This does not seem temporary, mgmt has guided that the demand jump is due to COVID and drug being a cheap drug in comparison to others . ALso many MNC’s have moved from purchasing their raw materials as well as other products from CHINA post COVID.

They have quoted in interview that their CSP is around $18 and where they have long term contracts they will be able to achieve $18 in FY 21

Additional - Methyl Acetate they have capacity of 110000, this year capacity utilisation was of 85000 tons, and next year they are targetting for 100000 tonnes.

The CARE Ratings Limited on 7th July 2020 has upgraded the Credit Rating by one notch (A- to A) for the banking facilities availed by the Company. Key points to be monitored (as mentioned in the rating):

Positive Sensitivity:

Strong and sustained improvement in the operating performance resulting in growth in total operating income and EBIDTA margin.

Diversification in product portfolio and reducing dependency on its main product viz. Ibuprofen.

Negative Sensitivity:

Reduction in demand and prices of the company’s main product Ibuprofen will remain the monitorable factor.

Regulatory risk arising due to nature of industry.

Any debt funded capex adversely impacting capital structure.

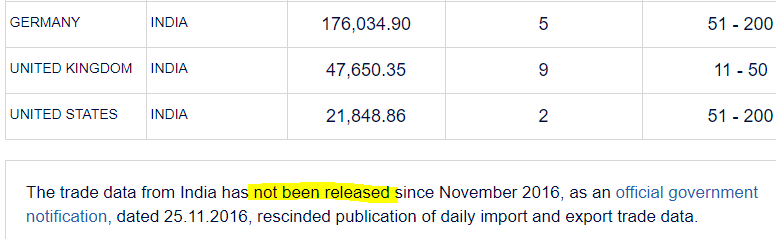

Thanks! I think you mean Ethyl Acetate, India seems to be a big exporter and small importer, looks like greatly traded commodity!

With avg price of $1/kg, 100k Metric Tonnes p.a. will give revenues of Rs 750 Cr. to IOLCP.

About 30% of their total revenues approx.

Does anybody know the price trend of Ethyl Acetate?

@vikas_sinha, Thank you for sharing the link. On the same website, the price of ibuprofen is $16.However, Vijay Garg, MD stated the spot price rises to $18. Is IOLCP is exporting to Germany only (price $18)?

@jaman_valuepickr I do not trust the quality of information on that website, that’s why asked about the trend in prices. The info I shared was just meant to give a very rough idea of Ethyl Acetate market. Somehow it shows India-specific info likely based on my location and then it gives a disclaimer below:

I think I do not see much divergence here from the usual pattern, checking past year data, whenever volumes are high the delivery rate has fallen to around the same levels. But yes, it is a bit lower than normal.

Try to understand the performance of the company in terms of basic parameters.You will understand whether you should exit or hold. Don’t be confused with the post on twitter or money control forum. More than 95% comments (positive or negative ) on those forum are illogical.

Thank you

Again, looking back at the history, this was and is around the lowest PE rating in 5 years, while performance has been better by the day. The price trend though very sharp and sudden has been on a secular uptrend (leaving the covid downturn aside). Overall would not say pump-n-dump is true for this one.

Point to be noted that the stranded shipment of lock-down will be shown in Q1. If every things are OK, Q1 result may be good. Any contrarian view on this.

The key take away from the "Disclosure of material impact of COVID-19 pandemic under Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015(iolcp-impcat-COVID-19.pdf )"

During the lockdown, the Company was able to maintain its operations as the Company’s activities /products were categorized under the essential activities/products.

The operations of the Company were affected during the last week of March 2020.

2019 Ethyl acetate capacity was running at : 83000

Ethyl acetate current capacity running at :100000 ton plus

What isnt justified that how long will this be remained and company has also 2 more new products that they were actively marketing since 2018 is showing up some values

Am unsure what are other 2 products that will hit the market since when ibuprofen story will be complete

So far March quarter numbers for 15 days of profit we are yet to see in June results

Ethyl acetate the company is also planning to do sales since the start of June Quarter - price of Ethyl acetate in global markets are seeing increase

we just need to plot imaginative figure for Ethyl acetate average price about 4%-5%

79% growth will be APAC since APAC is the highest market - due to corona disruptions what country favors for the market - no one knows

if someone has idea about their clients - we can take this research linear

List of companies who sell Ethyl Acetate

GNFC 50000 tons

Jubilant Life Sciences : Globally 7th largest ( in 2007 they were running about 40000) no idea on current capacity

IOLCP - 100000 Tons

Chemical revenue decreased but profits increased while Drug revenue increased along with profits. Could be a conscious decision to shift to drugs due to current needs? Will need to wait for commentary

Huge increase in margins in chemicals and an increase in margins for drugs too(though much smaller than chem)

Metformin capacity increased from 4000 MT to 11200 MT( Does anyone know the contribution of Metformin to the overall revenue/profits usually?).

Company says it foresees no issues with covid from now on but will need to keep an eye on this (I’ve summarised this in a childish manner. It’s explained properly in the result)

Deferred tax of 18 crores inflated profits a bit though still an increase in profits by 28 percent. Also, There was a less “a change in inventory and finished goods” expense of 20 crores as compared to Q1 FY 20 but the same was seen last quarter so doesn’t look like a one off. Even excluding that we have a profit increase YOY

Overall happy times . Not earth shattering… but not anything to worry about too much either.

Note: Editing as I read more in detail. If anyone can please add anything i missed please do.

Disc: invested e997bfe2-4a7f-491a-aa69-2c0d20700b09.pdf (1.4 MB)

I fully agree with the remarks of @Malkd quite nicely summarized.

My notes:

Chemicals were affected by lockdown but the pharma was not, that made results a bit flat.

Company is growing with the cash leverage it has.

Margins for pharma still seem bit muted, no great jump from the 2 weeks of delayed shipments from Q4. I always said mgmt guidance is that contracts are long term mostly.

Everybody does tax management practices to keep PnL looking nice, no exceptions!

Going ahead mgmt shows capability in growth.

We may have to wait till year end for growth in performance to cause more re-rating upwards.

Given the way, most of API companies are showing topline and margin expansion in Q1FY21, for IOL it is very flat, even after taking Q4 last 10 days sales not booked in the same qtr.

By the way, any idea what % of their sales of ibuprofen is undg term contract and when it is due for renewal. Disappointed with the number, if one sees the number excluding Q4 sales spillover and deferred tax benefit.

I wanted to know if any idea what % of their sales is under long term contract and when they are due for renewal. If they attributed to their past stellar performance to higher Ibubrofen prices, it should have got reflected in this qtr, unless they further added new clients under long term contract and reduced their spot sale of ibuprofen.