Good efforts but oversimplification in my understading. I would appreciate on what basis you get Rs 10 for 10 years? One has to look at cashflow from underlying assets and growth pattern in same. In couple of project, the concession agreement is over 20 years, so one may assume cashflow over longer period.

While it is correct, that there no terminal value at the end of concession agreement for assets, but still one has to put efforts to project growth in traffic, expected increase in toll charge per vehicle and debt repayment for various SPV to get some idea about IRB InvIT cashflow.

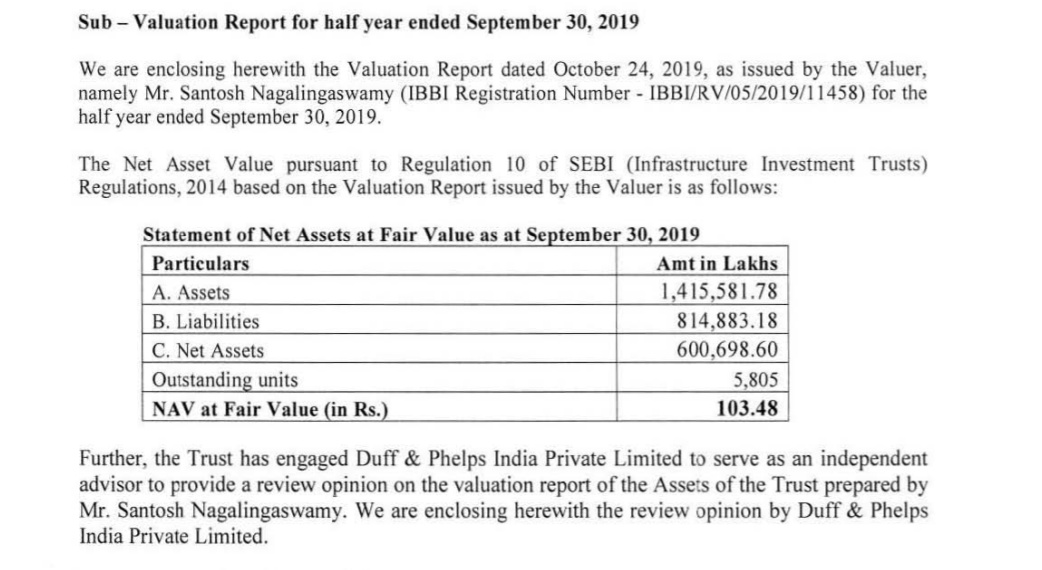

As per the latest valuation report, (September 2019), the NAV of unit (again based on assumed free cashflow, which has not materialised in past and one shall take of note of same) is around 100 per unit.

In my limited understanding, the major issue faced by IRB InvIT is management concern. Transferring assets from IRB to another InvIT promoted by GIC (Singapore government investment company) not gone well with existing investors. In addition to under-performance from new asseets (Deoli Jaipur and Pathankot toll assets) have also created concern among investors mind.

While one can become extra conservative and simplistic, we would get solution which would be far off from reality.

InvIT is structure in a way from cashflow that dividend would come only after repayment of loan which is very large. So, while your approach to simplify working is appreciated, the outcome may materially vary (on either side) if the concern for managment are not addressed.

In last 3 years (12 quarters) toll collection from various assets owned by IRB InvIt has shown very good performance (I have complied this information from various presention by InvIt over the period of last 2.5 years of listing).

| Tollection collection details |

|

Q3FY20 |

Q2FY20 |

Q1FY20 |

Q4FY19 |

Q3FY19 |

Q2FY19 |

Q1FY19 |

Q4FY18 |

Q3FY18 |

Q2FY18 |

Q1FY18 |

Q4FY17 |

Q3FY17 |

|

CAGR Q3FY20/17 |

| Gross Toll |

Rs mn. |

4,199 |

3,805 |

4,070 |

3,950 |

3,928 |

3,669 |

3,822 |

3,774 |

3,828 |

3,206 |

1,922 |

3,441 |

2,599 |

|

17% |

| Surat Dahisar Project |

Rs mn. |

1,897 |

1,704 |

1,799 |

1,787 |

1,724 |

1,605 |

1,655 |

1,687 |

1,687 |

1,468 |

893 |

1,475 |

1,114 |

|

19% |

| Bharuch Surat |

Rs mn. |

654 |

577 |

603 |

604 |

578 |

538 |

562 |

580 |

569 |

510 |

293 |

500 |

372 |

|

21% |

| Tumkur Chitradurga |

Rs mn. |

609 |

588 |

629 |

601 |

635 |

613 |

628 |

598 |

591 |

556 |

323 |

543 |

401 |

|

15% |

| Pathankot Amritsar |

Rs mn. |

329 |

286 |

335 |

293 |

319 |

294 |

313 |

282 |

313 |

11 |

0 |

271 |

238 |

|

11% |

| Omalur Salem Namakkal |

Rs mn. |

264 |

250 |

253 |

248 |

249 |

227 |

236 |

219 |

222 |

206 |

117 |

193 |

149 |

|

21% |

| Jaipur Deoli |

Rs mn. |

262 |

231 |

265 |

238 |

247 |

231 |

260 |

249 |

285 |

316 |

207 |

311 |

223 |

|

6% |

| Talegaon Amravati BOT |

Rs mn. |

184 |

169 |

186 |

179 |

176 |

161 |

168 |

159 |

161 |

139 |

89 |

148 |

102 |

|

22% |

While the growth in Traffic has slowed down in last 12 months (and mainly came from Mumbai Ahmedabad assets which would soon given back to NHAI on completion of concession agreement), There is possibllity of growth in underlying assets in my opinion. The managment really need to improve perception (by way of purchase of more units etc) and improve execution which could change perception of market.

Discl: My view may be biased due to my investment. Not Sebi registered advisor, Not a recommendation, Investor shall conduct their own analysis before taking any decision.