They explained the tax deferral in point 4 of the notes within the result

While I agree with others that the results are not as amazing as people expected I am also of the opinion that we were expecting a bit too much from iocl. The reason it rose so quickly is because it’s been trading at an unbelievably low PE for too long and the improvement in results led to a sharp rise. However, it’s still only trading at 12 PE. So while these results aren’t amazing as compared to others in its segment it’s better QoQ and YoY and in iocls history that was a difficult achievement. Turning a company around isn’t a quick process. It’s only been firing with added capex, zero debt, new orders etc for a few quarters. The way things are going there will be a Laurusesque quarter one day. It’s disappointing it wasn’t this quarter but the long term story for me is intact since they’ve improved their bottom line and margins have increased even if just… marginally. I definitely will not be adding more to my portfolio(I’m using most of my free cash for laurus lol) but I don’t think I’l be trimming either. Anyway, waiting for some sort of breakup of its sales. Hoping we get to see it over the weekend. I suspect it will just stay within range until next quarter now. Not much upside or downside since the result doesn’t merit a re rating upwards or downwards. Will need to keep a closer eye on it from now on. The company only just began diversifying and the new capex sounds good to remove it’s dependence on ibuprofen though tbh I dunno anything regards the contribution of Metformin to the topline.

Note: I’ve also heard that due to lockdown they had a lot of logistics issues especially since they are situated in Punjab and faced a huge problem. I cannot verify this though . Also it looks like production wasn’t in full flow either. Again, waiting on management commentary but im pretty sure there are valid reasons for the less than bumper result.

2 Main revenue generating products of IOLCP that generate - 85% revenue

Ethly Acetate -

Ibuprofen - cost per this year per kg $18 - $20

Capacity : 1 lakh ton Ethyl Acetate - 15% revenue growth for 2021

Ibuprofen Metric capacity - 11500000 -20%-25% revenue growth for 2021

BASF : Why such a demand - because there are lot of demand for ibuprofen due to covid and this is a less cost effective drug - wherein BASF had limited quantity of ibuprofen.

Rest - 15% revenue generation is from 3 new products

2021 - Target 300 crore from new products

3 new plants

Metformin

Fenofibrate

Clopidogrel Bi sulphate

2021 Capex 150cr - 250cr - Funding would be done from internal growth ( Now we need to understand that the management is refunding its own money to grow its capital )

Product Dependence :

No much dependency on China

Maximum dependability will be from US, UK & other countries

Now coming back to square 1 - Ethyl acetate wherein Jubiliant life sciences are 7th largest global player there a topline of revenue would be added next IOLCP also would benefit from this.

Next Metformin & rest of 2 plants mentioned above is going through a capex due to good demand

Topline -

Ibuprofen - 200 crore

metric tons per kg 11500000 * 18 = 20,70,00,000.00

20,70,00,000.00 * 12 (months) = 200 crore roughly - please correct me if this is wrong - open to constructive criticism

I would say we may have a bumpy ride as rightly said by @vikas_sinha : but mostly a revenue of 500 crore + we can expect this year

Management will be giving a commentary on concall from Q3.

Expecting a total EPS of close to 70-80 from current level (63) then planning to trim

Disc : This is not a recommendation of buy or sell am also learning with the markets - please consult your financial advisor

I am bookmarking this. Cheers. Good work. So we basically need to keep an eye on

If ibuprofen demand increased why did the sales not explode. BASF will take a while to increase capacity anyway so we ll have a few quarters to see if this increase plays out.

How did they manage to get such high margins in ethyl acetate sales

How much contribution did Metformin have to the revenue and why are they doing capex in Metformin especially (long term contracts etc). How much would Metformin contribute at 11200 MT to the revenue

Ensure that all capex is done without debt. Please… no more debt and pledging

How badly affected were their logistics due to lockdown and maybe dependence on the US

I was hoping this would be a set and forget play but when buying small caps it never really is… is it

Also their inventory decreased for the second time now. Not sure why… possibly the lockdown scenario. But those expenses may come into play again soon. So need to keep an eye on why they fell. Also, I’m interested in knowing the details about their long term contracts with ibuprofen. Maybe it will give us a clue as to which from quarter we can expect to see huge benefits from those.

Note: I’m not a pharma expert so apologies if I’ve made mistakes. Still learning

Ethyl acetate was not a good market performer - if you can see my post in Jubiliant life sciences being 7th global largest player they too got hit by it.

Going ahead from this quarter end i would see Ethyl acetate do good… for last 2 quarters it was just a ibuprofen play…

Thanks for the clarification nithin. One of the main criteria for me buying small/mid cap stocks in sectors I’m still getting familiar with is they need to have an active forum here on valuepickr with members who have a keen interest in the stock. So even though it looks like we still have a few quarters to go before we can stop doing too much homework il add this as one more positive in the basket of iolcp. Cheers :).

Btw I noticed you mentioned you would trim your stake around 80 EPS? May I ask why? If the EPS goes up to 80 wouldn’t you want to hold your position even longer long term? It would mean a re rating and iolcp is already trading at just 12 PE? Just curious

If you see the company charts of long term growth

The EPS is around 80 for this company to sustain … It well doesn’t justify why can’t it go too high as well? Yes it can go high too now in this case ibuprofen was a pure demand basis and now this quarter they will do capex so the capital will be diverted to metformin which - I guess substantially the results would have some effect if the ibuprofen sales goes down or the company is yet to receive the sum amount in next quarter not sure - we need to check the receivables in such case and eps might reduce from next quarter if ibuprofen sales goes down However note Ethyl Acetate will catch up demand or not for this quarter we don’t know if yes then eps will do well & new 3 product for launch will take time - it’s not in a day or two that they will sell ethyl acetate and metformin so we need to wait till the results come out… might be after Q3 that’s why company has agreed to go to concall after Q3

So considering capex and long term valuation there will be a gap - this is purely my analysis I request you not to consider this and depend on it as this is my thought process. @hitesh sir and @Donald sir are very good in such terms am just an average student in the ocean of knowledge

Disc : Invested at 480 - Earlier invested at 230 exited at 350 earlier (Regret) - would like to take some free cash to invest in long term sectors.

Thanks for more color being added on IOL. In my opinion, if company wants to be on the right side of investors, management need to provide more clarity on the following:

What percentage of their sales comes from long term contract in ibuprofen?

When these contracts are coming for renewal?

If ibubrofen prices are keeping higher, why no topline growth - logistics issue or something else. Is management still seeing 20-25% topline growth for FY21.

On new products, have they got any clients on-boarded or still work in progress, because it is difficult to move an existing customer(s) from their long established supplier. So tailwind from new products may be still 3-4 qtrs away.

Also the revenue break-up of new products - Metmorfin, Clapidogril and Fenofibrate.

Right… the company doesn’t open up via concall for this or next quarter… if anyone working in this company or if we can email the company about such questions we might get some input…

Following are some notes I jotted down on IOL’s Q1 2020-21 results.

1- Revenue 466 cr vs 447 cr in Q4 2019-20 and 496 cr in Q1 2019-20 (4.25% up QoQ and 6% down YoY).

a)Chemical - 156 crores vs 157 crores vs 197 crores (QoQ and YoY).

b)Drugs - 313 crores vs 293 cr vs 309 cr.

c)Others (Non Chemicals and Drugs) - Immaterial differences.

2- Interest cost down 1.8 cr in Q1 vs 8.3 cr a year earlier in same quarter, pushing the margin up. Interestingly the employee cost is flat YoY. I expected this to go up because of Covid related expenses.

3- PBT

a) 8.36 cr which is 5.3%, vs 3.6% vs 3.8% (QoQ and YoY). < The margin on Chemical product was better in this quarter>

b) 138 cr or 44% vs 43% vs 42.3%. The margin on drugs has improved by 170 basis points. Maybe because of higher realization for Ibuprofen.

4- Profit: Not accounting for the deferred tax the PAT would had been 109 cr vs 90 cr in previous quarter and 85 cr a year ago in the same quarter. So without deferred tax company still reported 20% PAT growth QoQ and 30% YoY.

5- EPS for the quarter stood at 22.30 which is 50% up both QoQ and YoY.

6- Assets => There is 30% increase YoY. Both Chemical and Drug assets have seen increase.

7- Capacity: Metformin capacity increased from 4000 MT per annum to 11200 MT per annum. Ibuprofen: 12000 MT per annum.

My interpretations

1- Because of better product mix and/or better cost realization the margins are getting better. On top of that the company being debt free is definitely helping the profitability.

2- The revenue came almost flat which could be because of (this is just my guess).

a)The company could not produce more products because of Covid (logistical challenges). Capacity constraint or demand contraction should not be the reason given what we have heard in the earnings call of other API players.

b)Another possibility could be the negative perception about the usage of Ibuprofen for a brief period, which was later found incorrect.

3- Given that margins were better for both Chemical and Drug, the only thing missing was topline growth. If company could produce more then possibly it would have disproportionate profits.

4- The company has guided for 20-25% topline growth YoY. Given that topline in Q1 was 6% down YoY, IOL has to grow at 30% plus topline to meet the guidance. If the company would indeed be able to do it, then the profit would be far better than 30% (again because of better margins).

5- Metformin increased capacity seem to have come at right time because there seem to be shortage of Metformin in market: https://www.tga.gov.au/alert/shortage-metformin-modified-release-500-mg-multiple-brands. Earlier management was able to bring in additional capacity for Ibuprofen just before the shortage. Putting both points on the table, it does seem that management is able to tap on these market opportunities which shows agility & competence.

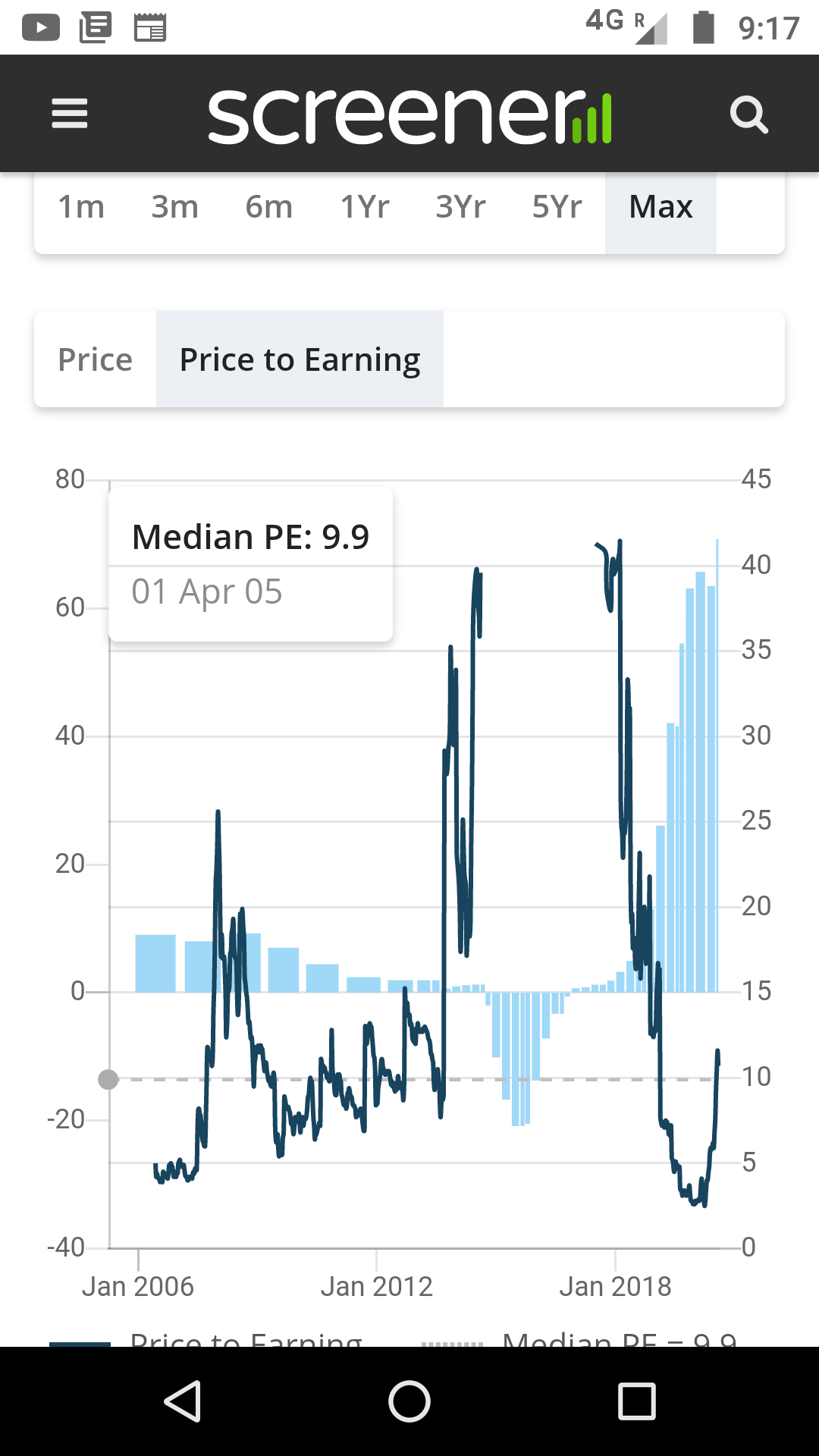

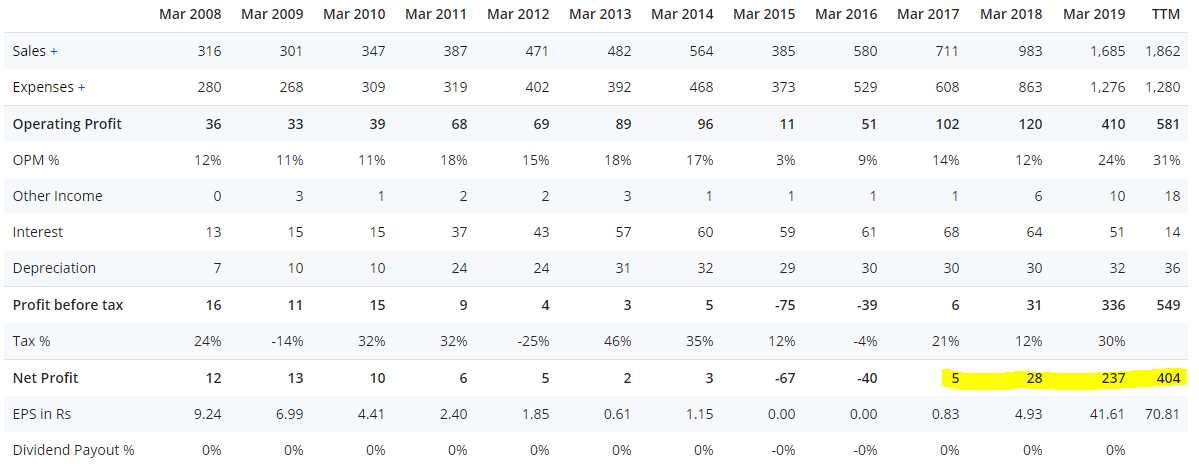

6- Valuation: TTM EPS after Q1 results is 70.81 which translates to PE of 11. Median PE for 1 year is 3.3, 3 years 12.5 and 5 years is 15.8.

The company does not have debt, and has significant cash on the books (from the Q4 BS). The core concern of single product dependency is being addressed by company with bringing in Metformin and other APIs and chemicals into play. The pharma industry also has tailwind with government backup. And finally, the management has given as guidance of 20-25% topline growth.

Cheers,

Krishna

PS: Not a buy or sell call. My knowledge is very limited and I am a novice retail investor.

Coming on this forum often - - but writing for the first time.

K K Rai have read and analysed your latest post , on the results. Very Well Done.

Nice break up of Revenue in QoQ &YoY, chemical/ drug percentages contribution in terms of revenue / PBT/ margins.

However the concern is still the projected additional contribution of Metformin in the balance of 03 Qtrs of this FY. This is a grey area as the increase in demand for metformin appears hazy & the anticipated price rise for this product is also unclear.This aspect has been earlier covered by Malkd also.

There has been less production / revenue of chemicals YoY ( but not changed QoQ ), intentionally , as the profit margins for chemicals vs drugs is phenomenal ( 5.3 vs 44). however being a backward integration company they still have to produce chemicals like IBB & others for ibuprofen. The company is focussing on Ethyl Acetate - - the profit margins are not known. Anyone any idea especially since the capacity is 1 Lakh tons .

Finally would the market escalate the PE and consequently the share price if the yearly FY 21 EPS comes to 80 - 82.

Disc - Invested at lower levels and added some more on the day of the results.

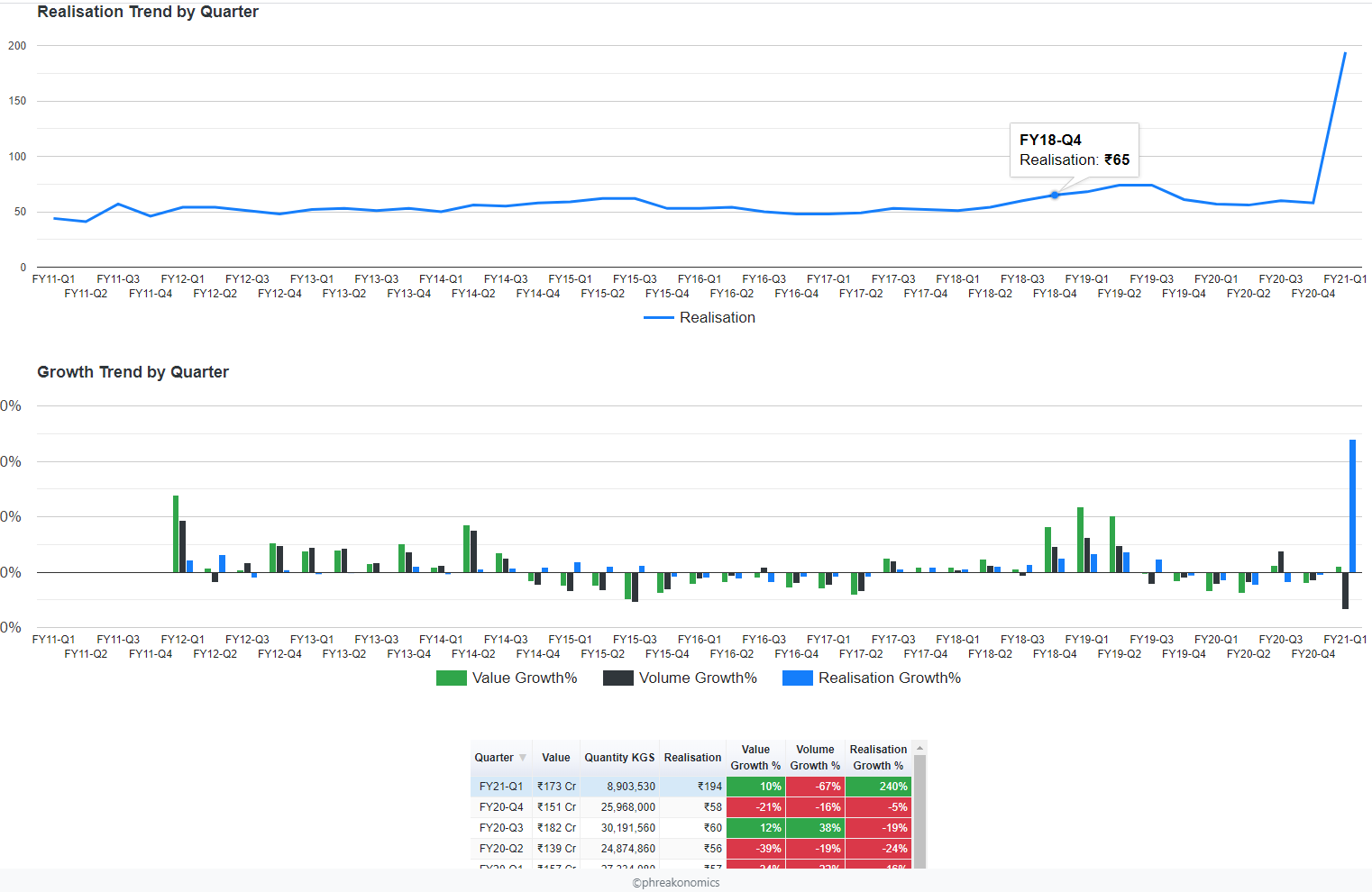

Trend for Ethyl Acetate Exports from India, it is showing big jump!

Though the data seems to be a bit wrong for latest quarter, it is said that DGFT revises published data and most recent quarter cannot be trusted.

Leaving aside Q1 FY21, trend seems flat. But we need to consider the domestic consumption market also.

Metformin is mostly just luck, though they do tend to capitalize well on such opportunities, making hay while the sun shines, fortune favors the brave etc. They do not have any fresh approvals since 2013, to be able to export to developed markets, or the data has not been updated.

Overall they have a very limited range as of now.

Though they might be happy with the domestic markets for the time being, cannot be said.

Mr Gupta was mumbling something about more approvals in pipeline in the interview on CNBC about Q4 FY20 results.

Given the overall tailwind in the API sector, IOLCP result has been slightly left behind in terms of the topline that has been posted.

In the Interviews given by Mr.Garg during the beginning of this month, he did say that some of the orders which couldnt be shipped will be booked in Q1, considering that scenario and the tailwind in full swing my expectation was there would be a good growth in topline

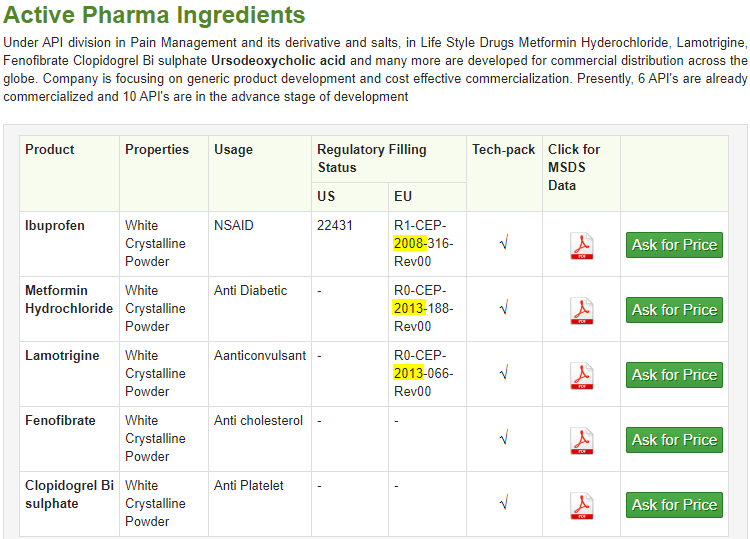

Also if fellow members can help me clarify apart from Ibuprofen, Metformin and Ethyl acetate they do have other bunch of products (ex - Lamotrigine, Febofibrate) any idea does that contribute significantly to their business, I couldnt find anything so any inputs would be helpful.

If we see the result of Vinati Organic, the topline get impacted significantly due to impact of Covidin April (as mentioned in the note). It seems Chemical business of IOLCP get impacted at some extend during the period though it is not clear from the statement of " Impact of COVID."

Disc:invested

In 2015 : Metformin hydrochloride is an API used in pharmaceutical products for treating people with type 2 diabetes.

The certificate, which is valid for a period of five years from the date of issue (ie April 17, 2015), will enable IOLCP to sell metformin hydrochloride in Europe resulting into increase in higher value added export turnover and margin.

In 2020 : Good News is that their product approval are renewed Now in 2020 National Institute of Pharmacy and Nutrition, Hungary, has renewed the EUGMP Certification for Ibuprofen, Lamotrigine and Metformin Hydrochloride products. Besides, it also approved the company’s recently launched products such as fenofibrate, clopidogrel hydrogen sulfate and pantoprazole sodium sesquihydrate. With this, the company will have more penetration in the European market, IOL Chemicals said

i will continue my research please feel free to post your comments - this will take our research on linear scale

As mentioned earlier Ethly Acetate will kick in from Q1 starting

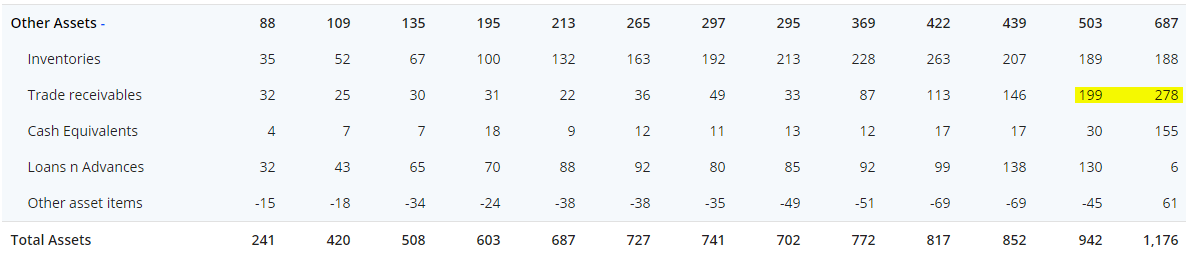

The Receivables* for 2019-2020 given below are raising in Balance Sheet

Considering 2015 was their silver lining of selling Metaformin approvals and rest of it - the company started to progress from 2016 after realizing the cash - the losses narrowed from 67cr 2015 to 43 cr 2016 - from 2017 profit of 5cr then sailing ship never saw backwards - if you see TTM the results are exceptional thanks for ibuprofen play going ahead strong tailwinds in Ethyl acetate (chemicals), Metformin (Pharma Drugs) - rest other products we can focus after year 2021 - so far management is right about 500cr for this year with their shares locked for 3 years giving in comfort and approval renewed - i take my words back on trimming.