“they are just plain lazy / incompetent” is what I think they are.

Also raising equity is opportunistic of them as market price is below book value, so don’t mind diluting unit holders

“they are just plain lazy / incompetent” is what I think they are.

Also raising equity is opportunistic of them as market price is below book value, so don’t mind diluting unit holders

When market price is below intrinsic value that’s when you shouldn’t dilute cause you are giving away units at a discount.

I think You should look to raise at premium not discount.

IRB Public InvIT receives offer for 5 Toll assets from unlisted private InvIT -

Finally some acquisition plans on horizon.

This sounds interesting.

Hope these acquisitions (if any) are done at arms length.

I am always sceptical about inter-group deals

Yes, at last some development in assets aquisition. However, today’s price reaction negatively is danger signal. Hopefully assets are acquired at competative price, at right valuation and ensure good unit distribution. HERE IS TEST FOR INVESTMENT MANAGERS OF IRB INVIT.

Can you share information source?

Filed with exchanges.

68577efd-5937-43e5-a135-dd74a58346ee.pdf (352.1 KB)

Till date IRB INVIT has evaluated 32 assets, 2 has been acquired. (Orginal assets were 6, 2 completed) One of the added assets is Amritsar Pathankot… everyone knows contribution from this asset. Another one is VK1 HAM asset.

Current one offer is preliminary and non binding offer. With extremely poor assets aquisition success rate… let’s see what happens.

I am thinking this one will go through cause seems like they want to give their private InvIT exit.

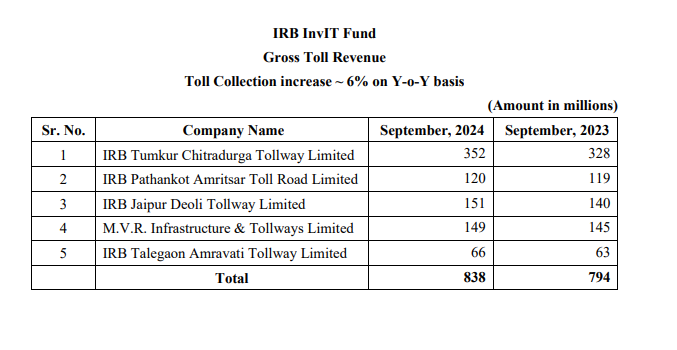

Just to put things in perspective. Here is the Sept 24 toll collection

If you go through this rating document by Crisil, these assets that are being offered have a

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/IRBInfrastructureTrust_October%2016,%202023_RR_329854.html

revenue of ~Rs 921 crore in fiscal 2023 and ~Rs. 425 crore in first half of fiscal 2024.

File_1731671507911.pdf (986.0 KB)

This is official filing by IRB Infrastructure…

End of day…unit distribution per quarter is key for retail investors. All these depends on right assets at right valuation deal. Let’s see.

They are mentioning the 5 assets at 15,000 cr Enterprise value !!. Irb invits EV is (rough calculation): Market cap of 3,366 cr + borrowing: 3000 cr= ~6400 cr EV. Looks like Irb Invit will have to do significant capital raise to buy these assets.

Is my understanding correct.

Debt to AUM is around 30%, back of the envelope calculation tells me they would have to raise atleast 5000-6000 crs through equity and remaining through debt to remain AAA rated.

I doubt that they can take all the assets in unless it’s at steep discount, maybe it will be in phases.

This excercise however highlights a critical flaw, that This InvIT can only acquire assets from private one/sponsor, regardless of market opportunity. Doesn’t matter if it threatens the viability of it. (Q1 25 they alarmed that remaining life of projects is below their threshold). Reducing investment manager to rubber stamp.

This is also the problem with powergrid InvIT, it’s been in freefall too. Their sponsor treat them as cash grab.

Only InvIT with value based market wide acquisition has been indigrid. (They started with transmission and now in renewable and BESS too)

FII sold 176000 units, small quantity from their large holding of @ 2 Cr, resulting in to @ 2% drop in unit price. This is exchange filing.

Dangerous situation for retail investors.

File_1732606470684.pdf (596.3 KB)

If the interpretation is that further FII selling will leads to further correction, how can this be a dangerous situation for retail investors? Its an opportunity to buy at much lower levels.

The risk for any investor in this stock is the company’s inability to maintain the DPU at Rs 8 p.a. and not the FII selling.

FIIs are much smarter, they foresee likely reduction in future DPU.

Between Jan-2024 and March-2024, FII reduced their holdings significantly in HDFC bank. They sold 29 cr shares for a total of Rs 42954 crore (Avg price per share = Rs 1468). I dont think we can conclude FIIs are super smart. They are not purely value investors but act more like momentum investors.

Indeed - this is my conclusion too.

The original thesis has been turned on its head… inspite of getting advantage of mothership - IRB InvIT and Powergrid InvIT are mere slaves to its masters.

Any ideas on why IRB went up pretty well from its low recently?