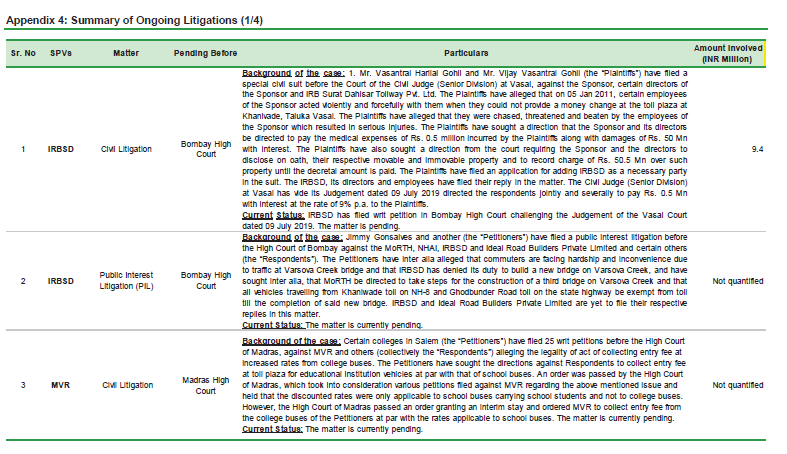

This appear in part of assumption. If you go through Annexure 4, there are 15 disputes listed in the annexure. In case the dispute is related to time when the assets where not owned by IRB InvIT, the cost or consequence of same would be applicable to orgnaisation which was owning that assets. So IRB InvIT shall not be concerned for old event, except that issue being so signficant that the concession agreement itself being set aside. In that case, IRB InvIT has already paid the owner of Toll assets, with no assets to recover toll. While, it can pursue in court to recover the amount paid to owner, that would be time consuming and not what investor has invested for. So there is risk if we look with microscope. However, even with Gsec, assuming no risk of interest payment, investor still run risk of present value of money, more relevant in current environment when inflation is going up. So every investor shall look at his/her own rsik appetite, return expectation, and profile before making any investment decision.

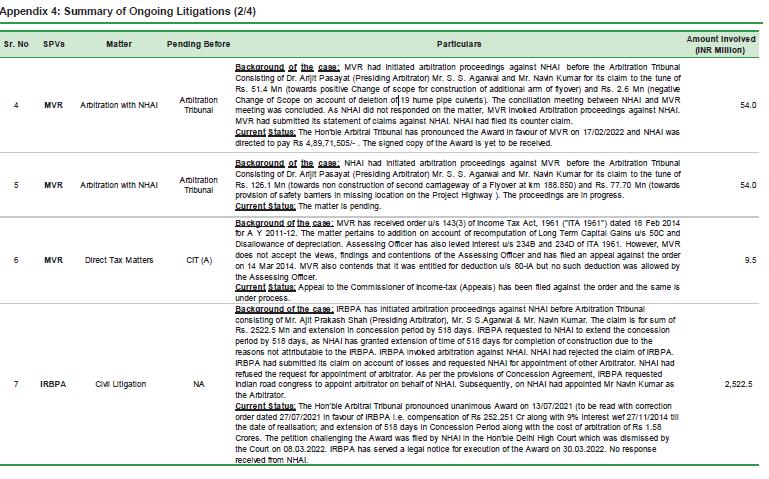

Of the 15 item listed, except Pathankot Amritsar Arbitration award against NHAI, decision on which has been in favour of IRB InvIT as per disclosure, in my personal view, none other issues are major. Please note that this is my understanding and it may be completely wrong. So, please read all risks carefully before making any investment decision.

Management avoided to give number in IRB Invit call and within few days spelt more details in IRB concall as most investors were asking for their approach wrt Public Invit. Raising 2500 cr for IRB Invit and the value accreditation for the new assets is a key monitorable now and we look forward to the Concept paper.

Management has atleast provide a complete clarity and roadmap and transparency in their forward approach. New assets are just a matter of time and I await levels less than 53 for adding more.

Double digit hike in Toll rate

Four of our project assets i.e. Jaipur-Deoli, Amritsar-Pathankot, Talegaon-Amravati and Tumkur-Chitradurga have received a revision of tariff rates at the rate of 10.16% which has been effective from the 1st April, 2022. The expected tariff revision for Omalur Salem project would also be more than 14% considering the provisional WPI for the March, 2022 month. The raw material prices have witnessed a steep hike because of the ongoing geopolitical tensions. Due to fixed price contract with the project manager for a period of 10 years i.e. up to FY30, we will not have any impact of this rise on our financials.

Guidenace for FY23 distribution

If you look at the current quarter numbers i.e. March 2022 quarter number and if we just take up balance 5 projects i.e. PA, JD, MVR, TA & TC, gross revenue from these projects (excluding the Bharuch-Surat and Surat–Dahisar) is around Rs. 200 crore and if we reduce the Rs. 10 crores of revenue share, the net revenue is Rs. 190 crore for the quarter. To annualize, if we multiply by 4 then we reach to Rs. 760 crores of revenue and increase by 10% for tariff revision and 5% for traffic growth on a conservative side, then we reach a revenue number of around Rs. 875 to 878 crore and Rs. 70 odd crores from the Surat–Dahisar project for balance tenure of 2 months, then we reach the revenue of Rs. 950 crore. After considering O&M costs of Rs. 100 crores then EBITDA will be around Rs. 850 crore, debt obligation including interest and principal is approx. Rs. 150 crores, the surplus will be close to Rs. 700 crores, Rs. 225 crores is the premium payable in Tumkur Chitradurga project. The NDCF will be around Rs. 475 crores which translates to around Rs. 8 payout to the unit holder in the financial year of FY23.

Medium term distribution guideance

If we look at last three-four years, WPI was very muted and we believe that this is the catch up effect and this will last for another 2 to 3 years. Still, we are not assuming a very high WPI even with 5% WPI and 5% traffic growth, if we extrapolate the current number itself, we should be able to maintain the payout of around Rs. 8 plus with a 10% revenue growth.

Discl: Invested in InvIT and hence my view may be biased. Not recommending any investment action. Not a SEBI registered advisor.

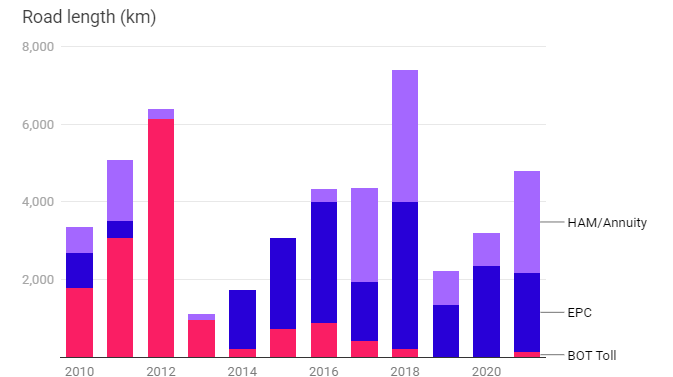

Not sure on IRR for a HAM project. Need more research. Done some research on HAM. But HAM (Hybrid Annuity Mode) is the way forward. Till now IRB Invit trust operate 5 BOT/Toll (Build Operate and Transfer) project. Current opportunity ,VK1 is a HAM project. recently NHAI awards most of the project under HAM.

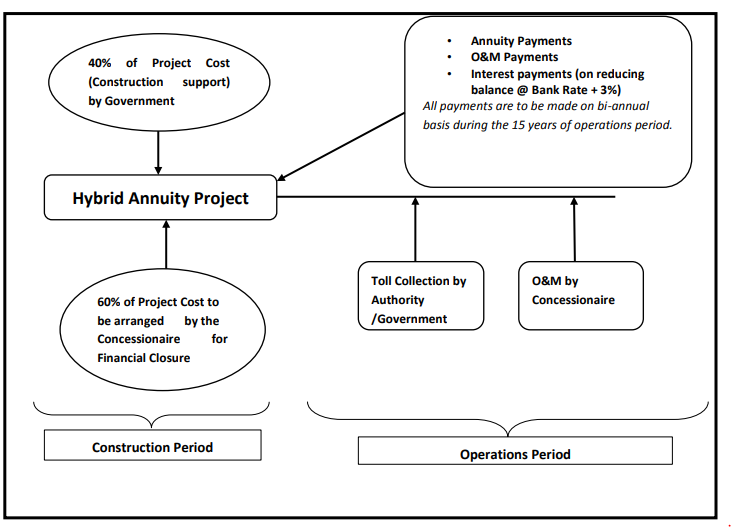

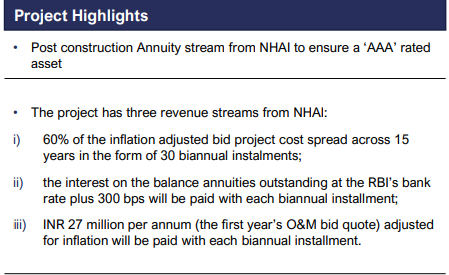

Good picture to understand various stakeholder and stakes in a HAM project

Based on the information shared, I feel there will be more revenue certainty in a HAM project and will only help in ensuring perceptuality of the instrument. Bridging of gap between current market value and Fair value is the capital appreciation I am looking for in coming years and 8+ distributions ensure a decent perpetual yearly yield.

The distribution will be paid as Rs. 1.201- per Unit as Interest and Rs. 0.801- per Unit as Return of Capital.

Two fold increase in revenue because of 42319 Lakhs arbitration amount is recognized but expenses are also recognized and hence no impact in comprehensive income…

At today’s price, if someone buys this invit and if the same run rate of distribution continues, it will be ~ approximately 14.29% pre-tax yield

From the Q1FY23 results, can someone please explain me the following:

Looking at their presentation, the Net Toll Collection number is: 287 Crs. Now when I look at their NDCF working the net cash inflow at the trust level has been shown only as 159.4 Crs.

How is this supposed to be read? I am not sure I understand the difference here. Any help will be appreciated. Thank you.

Hope you could listen as its easily available on youtube.

Management guidance of min 8 dpu is assuring and IRR of 12plus on equity in new asset. Also, their 50 percent funding of new asset by internal accruals demonstrates their conservative approach. Sponsor results yesterday were above expectations and the current discount from NAV is unwarranted as 14 plus yield on AAA rated instrument with inflation related annual increments.

Disc: Significant exposure from lower levels and small additions at 54.10.

8 dpu only with 5 assets. Many of HAM projects are ready for negotiated purchase in the next few quarters. They will have 7-8 asstes in next 2 years assuming if the new assets have IRR > 12%, DPU will only increase.

IRB Invit Board of driectors has approved the acquisition and will go to unit holder approval on sept. 5 and the acquisition will be completed by october.

June , July’22 toll connection news came out minutes ago in BSE

Steep rise in collection and it looks like traffic is getting back to normal. Also, easy to compare with prior year since Bharuch Surat and Surat Dahisar toll collections ended in March and May’22…if you drop the 130 odd cr that Pathankot Amritsar collected (for comparison, since it wasn’t there last year), even then, this is about 100 crore higher, in a month…

Slight drop in monthly revenues reflect a steady state of affairs and a price dip in market rate may give another addition opportunity for long term investors.

They seem to have valued the SPV at 377 Cr using 6.86% WACC (10.3% return on equity) which seems on the lower side. They have used a beta of 0.43 which seems low although I’m not sure about the source.

they have used a cost of debt of 7.2% which seems to be low. Their annual report indicates 7.25-8.15% and does not account for rising interest rates. Using 8% drops equity value by 8% and 8.5% by 12%. A few years ago they were paying 9%+

Using both a 12% return on equity and a 8.5% cost of debt, they are paying a ~20% premium on the assets and should have priced the asset at ~290 Cr

This is without the sensitivity to the income and delayed payments by the government. I’m not yet certain about HAM project revenue and inflation risks.

Historically, the valuation report for the other acquisition and half year reports seem to have over-estimated the cash flows and valuation. There is also the related party risk of buying from the parent. That said, the risk seems to be more return dilutive and not as much value destructive at current prices.

This is a problem due to low Corp Gov of Mhaiskars - they are beneficial onwers in both Invit and IRB - ideally invit manager should be high corp governance entities like blackrock/KKR as in case of Indigrid (Asset creator is Vedanta but Invit manager is KKR so minority interests in Invits are protected)

Valuations are subject to individual perceptions and all assumptions can be questioned. Regarding debt at 7.2 can get demonstrated as the management concludes the financial closure. I am optimistic on IRB Invit raising the funds in that range as they are AAA rated and rates may not be very different for this highly rated instruments.

As I view the price already captures all these uncertainities and was only looking for perpetuity of the Invit and this asset will add some cushion for coming15 years. Although levels less than 55 were ideal for me to add but I still feel price may come to early sixties by next quarter distribution.