I am not an expert in this and defer it to what you say.

I have got some knowledge about some red flags to look for and this thing in inventories showed.

Do you think there is mismatch in fcf and net profit here in year 21. Company’s Fcf are outstanding when you look at previous years, but this last year mismatch has happened.

> The revision in the ratings assigned to the bank facilities of IOL Chemicals and Pharmaceuticals Limited (IOL) takes into account its improved financial risk profile in FY21 (refers to period from April 01 to March 31) marked by healthy growth in the profitability and improved capital structure. Further, the revision is also on account its strong liquidity and strengthening of debt service metrics.

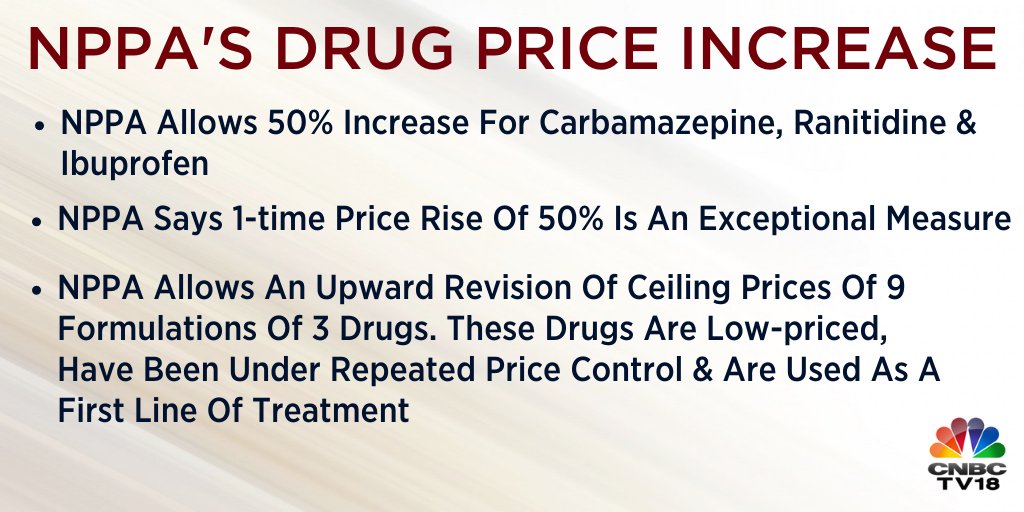

IOLCP has received approval of Korean Ministry of Food and Drug Safety for Company’s API products 'Ibuprofen and ‘Fenofibrate’. This approval re-establishes the Company’s efforts to keep the highest quality standards and to increase presence in the regulated markets. This will naturally strengthen Company’s presence in South Korean market.

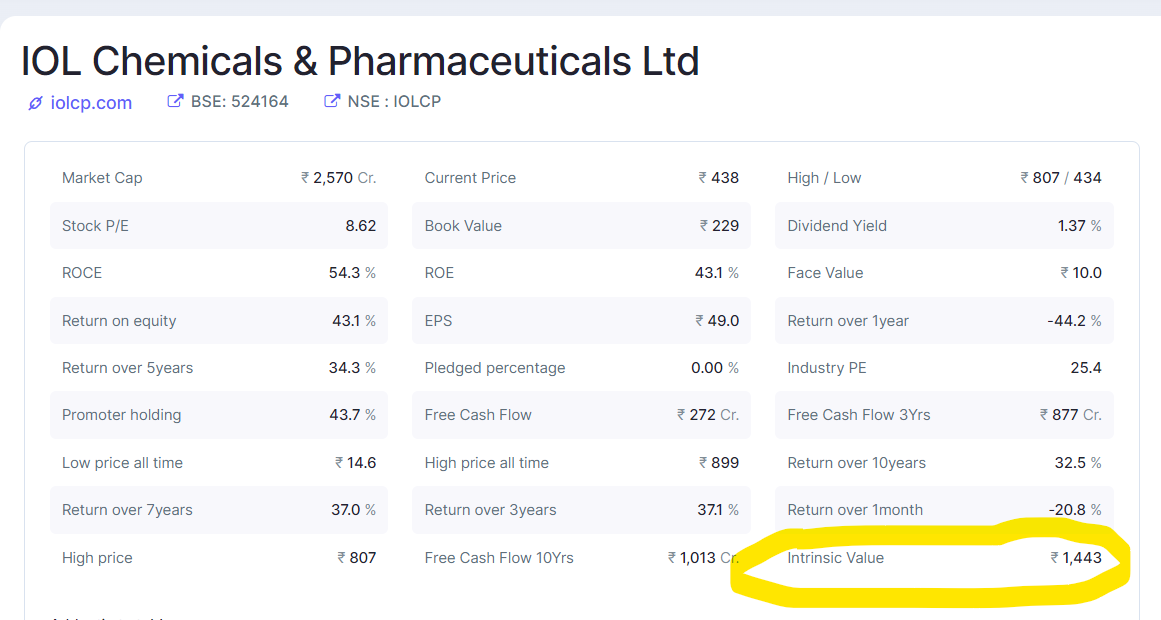

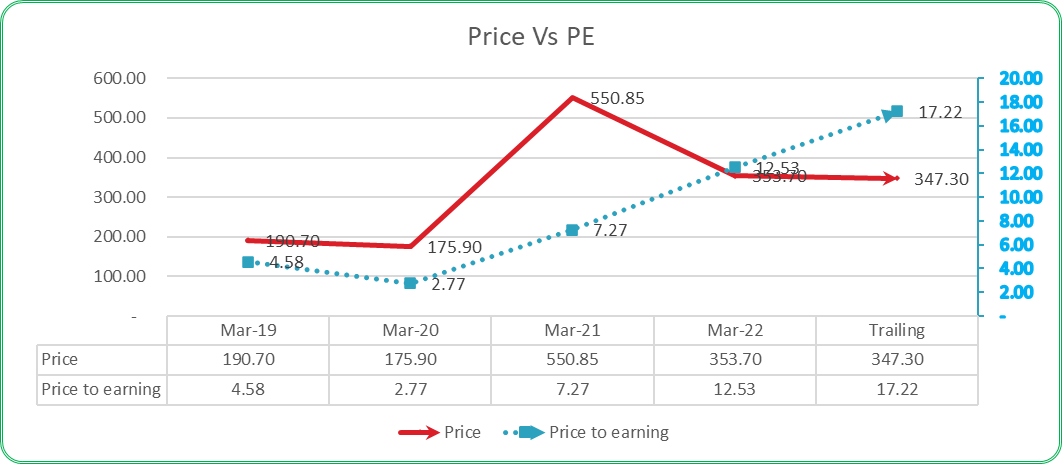

Intrinsic value as per screener is 1443. One of the major reason as everyone know for trading at such low valuation is over concentration on Ibuprofen and price of Ibuprofen remaining stagnant over last couple of months, IOL will continue to trade at forward multiple of 8-9 times only. If the market price needs to move to close to the intrinsic level, management needs to come out with a concrete plan of entering into high value products and more specifically specialty chem.

When asked in one of the earnings call, management did mention that their focus would be on manufacturing APIs in high volume, gradually improve the process and make these new molecules more profitable. Example, Gabapentin is facing severe competition still IOLCP went ahead to introduce this API in their portfolio.

Company is debt free and has decent amount of cash. IMO, IOLCP is not under pressure to hasten large number of successful molecules to overtake Brufin revenue

I am a long term investor but bit worried seeing decline from last 4 qtrs.

There was many things discussed in the last con call including various factor affecting price.

I am putting my notes here.

22 Nov con call

the company had a muted growth during the quarter.

The total revenue for the quarter increased by 2% to Rs.548 as compared to Rs.538 Crores in Q1 FY2021.

In Q2 of Financial year 2022 the EBITDA was at Rs.63

Depreciation for the quarter was Rs.11 Crores and Rs.21 Crores for first half 2022

Profit after tax for Q2 of financial year 2022 stood at Rs.31 Crores

there was some increase in raw material pricing, some of that we had been successfully able to pass on to customers and that will be reflected in the coming quarters

for some other areas, we are seeing a correction in the raw material pricing already in this quarter

So we do expect that this is a temporary blip that will correct itself within the next one or two quarters

The reason it is a temporary blip is that even if the raw material prices continue to be high we will be able to successfully pass along that cost increase to customers

we are expecting certainly maybe 330 Crores to 350 Crores kind of topline coming into the non-ibuprofen business for us this year and next year onwards we are very confident that you will see substantial jump in that figure.

Ibuprofen: peak capacity we believe that we can go through at least 85%-90% utilization and we have done that in the past

Ibuprofen: $11 to $12

Ibuprofen worlwide demand is 35000 and 40000 tons had contracted to maybe around 30000 tons and within the next two quarters it will be back to 35000 levels

Where do we see ourselves three years down the line. Because I remember like three quarters back when we had discussion with the outgoing CEO, he did mention that we will grow around 18% to 20% so, maybe by FY2024 we are looking at somewhere around 2800 - 2900 are we on track of is there a change if you can let know? Ans: We are on track I think 15% to 18% is a reasonable number for us and we will certainly in the next two to three years be achieving or exceeding both numbers.

The only capex that we have ongoing is the delayed project Unit No.9 that is a multiproduct facility that should be up and ready by the end of this quarter and that is the only one

Disc: i will wait for few more qtrs before taking any decision.

The irony in this statement of the company is when there is a product facing severe competition, it still tries to make it and in a more profitable way. On the other hand severe competition would reduce the margins by cutting the price.

“high volume” and “improving the process” can be copied by the competitors too.

IOLCP is not under pressure to hasten large number of successful molecules to overtake Brufin revenue

IOL has been very profitable only in the last three years. @reacharjunr is right when he says that the management should enter into high value product but it would require the necessary skill set.

IOL Chemicals incorporates a new subsidiary to focus on Pharmaceuticals and Chemicals business

IOL Life Sciences Limited incorporated as wholly-owned subsidiary of the Company on

20" June 2022.

Authorised Share Capital: Rs. 10,00,000

Paid-up Share Capital: Rs. 10,00,000

Size/Turnover: Not applicable

(yet to commence business operations)

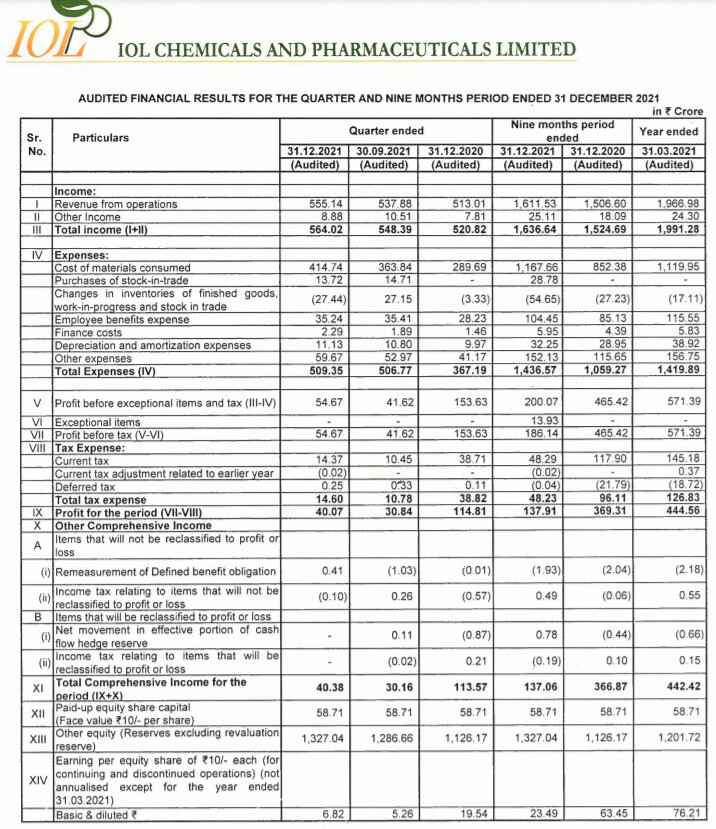

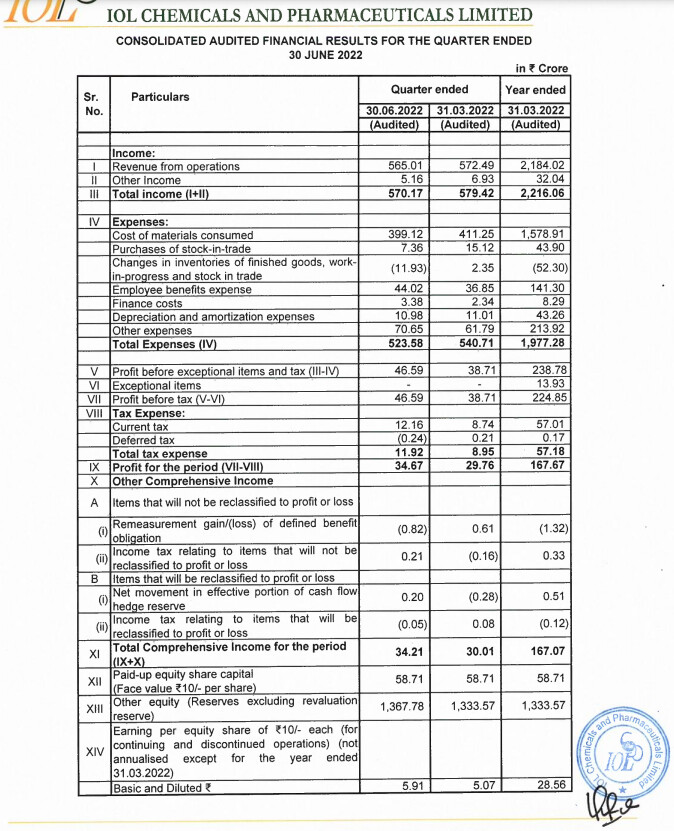

IOL Chemicals & Pharmaceuticals: Audited Quarterly financial results

Current utilization is running at 100% and the additional 20K MT capacity expansion done at a capex of 15Cr will get completed by Q3FY23

Need to listen from the management during earnings call. Their website says

it has 2 US plants and warehouse facility. IOL might be interested in tableting and warehouse

Am listening that energy prices are going above the roof in Europe including Germany, will this result in BASF increasing ibuprofen prices? 15 - 25 percent of IOLCP sales are spot sales

Any thoughts?

Disclosure: 30 percent of my portfolio is in this company, my views and the points I presented here could be very biased. Kindly do your diligence before investing

Revenue 546.5 Cr || EBIDTA 36.7 Cr || EBIDTA Margins at 6.7% || PAT 15.7 Cr || PAT Margins 2.9%

Chemicals

Ethyl Acetate price erosion mainly due to ongoing covid lock down in china, too much inventory which is being dumped all over the world at cheap price (QoQ price corrected by 40% )

At the moment the price of Ethyl Acetate is flat

Chemicals division negative EBIT ( -3 crores)

Normalized EBIDTA margins in chemical business are 6-8%

70% of the RM for chemicals is from China

Market is mostly domestic very less IOCLP exports

No new capacities are coming up

BASF plants shutdown don’t have any impact , they make in USA not in Europe

Chemicals that are produced : isobutylbenzene, monochloroacetic acid, and acetyl chloride

Pharma

Parma Business grown ( Q2 FY23 303 crores vs Q2FY22 241 crores )

Increasing product mix of non Ibuprofen share, more focus on products metformin, clopidogrel & fenofibrate

High costs of RM and energy impacted margins, some of this increase in costs are passed onto customers

Normalized EBIDTA margins in API business are 15%

Ibuprofen - Current asset utilization is between 75% and 80%. And in the next few quarters, I will take that to about 85%

Most of IOCLP domestic API business is on spot basis

Metformin - mostly sold in Domestic market , about 10% is sold to export market

PAP project (para-aminophenol) - paracetamol is fully backward integrated

Ibuprofen price is $11 - $12 in the export market and domestic market it is even lower

Ibu and it is derivatives IOLCP has 50% market share

Capex

20,000 Tonnes a year capacity is being added for Ethyl Acetate , will contribute to topline by Q1FY24

Guidance - 100-150 crore per annum

Registrations

(Europe Market) REACH Certificate for ethyl acetate and with a tonnage band of more than 1,000 tonnes per annum in accordance with EU REACH regulations on the chemicals and the safe use

EDQM certification to supply pantoprazole sodium as well as API in the European markets.

Sitagliptin patent - novel and green process, will bring in more cost advantages

Guidance

Rest of the year growth will be muted

Double digit growth will come back by FY24

Capacity addition in west side of India will be disclosed by Q4FY23

will be back to double digit EBIDTA margins by Q3FY23

Aiming to increase more regulated market sales, that will give some good margins

Registering 4 new products every year

De risking the IBU business , increasing focus on APIs

Key Products

Metformin - is the main first-line medication for the treatment of type 2 diabetes, particularly in people who are overweight. It is also used in the treatment of polycystic ovary syndrome

Clopidogrel - is an antiplatelet medication used to reduce the risk of heart disease and stroke in those at high risk

Fenofibrate - is an oral medication of the fibrate class used to treat abnormal blood lipid levels. It is less commonly used compared than statins because it treats a different type of cholesterol abnormality to statins

Pantoprazole - is a proton pump inhibitor used for the treatment of stomach ulcers, short-term treatment of erosive esophagitis due to gastroesophageal reflux disease (GERD), maintenance of healing of erosive esophagitis, and pathological hypersecretory conditions including Zollinger–Ellison syndrome.[4][5] It may also be used along with other medications to eliminate Helicobacter pylori.[6] Effectiveness is similar to other proton pump inhibitors (PPIs).[7] It is available by mouth and by injection into a vein.[4]

Sitagliptin, sold under the brand name Januvia among others, is an anti-diabetic medication used to treat type 2 diabetes. In the United Kingdom it is listed as less preferred than metformin or a sulfonylurea. It is taken by mouth. It is also available in the fixed-dose combination medication sitagliptin/metformin.