IOL Chemicals and Pharmaceuticals Ltd.

Disclaimer: I am not a SEBI-registered research advisor or analyst. The following article is based on my understanding and interpretation of publicly available information and should not be construed as investment advice. I am invested in this company.*

IOL Chemicals and Pharmaceuticals Ltd. (IOLCP) presents a strong investment case with its robust business model, diversified product portfolio, solid financial performance, and strategic growth plans. The company operates in two key segments: Active Pharmaceutical Ingredients (APIs) and Specialty Chemicals, holding a significant position in both domestic and international markets. Here’s why IOLCP could be a potential investment opportunity:

- Strong Market Position and Diversification

IOLCP is a leading player in the API pharmaceutical industry and a significant contributor to the specialty chemicals sector. It is the largest global producer of Ibuprofen, commanding a 35% market share and is the only company worldwide with complete backward integration for all intermediates and key starting materials of Ibuprofen. Additionally, IOLCP is the largest producer of Ethyl Acetate at a single location in India and the second-largest global producer of Iso Butyl Benzene (IBB). This diversified product portfolio across multiple therapeutic areas and industries provides a stable revenue base and reduces dependency on any single product or market.

- Consistent Financial Performance

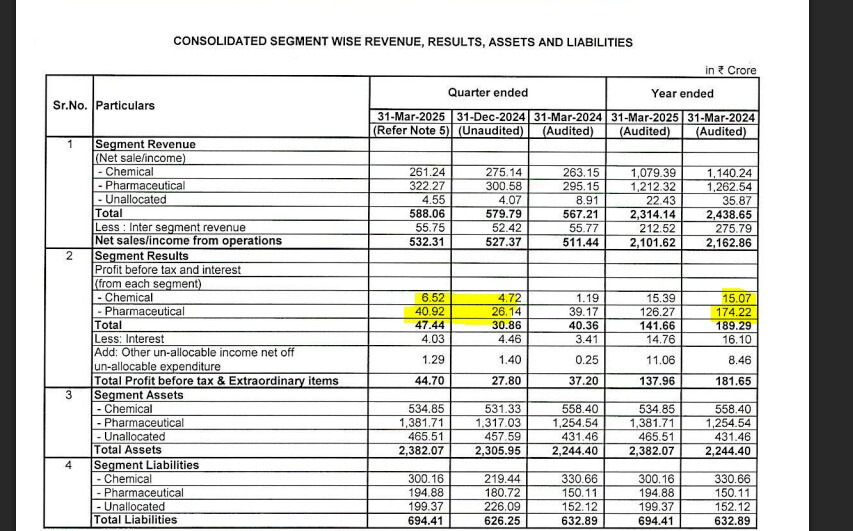

IOLCP has demonstrated consistent financial performance over the years, reflecting its strong operational capabilities. For Q1 FY2025, the company reported revenues of ₹509.76 crore and an EBITDA of ₹58.18 crore, with an EBITDA margin of 11.41%. Despite a year-on-year decline in revenue and profit, the company has managed to maintain stable EBITDA margins, indicating effective cost management strategies.

Over the past five years, IOLCP has shown steady revenue growth, from ₹1,685.3 crore in FY2019 to ₹2,132.8 crore in FY2024. Despite facing challenges in the global market, the company has sustained its profitability, with a PAT margin of 6.3% in FY2024.

- Debt-Free Status and Strong Balance Sheet

A key strength of IOLCP as an investment is its debt-free status, having not raised any debt since 2017. This significantly reduces the financial risk and interest burden, allowing the company to reinvest its profits into business expansion and innovation. IOLCP’s strong balance sheet, with increasing shareholders’ funds, indicates a healthy financial position and robust asset-building strategy.

- Expansion and Growth Strategies

IOLCP is actively expanding its non-Ibuprofen business, focusing on regulated markets, increasing asset utilization, and adding more products to its portfolio. The company has recently increased its production capacity for Paracetamol and other non-Ibuprofen APIs, such as Metformin Hydrochloride and Pantoprazole Sodium. These expansion efforts are aimed at capturing the growing demand in global markets, particularly in regulated markets like the US, EU, and China, where it has made significant regulatory filings.

- Sustainability and ESG Initiatives

IOLCP is committed to sustainability and has implemented strong Environmental, Social, and Governance (ESG) practices. The company operates a state-of-the-art Zero Liquid Discharge (ZLD) facility, ensuring minimal environmental impact from its operations. It has reduced its Scope-01 greenhouse gas emissions by 3.91% during FY2023-24 and aims for a 40% reduction in Scope-01 emissions and a 100% reduction in Scope-02 emissions by 2035. These initiatives not only align with global sustainability trends but also enhance the company’s appeal to environmentally conscious investors.

- Experienced Management and Governance

IOLCP’s management team brings extensive experience in the chemical and pharmaceutical industries, providing strategic direction and operational excellence. The leadership team, including Managing Director Varinder Gupta, with over 35 years of experience, has been instrumental in driving growth and innovation. The company’s governance framework emphasizes transparency and accountability, ensuring the best interests of all stakeholders.

- Favorable Industry Outlook

The global pharmaceutical and specialty chemicals industries are set for significant growth. The Indian API market is expected to grow at a CAGR of 13.7% over the next four years, driven by increased demand for generic drugs and cost advantages. Similarly, the specialty chemicals market is projected to grow robustly, with India poised to gain a larger share due to its cost-effective production capabilities.

Conclusion

IOL Chemicals and Pharmaceuticals Ltd. appears to be a compelling investment opportunity due to its strong market position, diversified product base, consistent financial performance, and strategic growth plans. Its debt-free status, commitment to sustainability, and focused expansion into regulated markets further strengthen its growth prospects. Investors looking for a growth-oriented company in the pharmaceutical and specialty chemicals sectors may find IOLCP to be a promising addition to their portfolio. However, it is crucial to conduct thorough research or consult with a registered financial advisor before making any investment decisions.