Normal rise towards DPU time is several weeks out…atleast 6-7 weeks away. So, this does not look like the normal rise around DPU time. Have they figured out how they will finance the enmasse block of assets offered? Someone knows something because this is a certain trend reversal, after months of being in reverse gear

1 Like

Possibly sponser and investment manager of IRB INVIT (IRB INFRA owner) realised that their image is getting tarnished due to extremely poor performance of IRB INVIT. This can be highly negative to IRB Infra for future growth and fund rising. They may pass on assets offered at such valuation which can enhance IRB INVIT’s future valuation and improve open market unit price.

My update on IRB Invit…

I have registered for an earning call for the subject event. I did register for the same and also joined the conference. I did registered by #1 in the Q & A session just after the coordinator prompted for the same. Unfortunately, I could not get a slot from you to ask questions in the entire conference. Nevertheless, I am now writing my questions which I expect your investor services will respond to. After my questions, I am also giving you my and my family’s IRB INVIT holding.

Question - 1

Good morning sir.

Thank you for providing me with this opportunity.

My first question is on the Capital return component of DPU. Capital return till date is Rs 20.20, including current quarter. My understanding is that the unit issue price was Rs 100 of which Rs 20.20 is returned. Current quarter distribution of Rs 2 consists of Rs 1.02 capital return and Rs 0.98 income generated from assets. Is my understanding correct?

Question -2

My second question relates to toll collections. My data compilation shows that,

1) Total toll collection in calendar year 2023 was higher by 9.62% as compared to calendar year 2022.

2) Total toll collection in calendar year 2024 was higher by 5.01% as compared to calendar year 2023. This is a sharp drop of 4.61%.

These data are for 5 currently operating toll assets only. Considering @ 4% annual rise being permitted for each year, toll collection is up by just 1.01% higher. This is something fishy.

Now, my question is,

A) Is there any mechanism to verify pilferages in toll by way of local staff milibhagat with toll user?

B) If yes, Is that mechanism completely automated with live updates to project managers?

C) Or there are some other loopholes by which toll collection gets lost. Do project managers analyse toll collections and take remedial actions? If yes, what action was taken?

2 Likes

A smaller number of vehicles could explain the lower than expected toll collection.

Since almost all tolls are collected via Fastag there is very less chance of revenue leakage.

How will proposals impact the toll collections for all the highway INVITs ?

Annual, lifetime toll passes for use on national highways

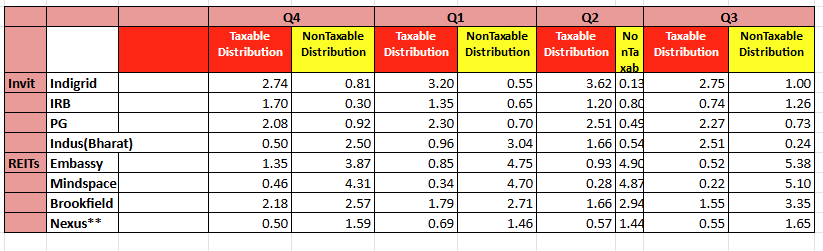

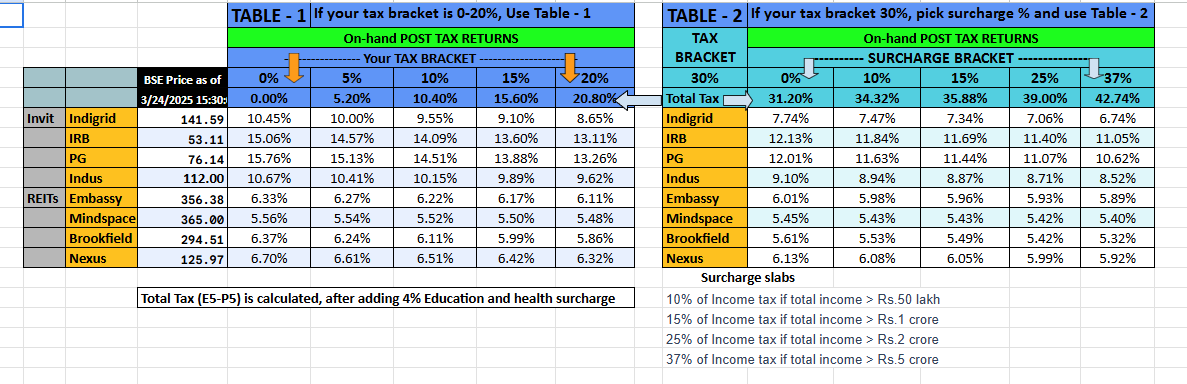

Here is the latest Yield calculations, if you have to buy the units as of closing prices today. It is the same running 4 qtrs based (3 quarters of this FY plus 1 Q from last FY, as of now)…I am also attaching the underlying calculation table of DPU…Qs/Comments are welcome, as always…

PS - Not claiming this to be perfect calculation. Taxation is a complex subject and hence do your due diligence…

3 Likes

Every day, is a new 52 week low, for IRB…with that, the yields (based on past DPUs) have become a mouthwatering 15% at pre tax, 12.13% for someone at full tax 30% (31.2% including education and health surcharge) but without any surcharge…

where is this heading?

For comparison…5-5.5% is the yield for tax free bonds in Secondary market

AAs…roughly 11-13% (if lucky, the odd one with near term maturity around 13.5%) in most secondary market instruments (again fully taxable)

AAAs - roughly 7.5-8.5% in most secondary market instruments (again fully taxable)

PS - At the end of the day,this is all about Management quality and proactiveness. When you compare with Indigrid, that is where the difference lies. IRB management is not forthcoming and no one has a clue on how they will finance the new projects and what will be its effect on the DPU…everything is taking its own course and there are no prompt disclosures, keeping investors informed.

2 Likes

Both PGinvit and IRBinvit are becoming compelling buys for patient long term investing ..I remember Indigrid coming down to Rs 82 or so after listing in 2017 / 2018 before rallying..

interesting situation..

1 Like

Pl read my comments in PS about management quality comparison…

1 Like

with today’s fall and yet another 52 week low, IRB is within breathing distance of the yield of PG

Has anyone tried reaching out to the management to know, how the new assets will be financed? My attempts to reach out to them have yielded standard answers ‘will update in stock exchange filings’…

Discl…averaging down, but with less conviction

2 Likes

My assumption is DPU is going to go down, because of financing debt and dilution for new assets that’s on horizon, and it’s gonna be huge. thus market is re-pricing the Unit price.

so I suspect this 15% yield is short term illusion, it’s gonna readjust to 10-12% (or even 8-10%) on current price. There’s no other way I can make sense of this.

if that’s the reason I would prefer if they go route of rights issue than QIP cause imo that would mark the bottom and end this wretched over hang.

Disc. Invested but cautiously optimistic about new assets.

Invits acquire assets to increase or maintain DPUs…new assets will also generate additional cashflows while diluting. so DPU will not go down

1 Like

Last Q3 DPU distribution was Rs 2 which contains one of the component RETURN OF CAPITAL, Rs 1.02. This is what you invested on day one at Rs 102, till time they have returned @ Rs 20 or so. So DPU is eating away your capital and we are calculating DPU yield.

Does anyone has other views other than above? Please do respond.

2 Likes

If you assume that cash flow that new assets will bring is higher than financial liability part. Which I don’t think so.

Especially If those new asset aren’t as matured and you front load the costs. Same happened with Brookfield for a while.

every year they returned 8 Rs for last 8 years…you should not buy when it is overvalues - my avg cost is less than 50 (there were times yields were close to 16% for AAA rated trust with 12 year visibility of cashflow)…you can expect IRR to be 12% even at inflated prices

They cannot take debt more than 70% (ie D/E cannot be > 0.7) due to regulations