintenance of 7 road assets which I believe can be easily replaced. However, one need to be careful about sponsor reputation.

We have seen Sterlite group (Original sponsor of India Grid InvIT) existing from InvIT and KKR replaced them as sponsor. Market viewed this development if price of IndiGrid unit is any indication.

This is my view and it may be wrong. Please also note while I hold units in IRB InvIT and IndiaGrid InvIt, I may change my portfolio in case I get attractive opporunity. Please do your own due diligence before making any decision

1 Like

Results are back to Pre Covid levels and I hope that the units price will also move up in coming 2/3 quarters. Investing gradually as a replacement to my long term FDR

Any comments on the valuation report and Half yearly report.

Team, waiting for more info on this invit. Found this thread very useful in helping me make my decision for investing at 35/36 levels and now fully invested. Looking for feedback as this invit has inbuilt growth although uncertainty considering economic growth but will beat FD rates in long term. Management call in next one year for bringing couple more projects is being anticipated cautiously by market but I feel same should not be a concern with current interest rates and capacity to increase debt resulting in a margin of 4/5 %. Views appreciated from seniors as I am still getting tempted to increase my holdings

Please look at past track record of managment. IRB group created another private InvIT in partnership with GIC. So that is one concern.

Second is about two main assets being coming out of concession agreement.

Third, no growth opportunity. If the listed unit are trading at 18% yield, which assets can improve yield for investor? Only if yield is greater than 18% and such assets (completed infra road with 1 year cashflow track record), if trade at more than 12-13%, then there may be more chance of something wrong than right.

So till the trust see improvement in price to trade at 10% yield, I as an existing investor would not be key supporter of new assets. Having said that, despite such attractive yield, there is very limited insider purchase.

In view of above, I am curiously watching my position. Excellent distribution and linkage of business with economy revival may result in turn around fortune around of the InvIT. As of now, that is more of hope then happening, in my opinion.

I am optimistic on current holding and pessimist for new investment in the trust.

Discl: I am investor and hence my view may be biased. I can change my position without informing forum, in case I find other attractive opportunities. Please do your own due diligence. I am neither sebi registered analyst nor recommending any investment action in the trust.

2 Likes

Dhiraj and other valued contributors,

I will vary the thought a bit and give you our take. Please feel free to critique !

A. For any asset to be acquired with pure debt what you say about yield needing to be more

than 18% is not true. As it is pure debt the differential in asset IRR and cost of borrowing is

enough to bump the yield. BTW, the debt headroom is 4000 crore or so. So potentially it

could mean a 120-140 cr additional NDCF …

B. I would not fault IRB on the GIC deal as opening another front is not too alarming. Actually

it is like IRB Invit getting a wealthy co brother in law.

C. Of course risk on growth/economy GDP growth/traffic diversion etc stay risks but they manifest

themselves in various ways in all equity/quasi equity like assets.

D. IDAA and Surat getting out is a dampener but a known fact from day one. The other assets and

potential new assets will surely kick in and enhance / replace the contribution from them.

E. Do not oppose new asset introduction…oppose bad asset introduction ( more on this later ),

and oppose increase in debt headroom beyond mandated 49% ( they have stated that stated policy

is that 49% will be cap )

Thanks for your detailed reponse. Find enclosed my view on various point

A) I agree that they can technically acquire assets with debt. New assets would provide IRR of 12-13% which funded with 9-10% interest would distribution accretive to unitholder. However, if the current units are trading at yield of 18%, would it not be better to buyback units and get than to acquire 12-13% IRR assets? I know that current regulation does not permit debt funded buyback.

Secondly, we also need to take note of moratorium exercised by company even with such moderate gearing. In case company use full permitted regulated leverage, may have adverse impact on rating, in my view, hence higher debt cost and lower NCDF from new acquisition.

Thirdly, please also look at track record on new assets acquired in past. Only one assets acquired post listing i.e. Pathankot Amritsar, performance is not great in last 2.5 years. One get better idea if one read valuation reports over period to get more insight. Partially one can explain it by external environment, but still it is way behind original expected expected cashflows.

Fourthly, we also need to see track record on distribution. The company has not been able to manage the distribution and it has gone down substantially in line chellanging business environment. So that may also pose chellenge to raise new unit capital in my view.

With this background, I find value secretive new acquisition may be difficult unless the listed units get improvement to make yield which move in range of IPO of InvIt.

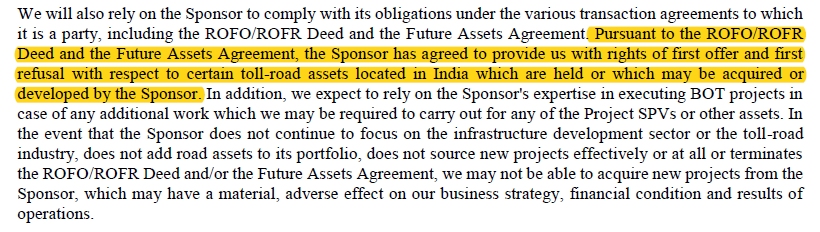

B) On working with GIC, it is not question of wealthy brother in law, but kind of unfair treatment to existing investors in IRB InvIT. IRB InvIT trust has first right of refusal on assets of IRB completed road assets. When IPO came, the investor thought about growth coming from IRB completed assets. One may go through old presentation after IPO.

IRB management was involved in managing the InvIT as sponsor and they could not mobilise the required money and than IRB did deal with GIC for Private InvIT. This is what fell as a concern for existing unit investor.

Find enclosed extract from Risk factors (Page 38 of Offer document of IRB InvIT)

C) I agree with you. These are business risks. However, the diverse assets over different region could have reduce volatility in my view. I may be wrong.

D). Agree that IDAA and Surat exit date was known. However, at that time, investor thought that new assets acquisition/ improvement in collection from existing assets would compensate for loss of revenue. That has not materialise and hence unit price decline materially.

E) Respect your view about supporting new acquisition. I have explained my rationale for opposing new assets already in point A.

1 Like

Thanks for your valuable inputs.

In fact I invested at 36 considering above known uncertainties of a Toll Collection business. I reviewed the other Invit/Reit available and felt that there was hardly any capital appreciation headroom .

All the known uncertainties of IRB Invit has driven such a discount in unit values and somehow I got tempted at value less than 40. I a cautiously optimistic for a new project being on boarded by management before the other 2 leave the portfolio. In fact if management is able to secure this with debt (their cost should be less than 8% considering AAA rating) , I have a feeling that Unit price is likely to reach 65-75 range.

Pl advise implications of Repurchase if allowed by Sebi. How that will be value accretive as existing cash flow funds will be utilized for same?

I doubt Sebi will allow Debt for repurchase.

Thanks to the members for their views as they have helped me a lot in my current investment and other options like Indi Grid/Reit.

I think SEBI would allow capital return to be used for share buyback. (may take a year or two to get approved). If IRB judiciously uses it for open market purchase of units, this would definitely push the Unit price up.

Agree ! Existing cash flow used to buy units are also fine…to an extent…This will be based on an individual’s own appetite or investment/consumption requirement

Hope this quarter we have good numbers. Invested last quarter with avg 37 and stock has given 25% capital appreciation along with dividend.

If anything on new project comes , stock can get a fresh push .

Q3-2021 results were released today and appear to be decent. Distribution of Rs. 2.5 announced for Q3 - 1.80 as interest and 0.70 as return of capital.

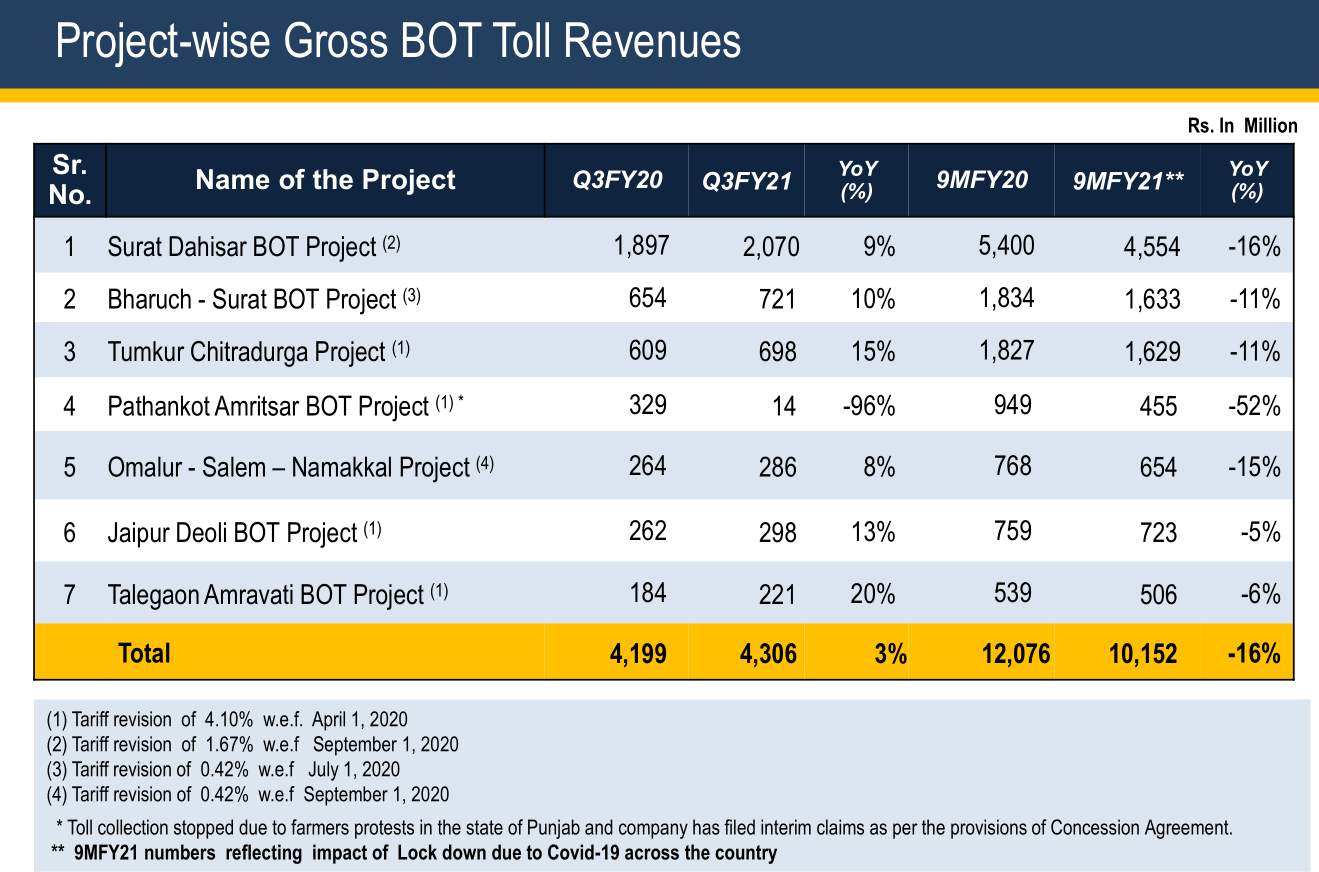

Good news is gross toll collection is above pre-covid levels now:

Results link here: https://www.bseindia.com/xml-data/corpfiling/AttachLive/f2be2ae7-f40c-41ac-b5db-f1e8e061d812.pdf

Investor presentation: https://www.irbinvit.co.in/wp-content/uploads/2021/01/IRB-InvIT_Corporate-Presentation-Q3FY21.pdf

Link to concall audio recording: Researchbytes.com

Disc: Invested

2 Likes

Thanks for sharing the information and I remain invested considering the current results and management commentary. Only eagerly awaiting New Project announcement so as this share reaches its book value.

Invested heavily.

Where did you get this data from? Also, by any chance have you updated this sheet as-per latest available information?

Thank you.

I quickly went through the investor presentation. Looks like they have been distributing ~10 rupees per unit for last many years. I understand that the earnings are subject to the vagaries of the political system, protests and such like, but doesn’t the INVIT price seem stupidly low, even at current levels, specially given the very high distributions? It is available at a dividend yield of ~20%.

Disc: Studying, not invested.

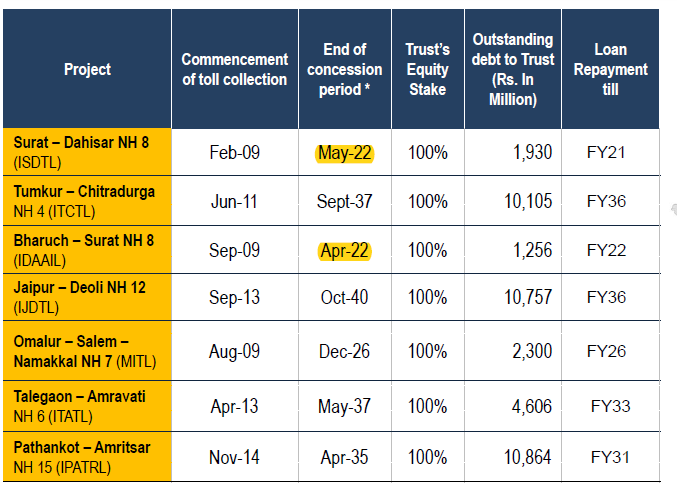

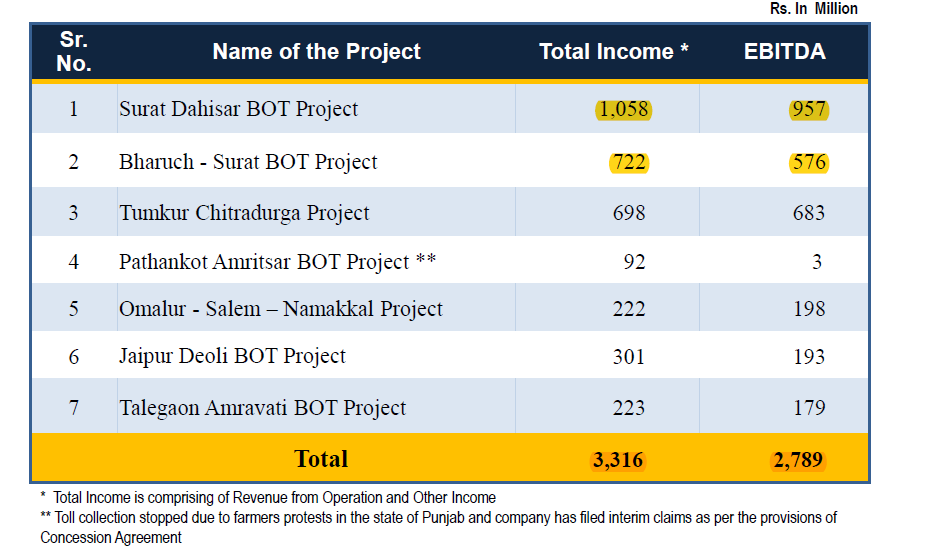

Please read the full thread. Note that nearly 55% of EBITDA Rs 279 Cr is from Surat Dahisar and Bharuch Surat Highway. Both are ending some time in FY23. Market is concerned with sustainability of distribution of cashflow post FY22. There are no addition in assets (except one Pathankot highway) which is also kind of put uncertainity of long term prospect of the company. Hence, please do more work on evaluating this risks in my opinion,

Discl: I am investor and IRB InvIT and my view may be biased. Not a SEBI registered analyst. Not advising any investment action.

6 Likes

One point worth noting is that while the Surat Dahisar cash flows will stop from May 22, the loan and interest for this BOT will stop in FY21. That implies (i am guessing) that for the next one year they will have additional cash flow that they could use to acquire assets. Not to mention, unlike Indigrid, which is at it debt limit of 75%, IRB debt/equity is 0.27:1. So, from an optionality standpoint, they have the balance sheet strength to definitely acquire more assets. Disc: invested from lower levels than CMP

Sir, in my understanding, 90% of NCDF distribution mandatory, unless they time asset acquistion, same has too be distributed. They are hybrid and management has limited option to hold on cash. In case, they find attractive opportunity, they can do right issue/preferential. Also, given performance only acquisition after IPO (Amritsar Pathankot highway) and handing over assets from IRB to private InvIT promoted by GIC, I would rather like to them distribute cash to investor, develop market confidence in IRB InvIT (which would reduce discount to NAV for units in secondary market) and show strong performance growth in remaining assets. This would assist them to get yield expectation in range of 9-11% at which level, it would make sense to acquire new assets with debt funding and improve IRR. When the units are traded at 18% yield in secondary market, it would be better to buyback then to deploy money in 12-13% yielding infrastructure assets in my limited understanding.

2 Likes

I invested heavily in November around 37-38 and I am optimistic with future prospects of this Invit. Got two distributions in this period, 1.8 and 2.5 and remarkably the Invit price captured the adjustments and is now around 54. Any political event is just a postponement of revenue and should not be a concern for long term investors.I feel that Invit price is likely to come around 65 by the time of next distribution and if Invit is able to distribute 2.75 or 3 market will push it to its NAV around 85. There is an opportunity of another 50 % appreciation for investment from current rate and dividend yield of 8-10 percent is likely to be assured by rising volumes and toll charges going digital. Invit has made significant saving considering fall in interest rates last year. Any new project coming to Invit in 6-9 months can be the last gamechanger and Invit price can go upto 100 as market will gain confidence in Managements prudence of taking new asset just in time and perhaps at lower interest rate of approx 7 percent. Additional projects taken after 2/3 years can guarantee longevity and yields in 8-10 percent range will pull more investors considering low interest regime.

Views can be biased as I have invested significantly based on above assumptions and my bench marks are Bank FD-Other AAA rated instruments. Cashed out of my equity positions and realligned my Portfolio to dividend stocks/invits. Currently investing in IRFC on every fall