Management does seem confident of Sales for remaining year; I think the real question is whether they can take the success to other molecules and can generate the return on capital anywhere close to current levels. It seems to be a 2 product play for short term , and bet on Jockey in longer run.

Disclosure - invested but a small portion of portfolio.

As a learner seeking valuable comments on valuation of company…

Solara Vs IOLCP ( Select only because of the same Industry - No other rationale)

Sales Growth

IOLCP

TRENDS:

10 YEARS

7 YEARS

5 YEARS

3 YEARS

RECENT

Sales Growth

19.31%

21.61%

37.55%

38.66%

12.41%

Solara

TRENDS:

10 YEARS

7 YEARS

5 YEARS

3 YEARS

RECENT

Sales Growth

1.38%

OPM

16.40%

16.40%

16.40%

16.40%

20.86%

IOLCP - Performance Good…

2 . OPM

IOLCP

TRENDS:

10 YEARS

7 YEARS

5 YEARS

3 YEARS

RECENT

BEST

OPM

19.53%

20.06%

21.48%

24.19%

31.23%

31.23%

Solara:

TRENDS:

10 YEARS

7 YEARS

5 YEARS

3 YEARS

RECENT

BEST

OPM

16.40%

16.40%

16.40%

16.40%

20.86%

20.86%

IOLCP Performance is good

Borrowing

IOLCP - Company has not any long term outstanding debt, Virtually debt free.

Solara

Equity Share Capital

24.67

25.77

26.85

Reserves

739.30

826.10

963.09

Borrowings

632.87

538.06

706.79

IOLCP - Virtual Debt free

RoE / RoCE

IOLCP

Return on Equity

4%

3%

1%

2%

-33%

-22%

2%

13%

51%

45%

Return on Capital Emp

9%

11%

12%

-3%

4%

12%

15%

56%

69%

Solara

Return on Equity

0%

7%

12%

Return on Capital Emp

4%

10%

12%

IOLCP - Good Returns.

Debtors Day

Solara - 63

IOLCP - 54

IOLCP - Good Numbers

EPS

IOLCP

Narration

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

EPS

2.40

1.85

0.61

1.15

-13.97

-7.12

0.83

4.93

41.60

63.50

Solara

Narration

Mar-18

Mar-19

Mar-20

Trailing

EPS

0.15

23.07

42.61

36.75

Some concerns on IOLCP

Depended on single Product -

-all capacities of ibuprofen are online now and still demand is more than supply. Management assured they will meet minimum 15-16 usd for ibuprofen. Plan to maintain it for next 1-2 years.

-management confirmed capex of 150-200 cr each year for next 2-3 years.

Recently added to Nifty 500 and other indices, Also under ASM.

8 Valuation

IOLCP - P/E -10.7

SOLARA - P/E - 27

What I am missing here as selection of stock as no Mutual Fund entered in IOLCP (Whats restricting them to enter at lower valuation),

Basically I want to learn from experts the criteria which not following in favor of investment which I am not able to figure it out.

Lots of news regarding BASF Texas plant restarting now and Ibuprofen prices war due to its impact.BASF pricw $18 while IOL sells at $16.Can knowledgeable community in the group throw some light and educate us.

This entire message looks misguiding! It is an old message.

Even if we assume that the massage has some contains.

Then let us analyze logically.

It says, BASF price is $18, so where is the threat? on the other hand, IOL Chem is selling @ $15-16. USA Co will buy from Indian Co, so where is the threat?

As the BASF (USA) will be selling @ $20, BASF investors should be worried about it because of the higher price. The message is not explaining how the price of Ibuprofen will come down. Solara Active has increased capacity, will they stop it?

IOL Chem has a backward integration plant. Practically IOLCP has a better position than BASF, Solara, and any other ibuprofen producers in the world.

All these news are factored in the price. In my opinion, IOLCP is the cheapest company in the pharma sector with strong fundamentals.

My few may be biased as I am holding this company. You do your own analysis before taking any decision.

The message seems to be circulated vide malafide intent, as i have read through the ARs of the company i think IOL is the only company which is fully backward integrated for ibuprofen. as far as cost is concerned in my opinion this company will always has edge as long as this remains only company with backward integration or in case some other player develops a unique process that cuts down costs. it can fight price wars with US company. worry should be how long the prices of api will sustain?

IOL has fallen today below 700 levels. Huw is Ibuprofen pricing now? Is there any change to fundamentals? As per Mr. Vijay Garg in AGM, they were confident to achieve revenue growth of 25% resulting in a turnover of 2300 crores -2400 crores. Is this still achievable?

IOLCP finally hosted an earnings call. The call was well attended; analysts from Motilal AMC, Sunidhi Securities, Dalal & Broacha, and many other analysts & individual investors were there. Mr. Vijay Garg (Joint MD) answered most of the questions besides for couple of questions CFO pitched in.

Following are my quick notes

General Comments

Mr. Vijay Garg came across as a great listener and very well grounded person. He answered questions for 80 minutes, provided great insights about the business and strategy, thanked folks who asked questions, and still in the end explicitly said if there are unanswered questions then please reach out to us.

Present breadwinners – Ibuprofen, Ethyl Acetate and Iso Butyl Benzene(IBB). Next inline Metformin, Lamotrigine, Fenofibrateand, Clopidogrel, UDCA and PantoprazoleSodium.

Expect the Ibuprofen prices to hold at current levels in the short to medium term. The current price is USD 15-16 per kg.

Spot sales for Ibuprofen have almost vanished with macro factors stabilizing. Company has mostly long-term contract with clients.

Company aims to grow at 15-20% (topline) every year. Plans to increase the profit contribution from non-Ibuprofen to 50% in the medium term.

Company plans to go for 150-200 crores of Capex every year over the medium term. Firm no to debt. All capex would be supported by cash flows.

Capacity

Ibuprofen – capacity of 12000 MT per year. 90% capacity utilization and can be further increased. About 5000 MT production in the first half of the year. The capacity is 35% of overall world’s Ibuprofen capacity. Other significant players – Solara, CN players, BASF.

Ethyl Acetate – 87000 TPA and IBB – 12000 TPA. A lot of traction in chemical business because of businesses opening up again after the lockdown.

Metformin – 11200 TPA. At full capacity, it would contribute 250 crores to the topline. WW capacity for Metformin is about 100000 TPA and the demand is growing at ~5% per year.

Product Pipeline

Available APIs (there contribution to topline to increase) Metformin, Clopidogrel, Pantoprazole, UDCA, Lamotrigine, Fenofibrate.

Target development of only those products which could give good margin.

Continue to reduce dependence on Ibuprofen by increasing share of other products.

CN Factor and PLI scheme

Only dependence for Ibuprofen was for Sodium. Now company has found an alternative.

For Metformin all companies and so even IOLCP is dependent on CN for KSM.

Has not applied for PLI schemes yet but discussions within company are happening.

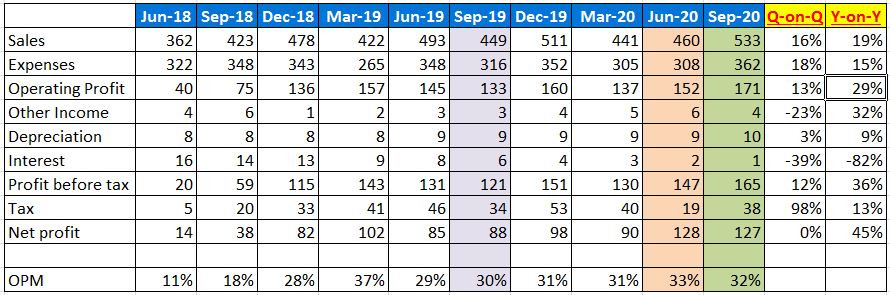

Financials

Q2 topline was 538 crores vs 452.4 crores Q2 last year. Profit in Q2 stood at 127 crores vs 88 crores yoy.

Debt is 21 crores. Reduced from 421 crores 2.5 years ago.

Cash on books is 281 crores.

Cash flow from operations (without working capital changes) in first half of the year was 326 crores.

Overall Impression

I came out from the earnings call far more satisfied with the management and their strategy. I like the commitment to growth, reducing dependence on Ibuprofen, healthy pipeline of products, firm no to debt and many more things.

I may have heard and/or interpreted things incorrectly. This is not a sell or buy call. I am not an analyst, and in general my knowledge is very-very limited. I own shares of IOLCP and have strong ownership bias.

Can somebody explain why IOL is trading at low PE of 10 compared to its peer Solara trading at PE of 25. In the last con call, I remember Mr. Vijay Garg has repeatedly mentioned that company is slowly moving towards diversification by adding other formulation products such as metformin, pantoprazole, gabapentin thereby resulting in risk mitigation by over concentration on Ibuprofen.

Kindly go up the thread and view the post of 30 Sep by Shri Murari. He has drawn a detailed comparison and also questioned the same. When all these products which are being launched or already launched start showing in the balance sheet in the next 2-3 Qtrs , I expect IOL to catch up and then overtake Solara. It is slowly inching up - - the Q3 result will show the direction of up move.

hi all, I wanted to understand whether 49% public holding is restricting IOLCP movement upwards. Need experts opinion to understand why the company is so undervalued.

The company is moving from a high debt commodity single product manufacturer to a debt free diversified business. Business transformations take a while and stock has re rate from a PE of 3 to mid teens in a few months. It’s a slow process, you should not expect the stock to keep climbing like it has. That’s not normal.

Thanks for the reply. I was checking the fundamentals of the company and was not clear why the valuations were so low. Your answer seems logical. I will do more research on this company and will update.