However Vinati Saraf said that demand will taper off in coming quarters. This quarter was good due to stocking. Supply addition will definitely reduce the prices.

3 Likes

In any case IOLCP will always do better :

10,000 Tons per Annum

Capacity and Market Share

IOLCP has world’s second largest Ibuprofen manufacturing facility and is only company that has backward integration. It has recently de bottlenecked its manufacturing facility and has increased the capacity from 7200 TPA to 10,000 Tons per Annum

Clients :

- Outlier in Focus: A Quick View of IOL Chemicals and Pharmaceuticals » Capitalmind - Better Investing.

Active Drugs as per USFDA : List of Drug Master Files (DMFs) | FDA

3 Likes

So Ibuprufen capacity for BASF is coming online this year, I am not sure how with so much supply coming in, the prices can remain at these elevated levels.

Disc. Interested but not invested

5 Likes

Can you please share source/link for the screenshot

1 Like

Regards Metformin… Mr. Vijay Garg mentioned that it currently contributes 5 percent to the revenue ie approx 150 crores to the top line. And now it will contribute 400 crores to the top line. From his cnbc interview. Not seen Metformin contribution mentioned anywhere and finally got a clue straight from the source! Edit: He also mentioned ibuprofen and Ethyl acetate contribute 90 percent of the revenue (60 and 30 percent respectively) . Was it not 85 percent earlier? Maybe I am nitpicking

3 Likes

The expected top line if I remember it correctly from the interview was around 2300-2500cr for FY21. Going by an estimate of 400cr of Metformin and taking the higher range of 2500cr, it should contribute around 15-16%, thats my understanding from the interview.

1 Like

Good Insights from the discussion here. I started first tracking this beginning of the Year when it was 150-170 ish (invested since then). Building further on the discussion

What’s Working for IOLCP?

- Strong tailwinds - BASF partial shutdowns, Ibuprofen demand surge, Price increase

- No Debt(this cannot go bankrupt even if demand falls to zero tomorrow). The finance cost for FY20 was around 21 crores and this can be expected to be 4-5cr this year so adding 3-4% to bottomline.

- New products : Metformin which they expect will add 150 crore addition this FY

Overall, the topline growth seems muted and the bottomline growth is driven by lower taxes, Interest costs, and margins (not in the order)

What’s my worry on IOLCP?

- I try to capture relevant insights into a quantitative financial dashboard. Based on the trends, its numbers have massively increased (ROCE, ROE, margins) over the last 2 years (only). Now whether this sustainable is another thing - Topline growth has stayed muted in the 2 years (quarterly basis)

- Mr Vijay Garg has been quite optimistic in stating a 20-25% growth in topline but that largely depends on how Ibuprofen prices sustain during the year and how well are they able to commercialize metformin. Big Question marks here.

- Tried using Owners earnings (OE) to arrive at an intrinsic value. Main concern is that even with a high 3 year average of OE, i don’t think it warrants a high 10 years future growth rate. Without a good future growth rate, it doesnt seem that there is much steam left but the game changes once you factor in 7%+ growth rates YoY

Ultimately it comes down to

a) how they are able to reinvest cash to generate high returns. If they don’t the high cash on their books is going to lower their ROE

b) How long will the Ibuprofen trend continue. Once the fat lady stops singing they definitely face the product concentration risk in a major way without any competitive advantage (atleast what i can see).

happy to be challenged

Regards,

U

9 Likes

For now they will reinvest cash to expand existing capacity of their 3 new products

-

My assumptions on ibuprofen will play well during rainy season domestically (India) - BASF is already on a capex for ibuprofen expansion and planned open date is 2022 . Till then we can see ibuprofen sales going good for IOLCP.

-

Metformin prices are roughly $4 where India being the highest exporter in the world

Ipca, Lupin, Granules, Aurobindo, Laurus etc all have Metformin as API -

Rest 3 new product prices range about $1-$2

-

https://www.pharmacompass.com/manufacturers-suppliers-exporters/metformin-hydrochloride

@Uzair_Fahmi : your views on rest new 3 products?

1 Like

Since the declaration of results the stock has been on a slow down slide. Not much but approx 1.2 percent on a each day . I am aware that its best to avoid looking at the stocks on a daily basis . Are the results hiding something apart from decreasing top line YoY ??

On the other hand Laurus Lab in the same space has been moving in spurts initially but now slowed down , but closing in green on daily basis.

Bought 3 slips of 10 tablets each of metformin tablets today for neighbor - there are 2 forms of metformin tablets diabetic patients to consume 2 tablets a day mandatory - dosage sizes varies

Metformin tablet is a daily must for sugar/diabetic patients to control sugar and leading to the estimated population and size of opportunities - India sells these products highest and this is something which doesn’t come in one season and go off…

Seems if the industry has a good long term contract to manufacture for years to come there will be frequent flow of income…

API -> Target Pharma industries (Big Fish) - no worries about the sales - they can target multiple range of pharma industries to distribute their API. - this is the first step

Pharma -> Target customers (Small Fish) - less sales then we would see PAT been affected - pharma to customer - second step

6 Likes

IOLCP Will be added to Nifty 500, Nifty Small Cap 250, Nifty Midcap 400…from 25 Sep’20

@ Forum Member, Is this add any value to company investment point of view ? ind_prs20082020.pdf (374.1 KB)

6 Likes

IOL CP AR Notes

- Indian pharmaceutical industry supplies over 50 per cent of global demand for various vaccines and it caters to 40 per cent of generic demand in the US and 25 per cent of all medicine in UK. India contributes the second largest share of pharmaceutical and biotech workforce in the world. India’s domestic pharmaceutical market turnover reached

1.4 lakh crore (US$ 20.03 billion) in 2019, growing 9.8 per cent from1.29 lakh crore (US$ 18.12 billion) in 2018. - Indian drugs are exported to more than 200 countries of the world, with the US being the key market. Generic drugs account for 20 per cent of global exports in terms of volume, making the country the largest provider of generic medicines globally and it is expected to expand even further in coming years. Pharmaceutical exports from India, which include bulk drugs, intermediates, drug formulations, biological, surgical, Ayush & herbal products reached US$ 19.14 billion in FY19 and US$ 13.69 billion in FY20 (up to January 2020). The exports are expected to reach US$ 20 billion by 2020. In FY18, 31 per cent of these exports from India went to the US. Healthcare sector witnessed private equity investment of US$ 1.1 billion with 27 deals in first half of 2019.

- The ‘Pharma Vision 2020’ by the government’s Department of Pharmaceuticals aims to make India a major hub for end-to-end drug discovery. The sector has received cumulative FDI worth US$ 16.39 billion between April 2020 and December 2019.

- The COVID-19 aftermath has plunged the industry into crisis mode, but it could just be the rude wake-up call it needed to set it on course correction. The coronavirus outbreak has started to hit India’s pharmaceutical sector leading to rise in the prices of key ingredients. Now the prices for vitamins and penicillin are double or triple their original price. Similarly, cost of paracetamol has gone up. Another major impact is that pharmaceutical companies face is disruptions due to extended factory closures in China. If the pandemic continues then stockpiles of pharmaceuticals, APIs and other chemicals may decrease, resulting in shortages.

- Company is one of the leading APls / bulk drugs Company and is a significant player in the field of specialty chemicals with world class facilities. The Company is a manufacturer and global supplier of APIs such as Ibuprofen, Metformin, Clopidogrel, Pantoprazole and Fenofibrate and other APIs and has significant presence across major therapeutic categories. Demand for APIs is showing continuous increase due to growing incidences of lifestyle diseases, rising demand for affordable healthcare delivery systems.

- Specialty Industrial Chemicals segment of the Company includes manufacturing of Ethyl Acetate, Iso Butyl Benzene (IBB), Mono Chloro Acetic Acid (MCA) and Acetyl Chloride. Ethyl acetate have application in diverse important industries like pharmaceuticals, ink industry, flexible packaging, adhesives, surface coatings, flavours, paints & lamination and essences etc. The demand for the product is driven by a wide range of end use industries.

- The Company has its manufacturing unit situated at Village: Fatehgarh Chhanna, District: Barnala, Punjab. The Company’s R&D Centre approved by Department of Scientific and Industrial Research (DSIR) is equipped with advanced and analytical instruments and having a captive co-generation unit with capacity of 17 MW to meet power requirements.

- Currently, Company has six APIs in its pipeline wherein R&D work has been completed and processes are ready for scale up/commercial trials.

- Going forward, the company’s R&D is targeting to develop at-least 5-6 APIs every year including developing its KSMs. The company is planning to step up its R&D resources in terms of man power and infra-structure which will enable Company to give high throughput in terms of processes developed.

- Pharmaceuticals- 64%

- Manufacture of organic and inorganic chemical compounds -36%

- The Company has in house backward integrated manufacturing facilities to ensure continuous supply of major raw material used in bulk drugs, Ibuprofen.

- The Company has also expanded its customer base in about 80 countries to mitigate geographical risk.

- The Company is a global leader with about 33% market share in Ibuprofen.

- The Company has prepaid all of its term loans amounting to

205.32 crore during the year (20.05 crore in previous FY) in addition to scheduled repayments. - Investment in property, plant and equipment increased during the year mainly due to installation of new manufacturing facilities for production of Pantoprazole, capital work in progress for installation of new manufacturing facilities of Metformin and purchase of additional land.

- Trade receivable and trade payables increased corresponding to increase in volume and market scenario. Cash and Bank balance increased with retained earnings and increase in liquidity.

4 Likes

Exports data only! (only till June here)

Ethyl Acetate: looks overall FLAT TREND

https://phreakonomics.in/export-import/micro-individual?startDate=2017-09-01&endDate=2020-09-01¤cy=inr&hscode_commodity=1670&type=exports&consolidation=month

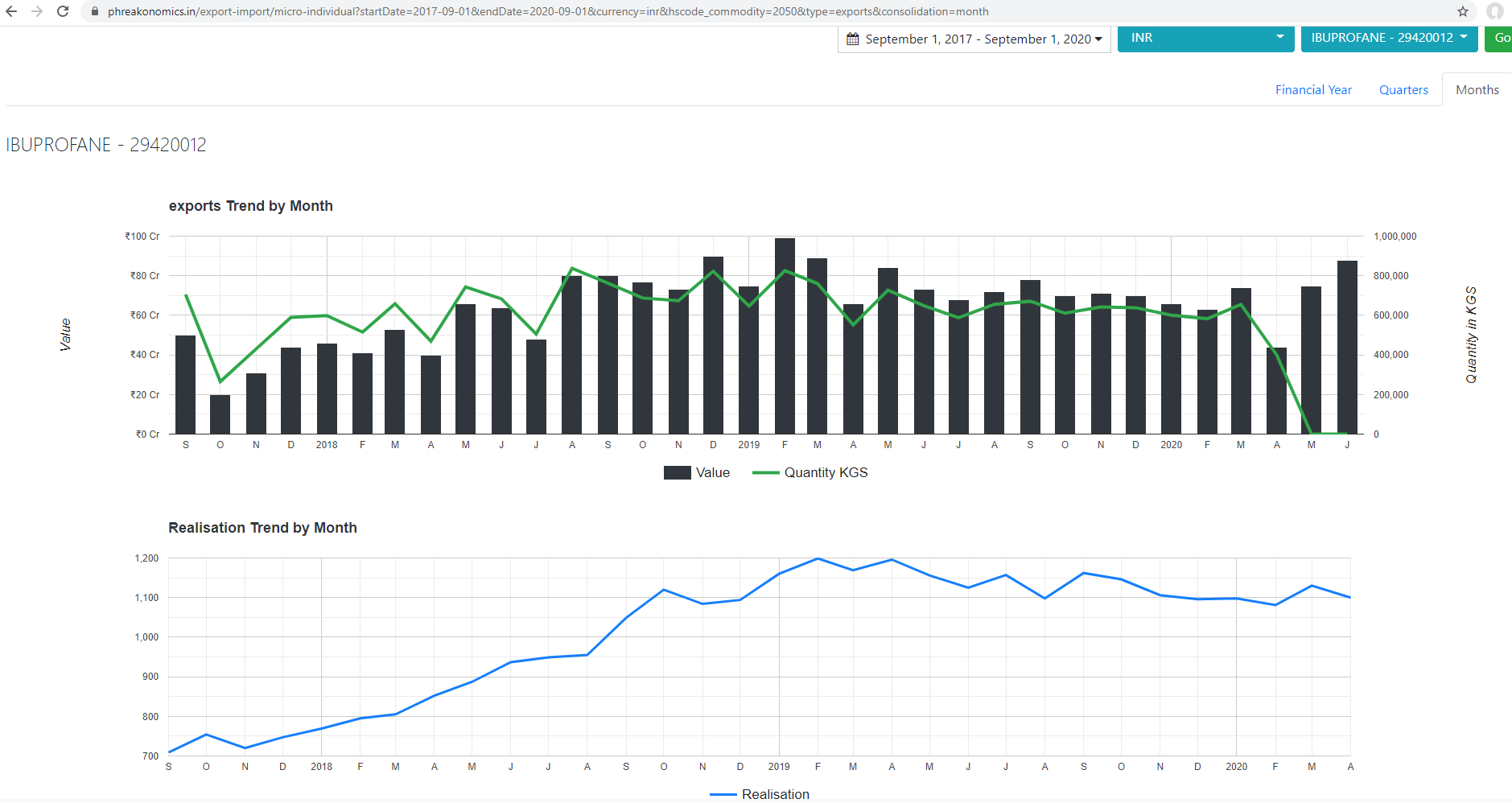

Ibuprofen: maybe BIT BETTER than usual

https://phreakonomics.in/export-import/micro-individual?startDate=2017-09-01&endDate=2020-09-01¤cy=inr&hscode_commodity=2050&type=exports&consolidation=month

2 Likes

Can someone help me understand why the stock is valued at low P/E of 10.

Was looking at this stock for my investment.

Being a API stock and with excellent performance for past 3/ 5 years, was expecting a better P/ E.

Is there any problem with management or any past record of corporate governance ?

Whether any promoter shares pledged?

Whether huge debt .

Thank you in advance for your inputs !

No share Pledged, All debt Pre-paid, On corporate governance any one please throw some lights.

No major corporate governance issue found as such. Company is debt free. One major issue was company’s dependence on a single product i.e., ibuprofen. But now company has been diversifying and moving towards multiple products.

@vikas_sinha ji can throw some more light on this.

7 Likes

Thanks Parul for the contribution on this thread! I do not have much to add than what is already present. All I can say is that indeed the management quality seems decent. They are making steady efforts to scale business to beyond Ibuprofen. So, certifications have been renewed etc. and some of the chems it seems can show good performance in the coming quarter (Ethyl acetate is a good jump YoY).

So overall, their Ibuprofen concentration strategy seems to have paid off and now they seem to be doing OK with expanding beyond also, hence I would say this shows consistent management quality. Tailwinds will help them here. Offers good growth in medium term at least. Currently stock is consolidating and offers good chance for entry.

Disc: invested

5 Likes

IOLCP Recent Expansions.

- Investment in property, plant and equipment increased during

the year mainly due to installation of new manufacturing

facilities for production of Pantoprazole, capital work in

progress for installation of new manufacturing facilities of

Metformin and purchase of additional land. - During the year, the Company has successfully set up Unit VI to

manufacture “Pantoprazole” and has started its trial production. The

installed capacity of the “Unit VI” is 240 MT per annum with a capex

of ` 33.83 Crore, which is met through internal accruals only. - Successful setting up a new Unit VII for manufacturing of ‘Metformin’ with the additional capacity of 7,200 MT per annum with capex of~ 28 Crore which is funded fully through internal accruals. Presently, the Company is operating existing unit for Metformin, having installed capacity of 4,000 MT per annum, which is fully utilized. With this additional capacity, now the total installed capacity of Metformin is 11,200 MT per annum.

4 Likes

I attended it but could not make notes. One thing which I liked about IOL AGM is they gave chance to shareholders to ask for questions.

Even one shareholder asked 25-30 questions in one go, he already emailed the copy and management answered it patiently for each question. One of the good agms which I personally enjoyed attending.

Some very good positives from AGM:

-management confirmed to meet growth target of 20-25% for this year.

-all capacities of ibuprofen are online now and still demand is more than supply. Management assured they will meet minimum 15-16 usd for ibuprofen. Plan to maintain it for next 1-2 years.

-management confirmed capex of 150-200 cr each year for next 2-3 years.

-management was open for more capex as well if good opportunity comes.

- management explained the plans of company. I am trying to recollect as correct as possible.

Short term plan- capex for low value molecules. Bring 2-3 new molecules each year.

Medium term plan - is to go for capacity 700-1500mt per year for molecules having price in range of 30 usd

Long term plan - is to go into very high value molecules like 3-5 lakh per kg.

In chemicals preference would be to backward integrate pharma molecules first .

Rest MR Vijay garg explained each current molecule in detail but I couldn’t remember that much. However good part is company is planning to have concall after q2 or at max by Q3 results. They are just looking for company which can assist them in concall. If it is finalised the q2 otherwise Q3.

Also Mr garg informed q2 results will be better than q1. He said they will try to publish results in 30-45 days from today for q2.

I hope I am able to give flavour of agm.

I have a small tracking position in iol. After agm confidence grew and plan to hold for couple of years.

11 Likes