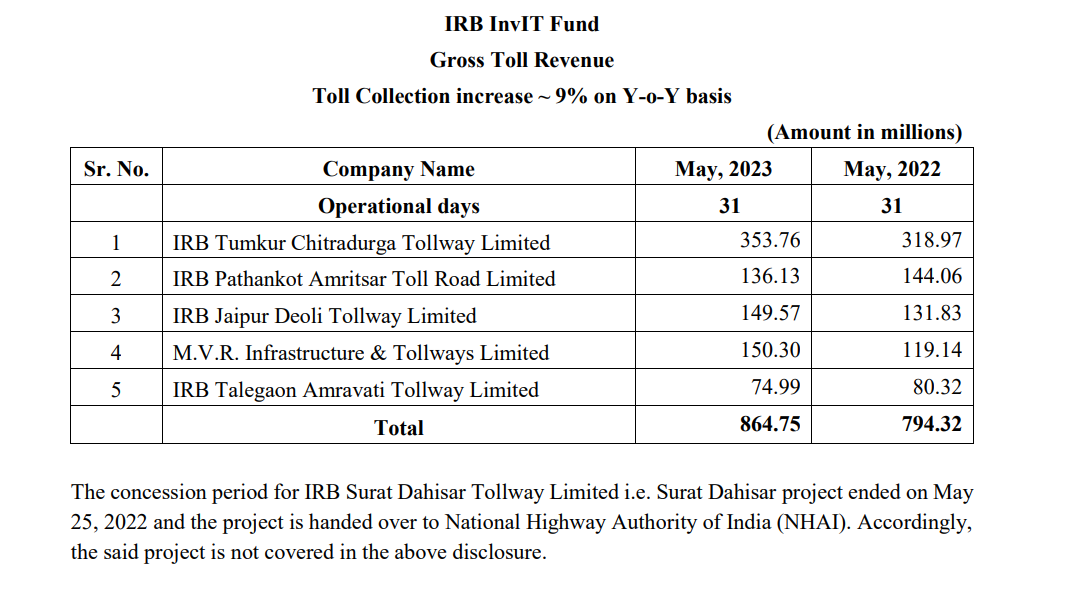

Another steady increase in monthly toll collection

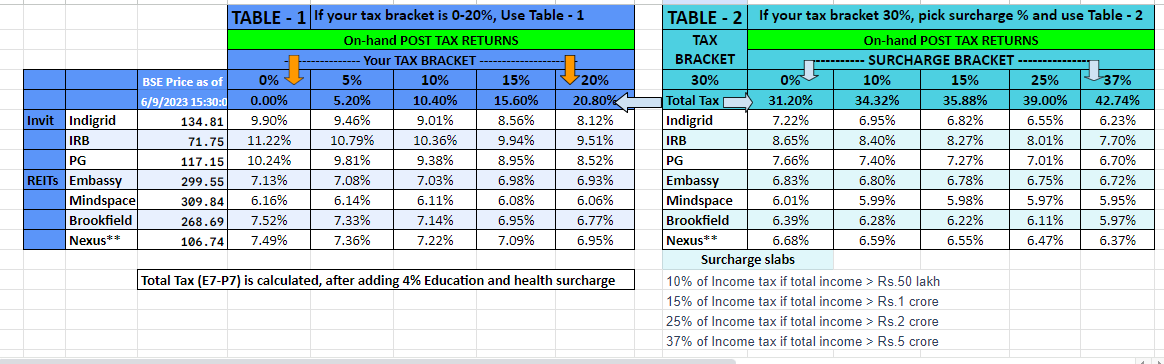

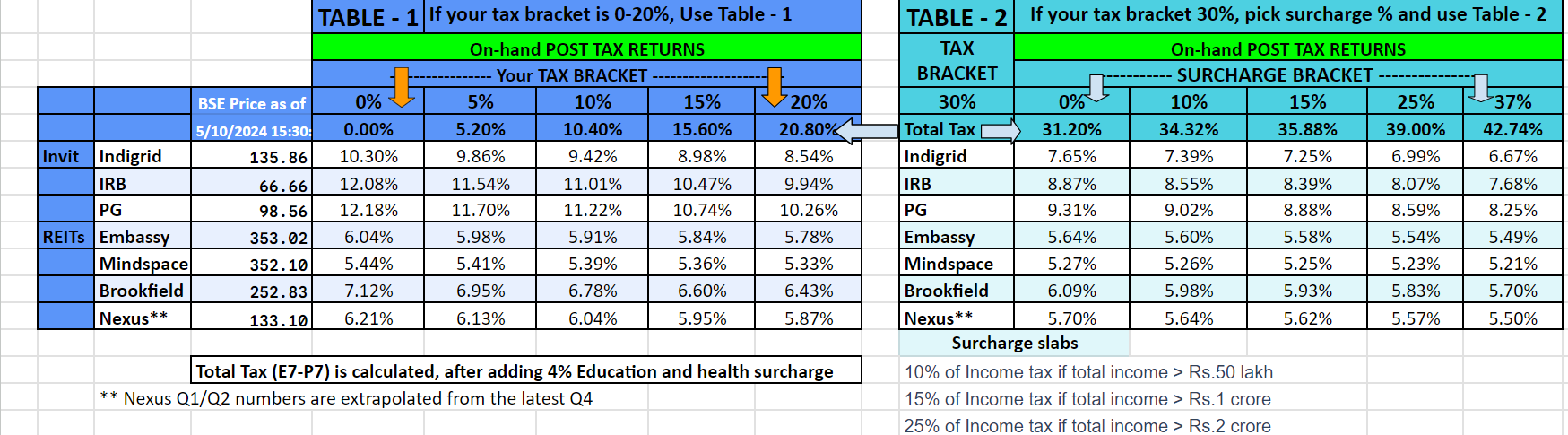

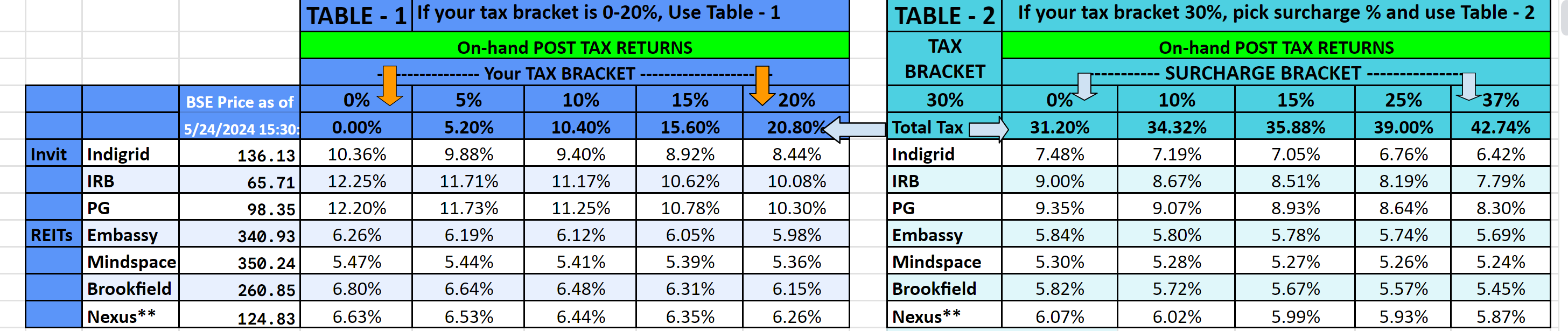

Wanted to give a comparative view of yields across listed REITs and Invits, on the prices as of 9thJune 2023 (earlier I had shared it on 2nd June. There was a minor error in DPU of PG and I fixed it…won’t change anything drastically and it is a 2nd decimal correction), and this is based on the rolling 4 quarters DPUs …Obviously, yield will differ for your tax bracket and hence pick the right slab below…

REMEMBER that these are POST TAX, ON HAND Yields for the Invits/Reits, for the price shown. **Nexus yield is based on projections gleaned out from various interviews, during IPO.

IRB obviously has been topping this yield chart and it has been that way for a while. Steady performance in toll collection, keeps the hopes alive in price action. Discounting the fall in 2018-20, ever since the U turn, it has been a phenome of a one way ride but still below the initial listing price of 79 and IPO price band of 100-102

No surprises in DPU…Same 2 but the mix of 1.7 as interest will make it less attractive for folks with higher tax brackets. It was the same in Q4 last year but if this is the trend, the yield advantage will fizzle out, in comparison with Indigrid and PG

The Yield table is updated. Q1 DPUs are updated for all except Brookfield and Nexus, who are yet to declare. Remember that I compute this for running 4 qtrs

Hello @dd1474, I came across your thorough questions in the transcript of the call and was wondering if you could provide your thoughts on the FY24Q1 results. Additionally, I’m curious to know if you think the HAM project is not performing well. I value your insights and appreciate any feedback you can offer. Thank you.

@saintsat

Thanks for your kind message. Q1FY24 for reasonably good. During Q1FY23, we had Surat Dahisar revenue for 45 days, which resulted in superior income. Now same being replaced by an HAM assets, but that contribute marignally in distrubtion. So other projects have performed better and hence InvIT could distribute Rs 2 per unit.

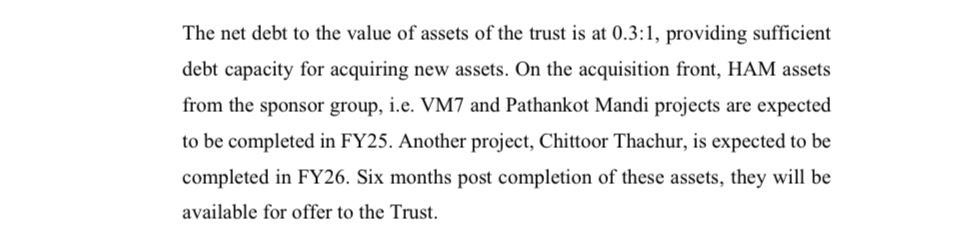

HAM assets cashflow are more like fixed income. Hence,like Fixed income assets, value of HAM assets would increase in case interest cash decline (resulting in lower discounting rate) and vice versa. So view on HAM assets shall be linked to expected movement in interest rate. Since, the management indicated improvement in guideance from HAM cashflow for FY25, I assume they anticipate decline in interest cost during FY25. The details for same are available on Q1Fy24 Con call trasncript form which I am enclosing extract.

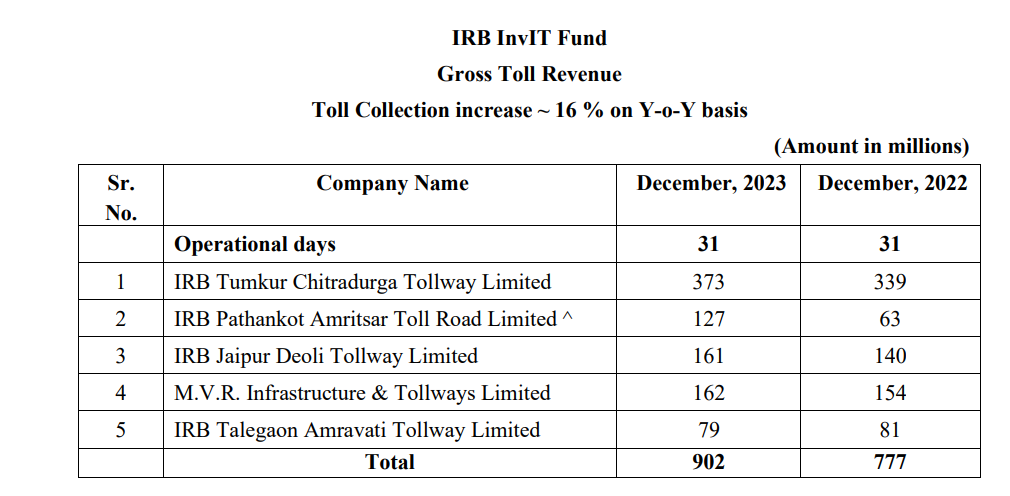

FY2023 was probably the best year for IRB InvIT due to higher WPI. With WPI stabilsing, the toll revenue growth would be driven mainly by traffic for 5 assets. Considering 5 toll assets with economy linked revenue, and One HAM assets which has fixed revenue, I find overall portfolio of IRB InvIT improved with HAM addition, as it would provide stability in case of economy downturn.

Disclaimer: My view may be biased due to my holding and may be worng as well. I may exit from investment without informing the forum. I am not SEBI reigstered advisor. I am not recommending any investment related decision.

Declared 3rd Distribution of Rs. 2/- per Unit, for the financial year 2023-24. The distribution will be paid as Rs. 1.70/- per Unit as Interest, subject to applicable taxes, if any and Re. 0.30/- per unit as exempt dividend.

February 5, 2024 has been fixed as the Record Date for the purpose of Payment

of this Distribution and it will be paid / dispatched to the eligible Unitholders on or before February 13, 2024.

PS - I was hoping that a slight uptick on Distribution will happen, from the usual 2 and the mix will also be better but it is on the familiar lines

Another quarter and another DPU of Rs 2…not much has changed and IMHO…this is causing a negative bias in the price. It has steadily declined now, over the last few months…

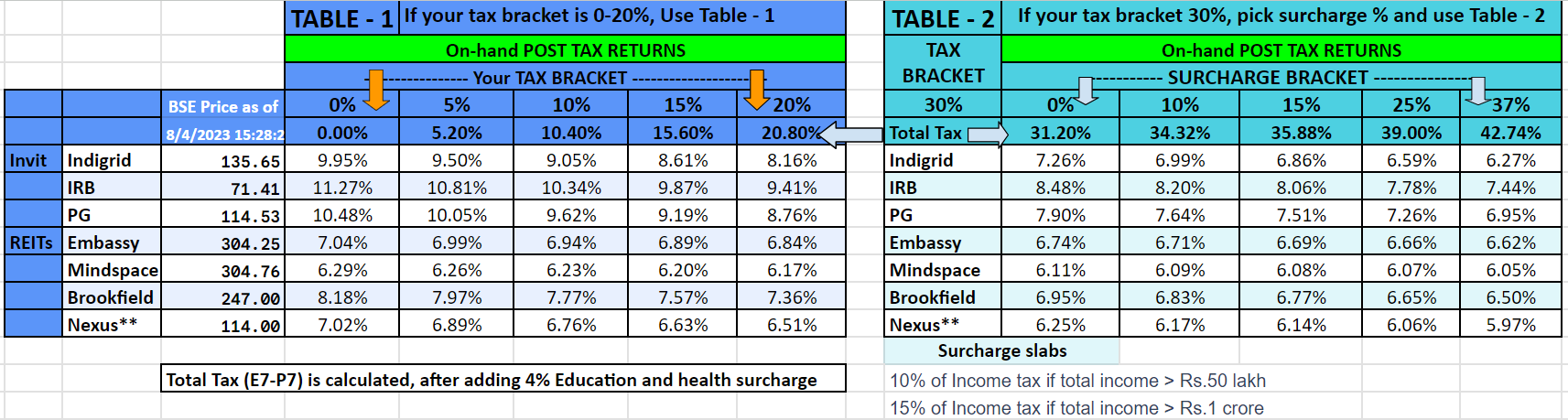

I have updated the yield table with the latest (whoever has declared Q4, it is there; otherwise, it is from last year Q4)…in Nexus, there is approximation since they have not done a full 4 Q year…as always, this is my calculated sheet…there can be errors and I am open to feedback

I think that means the assets would have to be returned back to the owners (Government) after weighted average of 15 years. Once the asset is given back, they stop getting any revenue from it. Typically, once an asset is returned, Infra trust would try and buy a new one. This period is also called concession period.

How this works is: The developer (infra trust) will develop the project (road asset in this case) and then they will take toll for those numbers of years (concession period), and once concession period is over, asset is taken back by the govt.

Hey do you know if there any issues with IRB invit management or with the assets they own? The price has been falling more than usual in the past few days and i was wondering why

Second, there is a new public listed InvIT, Bharat Highway InvIT which has only HAM assets and cashflow here is more stable. They also have a dividend yield of 11%.

Overall, IRB InvIT seems to be at mercy of its sponsor IRB infra and the sponsor also has a private REIT to distribute assets. I listened to Bharat InvIT first earnings calls and they seem to be aggressive in adding assets and have plans for around 7-8 assets in next 2 years.

Thank you for this insight Shiva. But in the IRB concall, they maintain guidance of Rs 8 for the year and also mentioned slight increase of cash from new HAM asset. If that’s the case the div yield before any taxes is as Kalyan mentions above i.e 12%. They have enough space for debt and the toll revenue would increase slightly over time. So why is it not good for invit price if the invit doesn’t take more assets in the near future? Is it cus there are other options out there that do it and therefore might actually provide a better yield? Sorry for the long question:smiling_face_with_tear:

There’s also the case of Deferred Premiums to NHAI which is putting downward pressure on share price.

IRB Tumkur Chitradurga Tollway (IRBTC) was supposed to pay a fixed annual premium to the National Highways Authority of India (NHAI) with an increase every year.

Due to lower toll collections in the initial years, NHAI allowed IRBTC to defer the premium payment from FY 2014-15 to FY 2024-25.

Repayment of deferred premium:

The deferred amount will be treated as a loan and needs to be repaid with interest at 2% above the RBI bank rate.

Currently, the outstanding deferred premium with interest is around ₹538 crore (or a little more).

IRB InvIT will repay the dues when they have enough surplus cash.

Impact:

Deferring the premium helped IRB InvIT improve its cash flow in the initial years and distribute higher payouts to unitholders.

However, this is a liability that needs to be settled eventually, and it can put a strain on future cash flows.

I am not saying that they will decrease the dividend but it would be hard to grow dividends in long term without adding assets. Even road assets have risk like decrease in traffic, sudden increase in maintenance costs or natural calamities. If you keep adding assets which are DPU accretive, the concentration decreases and the overall company is more stable.