Medplus IPO Note

Medplus Ltd IPO Note.pdf (855.2 KB)

Medplus IPO note.pdf (1.3 MB)

We need to some attention on SME IPO as well

last 3 to 4 IPO give very attractive return.

Today Vivo collaboration up 355% up from Issue price.

Adani Wilmar IPO likely to launch on January 27

At what price does PAYTM becomes interesting? 750 which is 15x revenue ? interested to hear others thoughts

I am tracking paytm as well. But the more I hear their CEO Vijay shekhar sharma, the less I am convinced about it. His interviews don’t inspire a lot of confidence. I would suggest listening to his interviews.

Will remove this in a couple of hrs as this post doesn’t add any value.

Hyper speculation thesis can be very hard to predict but some trends are there.

After Ukraine war many countries like UK,France and now even German now want to shift more quicker to other non Russian sources and also dfavouring there old policies.

These include

- Higher military spending

- Nuclear Powe renaissance

- Lpg growth story

Will this be a big target for someone like MTAR that depend a lot on nuclear power contribution is around 25%+ and also very heavy on exports.

Even there growth in this was very slow due to many countries avoiding and also shutting nuclear but now in opposite it can be a turnaround.

There client base is also us or Europe only so the focus shift can also be converting a headwind to now a tailwinds.

In defense most want r&d and modernisation that most Indian company might not benifit much but our own defence story is a great tailwind.

Disc: Not Invested

Can some one explain me about Ruchi soya FPO. They are offering shares at 615-650 range where as the shares are already trading at 800 means at a 20% discount we can get the FPO shares. It means they are devaluing their company? or is it my perception wrong?

Fpo is there for many reasons

- high debt and need to pay

- high promoter holding need to be reduced and they don’t have much time to reduce that.

- have some expansion plans.

They are placing fpo at such a discount for reason that they can’t delay there holding decrease plans and want quick and better way to do that as if they directly sell there holding to decrease below 75% it will tank stock way more then 600 and may also worsen the company while this will rather help in long term.

After fpo they will have around 4-6% more to sell that would be alot easy to sell directly in the market and will not affect the company that much.

If this fpo fails to gain attraction it will make there selling be more and will also have negative impact on the stock.

So take a hit now to raise money and then use it to pay debt, expansion and other objectives.

anyone review or any research report on PE Analytics SME IPO

Thanks in advanced

Excerpts:

The IPO price values LIC at around Rs 6 trillion or 1.12 times its embedded value of Rs 5.4 trillion at the end of December. The embedded value is a measure of future cash flows in life insurance companies and a key financial metric for insurers.

When LIC filed the draft red herring prospectus (DRHP), experts had pegged its valuation at two to three times its embedded value, based on the valuation of its domestic private sector peers. However, market volatility due to the Russia-Ukraine war may have changed the dynamics.

Listed private life insurance companies like HDFC Life, SBI Life and ICICI Prudential Life trade between 2.1 to 3.1 times their embedded value. The average market cap to EV ratio of the three is 2.6 times. If we apply the average multiple, LIC’s value would be Rs 14 trillion. The IPO valuation is almost 60% below this level.

However, it is in line with the multiples commanded by global peers which are anywhere from 0.21 to 1.89.

Analysts highlighted that LIC had a lower Value of New Business (VNB) margin of 9.9% in FY21 compared with private players, who have VNB margins of 22-27% due to higher share of participation and group products.

The government was previously criticised for under-pricing the October 2019 IPO of IRCTC.

At the top end of the price range, IRCTC fetched a market value of Rs 5,120 crore.

The government divested around 12.5% of its stake in IRCTC during the IPO and sold another 20% in December 2020. Today IRCTC is valued at almost Rs 60,000 crore, an increase of 1070% since the IPO. Does the government risk a repetition of the IRCTC episode?

According to Ashish Gumashta, CEO, Julius Baer India, govt is eyeing price discovery for LIC and it can’t think of a better defensive bet than this at this time. He believes this size will not disrupt the primary market, and the valuation leaves something on the table for investors. Market strength of LIC and private players vary.

Another expert echoed similar views. Deven Choksey, Managing Director, KR Choksey Investment Managers says **the govt wants investors to come again for FPOs. He believes the valuation is sensible in current situation, but price to EV ratio could have risen to 2 if market conditions were right.

Experts feel that the conservative valuation for LIC at this stage is a sensible approach by the government, which has to consider global and local market conditions, long-term return expectations of retail investors and the nature of LIC’s business compared to its private competitors, among other things. They say such attractive pricing will help an IPO of this size sail through easily even as the market remains choppy.

Excepts

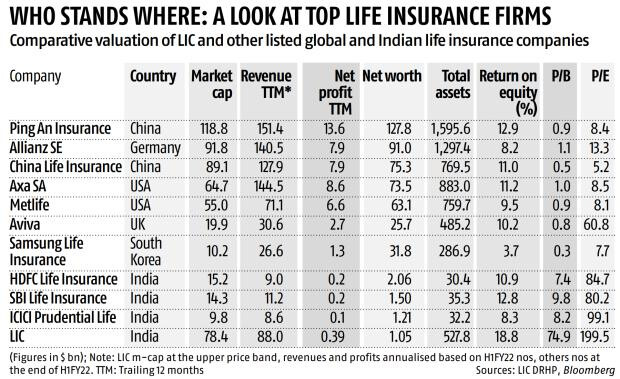

When Life Insurance Corporation (LIC) of India gets listed on the bourses next month, it will be among the biggest listed life insurers globally in terms of market capitalisation (m-cap), assets, and revenue, but will also be among the least profitable and capitalised among its peer group.

A big gap between LIC’s m-cap, profits, and networth (shareholder capital) will make it one of the priciest insurers globally, in terms of (P/E) multiple and (P/B) ratio.

LIC valuation is also on the higher side, compared to listed private sector insurers, such as HDFC Life Insurance Company, SBI Life, and ICICI Prudential Life Insurance. These private insurers are currently trading at a P/E of 88x on average — less than half of LIC’s. [LIC P/E of 199.5]

Similarly, private sector insurers average P/B value at 8.5x is also a fraction of LIC’s [ P/B 74.9]

Many insurance analysts, however, say that LIC is reasonably priced on the basis of its embedded value (EV). The public-sector insurer reported an EV of around Rs 5.4 trillion at the end of September 2021 (2020-21, or FY21), up 464 per cent from Rs 95,600 crore at the end of March 2021.

“At the upper price band, LIC is valued at around 1.11x its EV. In comparison, private-sector insurers are trading at 3-4x their EV,” says an insurance analyst at a brokerage.

Analysts attribute LIC’s poor profitability to its policy of distributing most of its surplus to policyholders unlike private-sector insurance companies.

“Currently, shareholders only get 5 per cent of the surplus generated by the LIC insurance business. This will rise to 10 per cent by 2024-25, translating into higher net profit in the future,” says another insurance analyst.

EV is the present value of shareholder interest in earnings, distributable from the assets of the life insurance business after an allowance for aggregate risks in the existing life insurance business of the entity for the relevant date. While LIC is cheaper on a price-to-EV basis, compared to private-sector peers, its margins are also much lower.

LIC reported a value of new business (VNB) margin of 9.9 per cent in FY21, against HDFC Life’s reported VNB margin of 26.1 per cent, followed by Max Life Insurance at 25.2 per cent. LIC’s VNB margin declined further to 9.3 per cent during H1FY22.

It is calculated by dividing VNB (expected profitability of new business written during the financial year) during the period by the annualised premium equivalent.

The VNB margin for all players improved substantially between 2015-16 and FY21.

But LIC is likely to remain a pricey stock, even if its net profit doubles from the current levels over the next three years.

Business Standard seems to be recommending a buy with this editorial…

https://www.business-standard.com/article/opinion/money-on-the-table-122042701365_1.html

The rationale is

But then in another article…

After reading these 3 articles… now I’m in a fix…

with my limited understanding i guess P/E with normalise to HDFC, SBI levels once this gets in 2 year time frame…

But the P/B ratio at 75 is roughly 10 times HDFC and SBI…

Being a behemoth, new business value is 1/3rd of other lister peers…

And when Bonus drops there may be a further drop in new customer addition… so wondering how this will all play out for LIC in the long run…

In the short-run can we expect listing gains to grab as indicated by BS Editorial ?

Seniors, any guidance on this would be helpful…

Currently Shareholders get 5% profit and 95 % to policyholders. Thats their practice from the 1956 , since inception. But IRDA in 1999, while privatisation, has given a limit of 10% profit to shareholders and 90% to Policyholders. If LIC starts following IRDA act, then it can change to 10%.

Also currently policies are two types

- participating policies, where profit is shared with policyholders as bonus

- Non-participating policies, where profit is not shared with policyholders as bonus like Term Insurance, annuity plans, cancer cover plans.

till now, Lic shares profit earned on all policies whether participating or no-participating with 5%::95% Ratio…

but going forward,it will share profit of only Partcipating polcies with policyholders…

what it means to shareholders =

- their profit share will increase to 10%

- their profit share will increase as all non-participating policy profit share will go to only shareholders…