Hi guys,

I would love to know your thoughts after the recent con-call.

I would like to point out a correction to the above insights offered by @rmehta26 . The Rs.2,400-2,500 Cr guidance is for FY22 not FY21. FY21 will most likely stay flat vis-a-vis FY20.

I have a few concerns which I have been trying to wrap my head around.

Concerns-

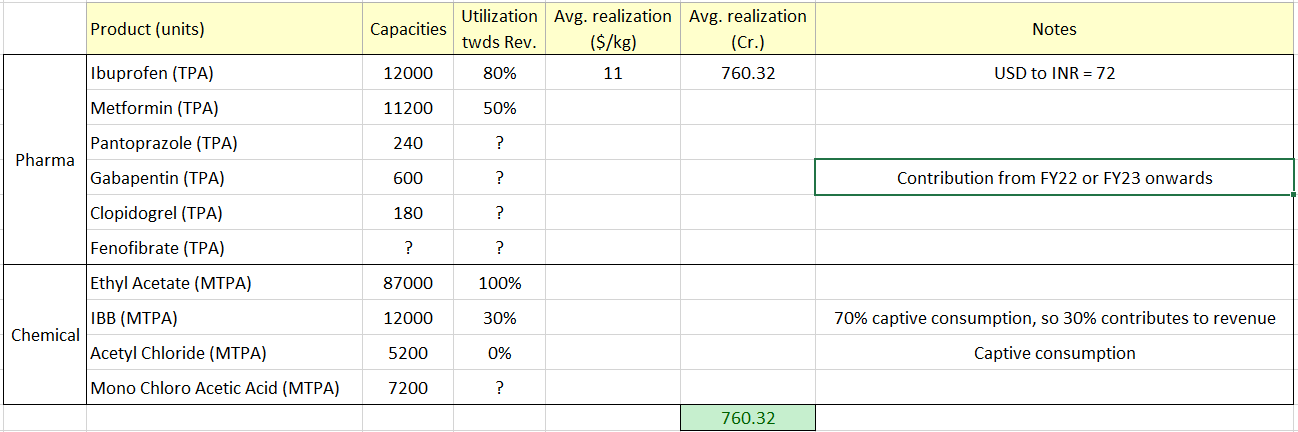

1. Ibuprofen spot prices correcting to $12-13 (this year they were $14-15 and the contracted prices were $15-16) and expected to go touch $11 in the medium term.

- So they do their 70% business on contract and the contracts reset annually. As the prices have corrected in the range of 15-20% and may correct further to about 20-25% in the medium term. That translates into 7.5-12.5% potential correction in realizations as 50% revenues come from Ibu currently (roughly Rs.1000 Cr).

- Inability to increase volumes on Ibu due to overall supply situation. So a dent in prices would definitely result in lower realisations.

-Potential Impact

Topline: 150-250 Cr

EBITDA: 60-100 Cr

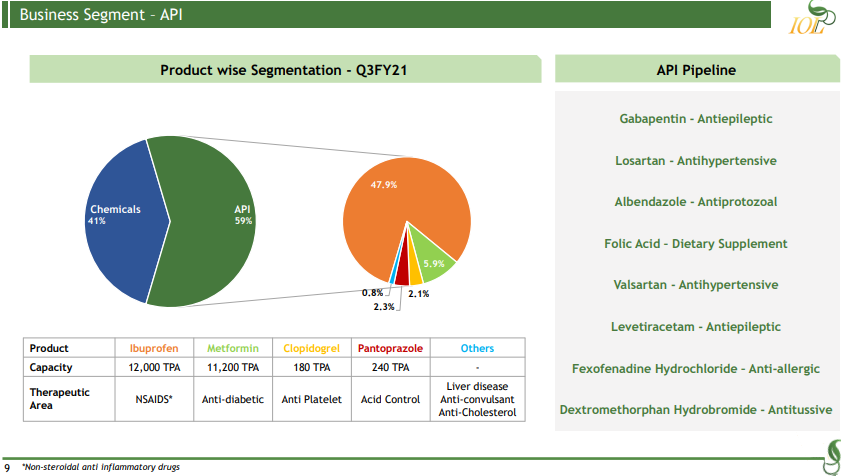

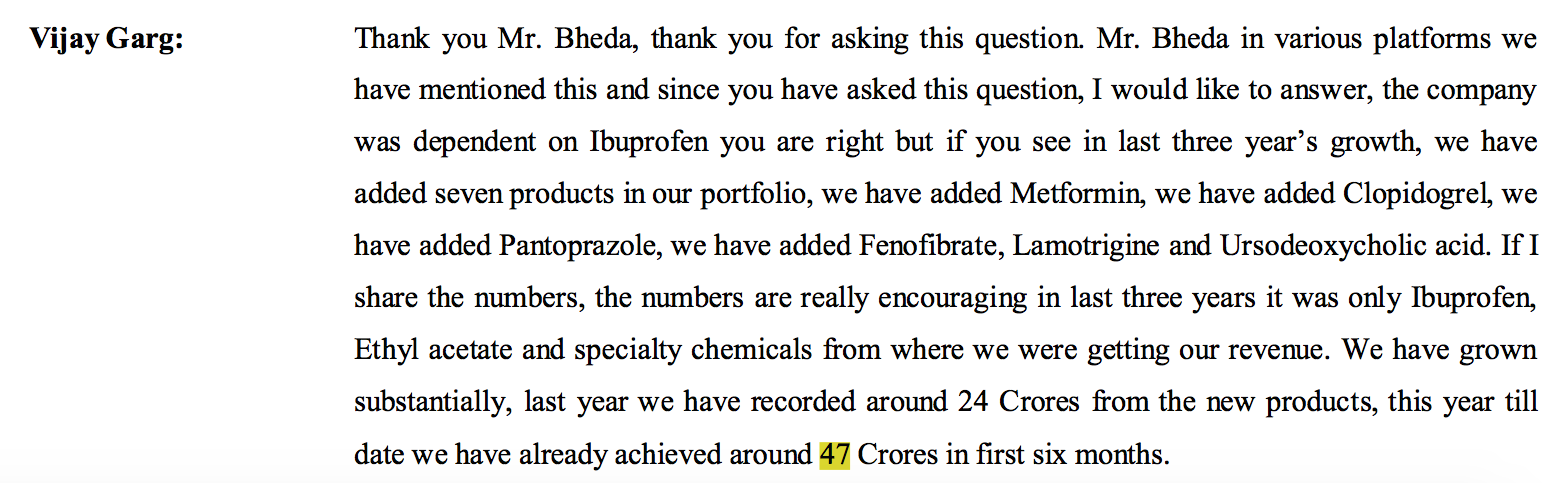

2. Not a lot of growth coming in from new molecules (drugs) in the near term due to slow ramp up and the usual 15-18 months gestation period

- Their list of upcoming and existing molecules is exciting but it would require longish timelines as their current capacities either scaling up, on the verge of completion or under construction.

Current year expected topline is 200 Crore and the coming year they should be able to add 150-200 Cr more as Metformin goes to full scale, other current molecules scale up, Gabapentin comes on and their FUL multipurpose plant comes on stream.

-Potential benefit

Topline: 150-250 Cr

EBITDA: 30-60 Cr

They are also expanding their Ethyl Acetate base (currently running full capacity at 87,500TPA) by 30%. Mr. Garg said there’s a fundamental shift to the business and they expect better than erstwhile margins. (earlier margins have stayed in the range of 8-10%). And they can scale up the capacity in the coming year itself by investing Rs.10 Cr.

Now doing some back of the envelope calculation, they must be making around 600-700 Cr revenues currently from this product. So the additional capacity would add 180-200 Cr to the topline, albeit at a lower margin vis-a-vis drugs. (Last-Q margins: 15%, This-Q margins: 17%).

If they are able to sustain the margins say at 13-15%. This adds about 20-30 Cr worth of profits. (The expenditure is in turn value-accretive at east at the moment with a high IRR).

I believe the coming year could be flatish in terms of profitability growth due to a hit on Ibu prices (and the Ibu margins incredibly high at around 35-40% this year going by their EBITDA).

The one thing I am failing to clearly get is what all capacities of what all products have been commercialised and can go to full scale when. Because in Q2 concall they said they are “planning” on capacities for Gabapentin, UDCA, increasing Fenofibrate, etc. So if anybody has a clearer idea as to the product wise capacities on-stream, being constructed and also in the pipeline.

If we consider a 5 year horizon, the capacities at any stage could be on stream by then and at full scale (major “if” involved, as to whether they can do full capacity utilisations for all the products… a little bit of respite is their product selection criteria and involving only decently growing molecules). By what I can gather from the calls and doing back of the envelope calculations, full capacities could add roughly 1500Cr of topline from Drugs alone and about Rs 300 Cr of Ebitda (as their Ebitda guidance is 20-25% for new drugs).

Their current TTM Ebitda is Rs 618 Cr. And the addition would be at best 50% growth (this is not even factoring in Ibu price erosion).

So basically everything is contingent on the clarity as to at what stage their new products are and the pipeline as well. So is it that the 150-200 Cr capex they’ll incur would be mostly for the future products they come up with and which are not planned yet or would it be for currently planned products? If it is the latter, then there’s every reason why the current PE is low.

Sorry for such fragmented thoughts at the moment.

I would absolutely love to be appended and even more to be contradicted!

Disc: Invested from much lower levels