Is swaping IRB InvIT (Rs 62) for Bharat Highway (Rs 113) a good trade at current levels for mid-long term?

Especially when revenue stream from annuity model is superior vs IRB’s toll collection

Is swaping IRB InvIT (Rs 62) for Bharat Highway (Rs 113) a good trade at current levels for mid-long term?

Especially when revenue stream from annuity model is superior vs IRB’s toll collection

What is preventing me from making the switch now ? (my 2 cents…someone else’s view can be different)

But isn’t annuity based income is interest rate sensitive? Wouldn’t it go down with interest rate ? Am I missing something.

Management themselves said so, though they tried to assure investor that they would hedge it with loan interest but they can’t achieve 100% hedge as of now cause invit has little loan.

Same here, especially last concall sounded alarming to me, like they were panicking that they couldn’t add new assets.

It’s big part of my portfolio as well since that kind of returns at AAA rating sounded like no brainer.

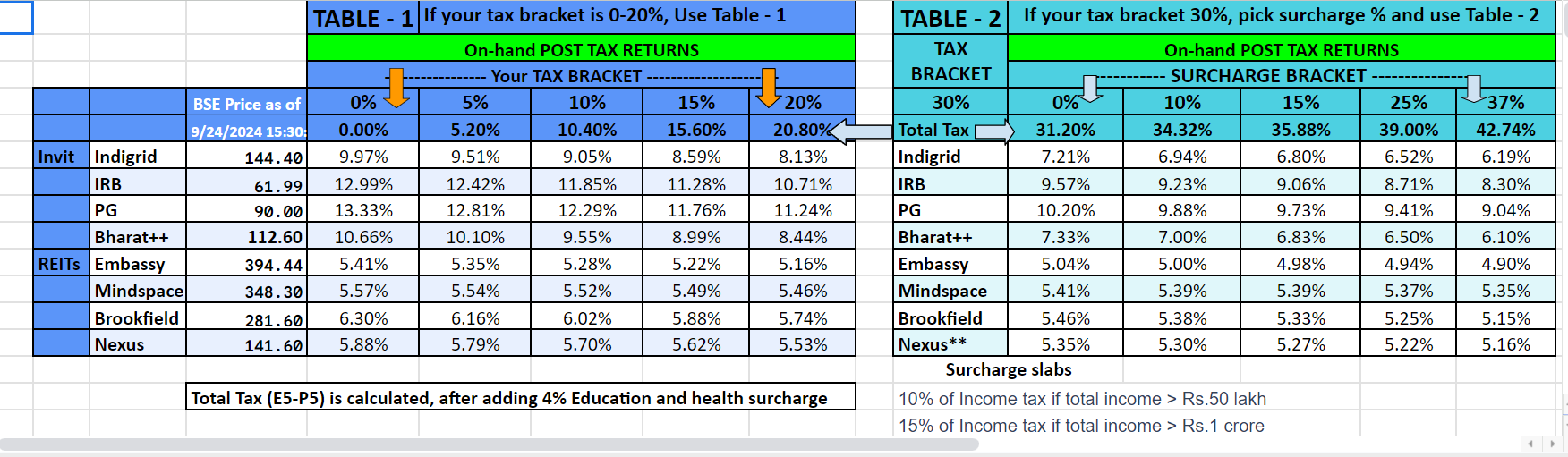

I think we need to differentiate rating of InvIT trust from InvIT unit investment. The AAA rating is to debt taken by InvIT to finance assets and they have supeiror claim over InvIT unit holders. InvIT unit is broadly comparable to equity. Do we consider credit rating of debt company and yield of debt paper as quasi equity return? No, in my view. Similarly, investor in InvIT is taking business risk and hence can not consider as debt investors. The interest on loan of IRB InvIT is around 8% which is equivalent to AAA credit rating paper for debt investor. Yield of 13-14% is not certain and would undego change with toll change, traffic change, interest change, asset termination due to ageeement and foced event (likr Pathankot road closure in farmer protest). The additional 5% yield to invIt investor is to assume all other listed and many unknown unlisted risk. This is my view and may be wrong. However , would advise members not to consider credit rating of InvIt trust and current yield on InviT unit as same have differnt risk profiles.

ofc, it’s as risky as equity everyone knows that, I thought that was common sense. When I mentioned AAA it was shorthand for adequate liquidity and solid assets. wouldn’t write down every redundant detail in every comment about InvIT as an asset class.

How much is the dividend per share for this INVIT?

As per management commentry in last investor call, they have guided Rs 2/Unit/Quarter. However, this can not be taken as granted as it depends on toll income generated from assets. The current downward price movement indicates likely miss by @10 Paisa in current quarter. The downward price movement is also due to inability of management to secure / add good income generating assets.

The only saver for IRB INVIT will be adding new cash generating assets

(Same is the case for PG INVIT)

Somehow Indian INVITs REITs are not getting it’s due from broad investor base

Disc - invested in both

PS sitting on ~7% and ~40% capital loss in IRB & PG INVIT respectively

Is the dividend directly propotinial for indigrid as well?if that is the case why would an investor invest in these trust?

My thesis of investment was that share prices would rise when intrest rates fall as the cost yo match the yield or lower bank intrest rates

It is that time of the year and the the DPU is the same old 2. I wish that the management gets serious about project addition and DPU increase but during my attempts to reach them, they were coming with the same old trite phrases’

“Declared 2nd Distribution of Rs. 2 /- per Unit, for the financial year 2024-25. The distribution will

be paid as Rs. 1.20 /- per Unit as Interest, Re. 0.57 /- per unit as return of capital subject to

applicable taxes, if any and Re. 0.23 /- per unit as exempt dividend.

Please note that October 31, 2024, has been fixed as the Record Date”

Expenses seems to have dented Total comprehensive income

https://www.bseindia.com/xml-data/corpfiling/AttachLive/11d48142-0a88-4434-a286-c34de82a9852.pdf

Here is the latest valuation report (for what it is worth !!)

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b993c356-3f97-489c-bcaa-681ddb82fa80.pdf

As usual, there is the farmers’ agitation and suspension of toll collection in Punjab. Even though, it does get compensated later, all these lead to delays. I would be curious to see what happened to the loss in toll hike delay, due to general election as well.

Disc…invested and cringing

Participated in Earning call - Q2/25 Earning call highlights.

Any one has idea, lets say I am holding 5000 units right now. What will happen to my investment (@ 62X5000 = 3,10,000) when there is no assets left with INVIT? Thus, price recovering to face value is distant possibility. It can go further down if no new assets added and old assets goes back to NHAI.

If DPU of Rs 2 per Quarter is sustainable and going to increase by Rs 0.25 after 3 years, then the current yield of 13.5% is attractive. Any comments?

Yes, it is attractive but market also looks at what is long term vission by ensuring assets aquisition.

Per latest valuation report, the NAV is tad above 97 Rs at a WACC of around 10%. Keeping 20% aside for possible aggressive assumptions we still get NAV of somewhere between 75-80. So no reason to sell. If there are no more acquisitions, they will keep returning the money as “return of capital”. And final payment should happen once last asset is handed back.

Disclosure - Holding and hence biased. Entered at a lower price a couple of years back

The current InvIT structure of IRB own 4 BOT and 1 HAM assets. So in case there is no futher asset additions, the trust would continue to distribute NCDF to unitholder. In case NCDF cashflow discounted value are higher than current market cap of unitholders, then unit holder would receive excess amount over NAV as dividend. In case the discounted value of cashflow is lower than current mark cap (due to lower traffic, frequent issue of farmer protest etc), and tenue of asset get over, the investor would have to write down undistributed capital outstanding at end of last assets and book loss. However, while there may be accounting loss, the likely loss of capital appear low probability to me.

Since listing in May 2017 to November 2024(including Sep24 quarterly distributon with declared but not disbursed), IRB has distributed Rs 68.35 per unit as distribution. Of these, nearly 71% portion came as interest distribution (Rs 48.35 per unit in agggregate), 28% portion came Capital redemption (Rs 18.88 per unit in aggregate) and 2% (Rs 1.12 pre unit in aggregate) distributed as Dividend. So, signficant portfion of cashflow are distributed as Non-capital redemption in form of Interest/Dividend and hence I see limited probabilty of cashflow based loss on investment.

I was in the call, must say you asked very daring questions and took them head on. Most analyst and those brokerage guys don’t ask daring question. They just punch their question, show it to employer and call it the day.

Keep asking these questions and press them on acquisition.

Thanks for your compliments.

I think these were concern in the minds of retail investors. Management shall prepared for such questions if they fails to deliver.

One thing IRB managers have failed to eloborate on conflict of interest

IRB group has another unlisted (pvt held) InvIT within IRB Ltd. This is well capitalised with FII funds. And somehow IRB InvIT has become an unwanted child

Also a small silver lining is that IRB can take aggressive route to add assets with debt financing when bank rates cool a bit

CC @Abhinav_007

Well, to be fair they have said many times there’s no conflict of interest as Private InVIT just serves as platform to develop assets, those assets don’t generate cash right now. they haven’t given distribution in long time. Of course, I am skeptic of them, why they need separate InVIT why not do it under the IRB developers but I don’t think Public InVIT will be interested in those assets. I think They are just plain lazy/incompetent. A few times they have also said because interest rates are so high IRR calculation on HAM assets don’t make sense, which is true but why not look for BOT assets ?

Also, yeah maybe they would acquire some asset after rate cuts but as we have seen InVITs and REITs keep raising equity capital even after having debt room, which has never made sense to me.