Reserve is always a liability. It’s accounted so by the accountants on the liability side of the B/S.

// Edit (19-June) | Revised to reflect Reserve and Profit interaction. Earlier, I mentioned about the ‘provisions’ instead of the reserves.

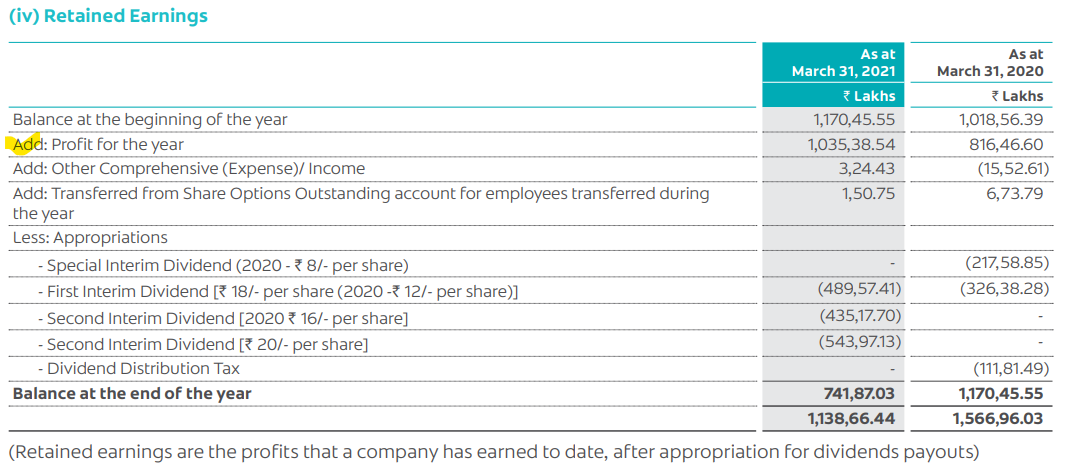

B/S is a cumulative record whereas PnL and St. of CF are created fresh every year. Earnings of a particular year are moved to the B/S using the approach you have mentioned. For example (FY21 AR of Colgate Palmolive) -

Reserves are simply record of historcal sum of Net Profit+ share premium(excess price investors paid over and above face value of share). These are the two major entries of reserves. There are many other reserves which are of lower value(DSRA etc.)

Cash is the actual thing you hold in bank.

With regard to shifting cash to reserve. It is done only when Company is raising money.

Example: Company sold 500 rs. worth Shares. So cash increased by 500 rs. Reserves increased by 500 rs.

If there is anything specific company you want to clarify VP’ers will be happy to help you.

Does it mean Reserves are not kept in bank (or invested in bonds, etc.)?

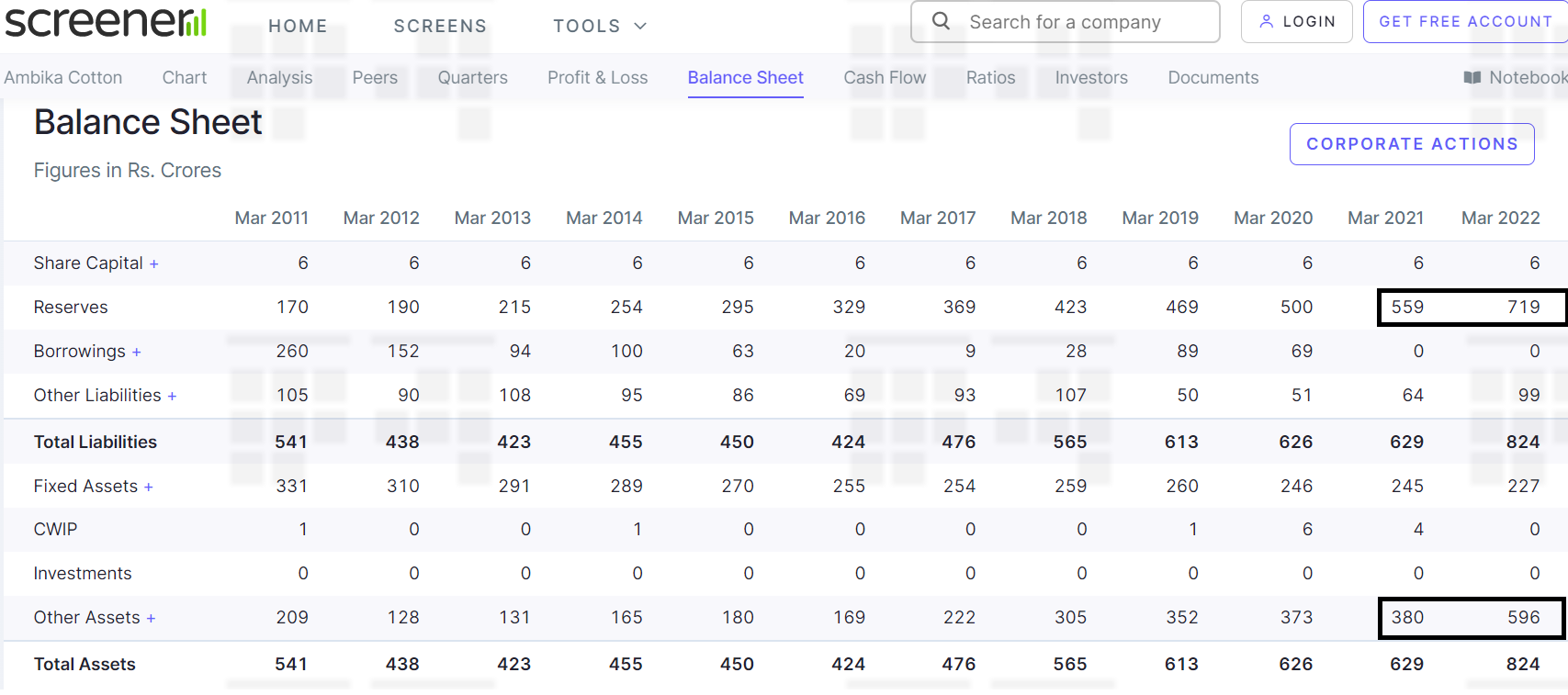

I was looking at Ambika Cotton Mills. This company’s reserves are consistently increasing every year. They don’t seem to have any expansion plans, at least not talked about by the management. This is what got me thinking. I was wondering if I can consider Reserves + Cash/Equivalents as the total cash owned by the company.

Reserves are just accounting entries there is nothing as such in the bank. With regard to ambika cotton I dont follow so gimme some time I will get back.

You have decided to own a house. While buying a house, 3 B’s are involved - Buyer, Builder and Bank [to avail loan]. The builder wants INR 100 to handover the house.

You checked your sources of funds:

Savings & Family Sources [RESERVES]: INR 30

Bank agreed to fund: INR 75 and you availed all.

Builder got INR 100 [25 from your funds and 75 from the Bank], and you got the house.

Congratulations!!!

Before the transaction, your balance sheet was as below:

Total Liabilities [Sources of Funds] - 30

Your Funds [Owner’s Fund, Includes Equity and Reserves]: 30

Borrowings : 0

Total Assets [Usage of Funds] - 30

Fixed Asset - 0

Cash - 30

After the house transaction, your balance sheet will be as below:

Total Liabilities [Sources of Funds] - 105

Your funds [Owner’s Fund, Includes Equity and Reserves]: 30

Borrowings [Bank Loan that you will honor as EMIs]: 75

Total Assets [Usage of Funds] - 105

Fixed Asset - 100

Cash - 5

Conclusion: Reserves is a source of funding and not the funds. You must not add cash and reserve to come up with TOTAL cash. Cash with you is INR 5 only, the one on the Asset side of the B/S.

Reserves are not necessarily the cash or cash equivalent in bank or anywhere else. Its is an accounting / balance sheet term which shows how much that company has in reserves as a value. Normally the reserves is total assets - all the other liabilities (share capital, short term/long term borrowings, other liabilities such as working capital etc).

Its like if you own a home which you have bought with a loan, then the reserves you would have for that home would be the actual market value of that home at a point in time (your total asset) - the loan amount (total liabilities). This is just a high level simplifies example but the things get a bit complicated when it comes to company account but the concept is same.

For Ambika Cotton Mills, I do not follow that as a investment study but I can quickly see that the reserves has gone up in last year because its other assets have gone up with the overall liability figures not changing so significantly.

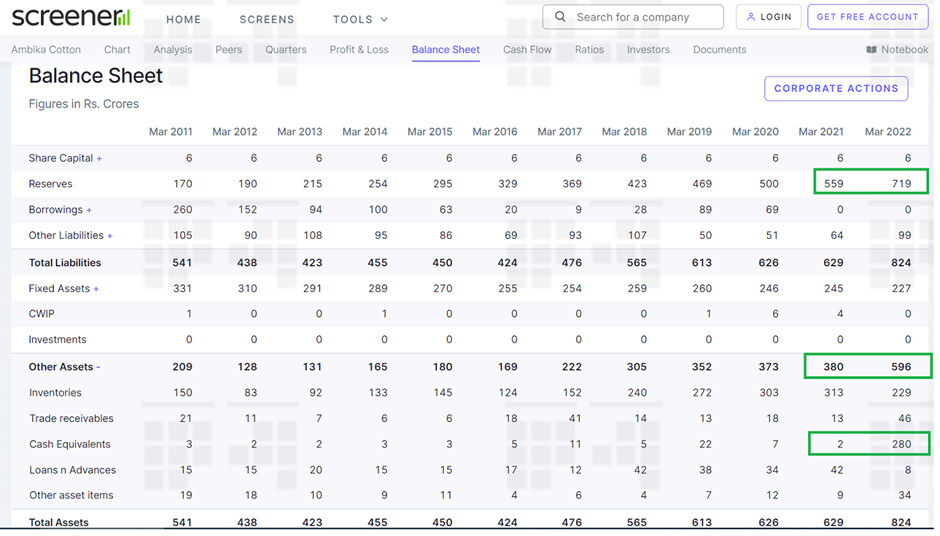

So in this case the reserves have gone up because cash eq have gone up, but that does not mean that all reserves are cash. Further it would be good to see from company AR what constitutes this cash eq.

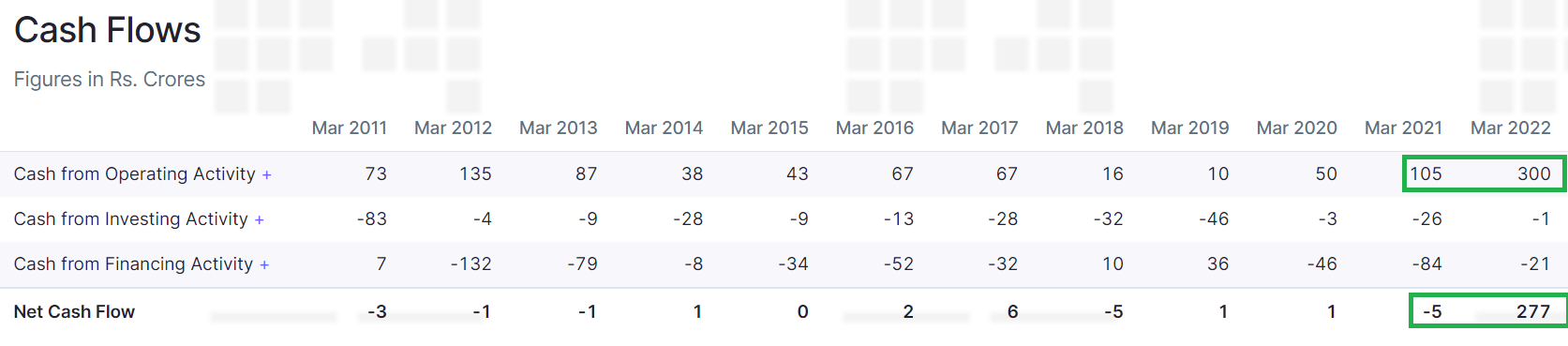

A quick glance at the cash flow shows that this cash eq is coming from the increase in the yearly profit which is being converted to operating cash flow and it is not being invested anywhere yet.

I really appreciate your interest in learning about these things. A basic understanding of accounting is a must for all DIY investors. Looking at your questions, I suggest you do a couple of formal courses on basic double entry book keeping which explains accounting fundamentals and how Balance Sheet, P&L Account and Cash Flow Statements are prepared. This will clear elementary doubts and help you understand financial statements better. Though I cannot pin point any specific course, I think enough free tutorials will be available on any standard e-learning portals such as Coursera, Unacademy etc. Wish you all the best!

@Malhar_Manek There are very subtle differences between a technocrat & a non-technocrat.

A Technocrat is basically a hands on promoter who knows the nuts and bolts of the business in & out. Typically he/she has been with the co. since it’s inception.

A technocrat promoter is particularly important in small cos because he/she has seen different cycles in that business over several years and sometimes decades. He/she may have turned around a loss making co. and made it profitable and could potentially take it to the next level over the next few years. He held a closely knit team through the ups and downs that is now poised to succeed. Compare this to a non-technocrat large cap such as Asian Paints which is probably run by a professionally managed top guy today.

The technocrat understands the risk/reward ratios better than a CEO who has come from outside the co. say only 5 years back. From his valuable experience of past cycles, at times he/she might say this is the time to focus on risk, while at other times he/she might say this time, the risk is more than offset by the potential rewards that the current cycle offers.

A technocrat promoter’s interests are more likely to be aligned with the longer term interests of the company compared to a professional CEO who does not have a big stake in the company and hence his incentives could possibly be short term beneficial and long term damaging at the same time. During an up cycle, the technocrat may say I don’t want to squeeze the last penny out of my suppliers because they will help me back when the tables turn while the external CEO may be thinking, let me squeeze whatever I can right away because my ESOPs would become worth more if I increase this year’s EPS and I will be moving out to a new job next year anyway.

One noteworthy technocrat founder in India would be Narayana Murthy of Infosys. We all know how he took Infy from a 200 Crs market cap in 1994 to about 186000 Crs in 2011, when he retired.

For a technocrat like him the game is more than just the money (most of them consider the moolah as just a byproduct of running their business well). He achieved what most people would have thought, was unbelievable back in the license raj era and even after his retirement he explicitly brought up the issue of high promoter salaries and misaligned incentives. This tells you he probably considered Infy for more than the wealth it gave him. It showed the technocrat founder cared even after he was gone.

Some other noteworthy promoters that I know of, include (not in any particular order) Dilip Shanghvi at Sun Pharma, Sam Walton of Walmart, Jeff Bezos of Amazon and Sanjiv Bajaj of Bajaj Finance. All these technocrats built their businesses ground up, at a time when most competitors were still trying to figure the nitty-gritties out.

What must be the drawback of technocrat-promoter for a company?

Is it possible that his calls of capital allocation may go wrong? Or may be he is good at technical details but he may not properly identify business cycles or economy cycles?

Can anyone explain me the impact of cos. holding higher inventories in times of rapidly rising commodity prices?

My question specifically refers to cotton mills - Most of the mills have halted production due to rapidly rising cotton prices. Accordingly, they are beaten down in valuations by the market. However, some of these mills are holding a large amount of inventory vis-a-vis thr market cap and have staying power thru these tough times. Do these mills represent value buys?

Promoters pledging their shares is one way to raise funds.

Besides promoters, there are other shareholders, say FII, DII, retail etc. So why is only the “promoter” pledging his stake? How’s the risk distributed to the rest of the shareholders? This seems unlike regular debts and equity-based funding which impacts everyone equally. It either reflects as equity dilution or goes as debt in the books.

@Prathamesh_Nalawade Base rates support the idea that most entrepreneurs are good at one business or at best similar line of businesses.

With that in mind, I would say good capital allocation more often than not means reinvesting the money back into the same business. It is a given that the business in question is a scalable high ROE business.

There are some exceptions to the above rule. Very few mortals have the gifted ability to successfully allocate capital to businesses of varying characteristics across varying cycles and varying circumstances.

In the past, in India, one entrepreneur who was known for his excellent capital allocation skills was Ajay Piramal. He’d not only done well at running Piramal Healthcare but also exiting Piramal Healthcare’s business at a premium valuation by selling it to Abbott Labs for about $3.8 Billion.

He’d grown his pharma business inorganically by acquiring Nicholas Laboratories in 1988, Roche Products in 1993, Boehringer Mannhiem in 1996, Hoechst Research Center in 1998, Rhone Poulenc in 2000, and ICI Pharma in 2002. His investment in Vodafone (2011-2014) also fetched decent returns considering the scale of money involved. I am yet to come across another inorganic Indian growth story as good as this one.

That being said, his forays into the lending business over the last decade seem to have backfired and base rates seem to have caught up finally.

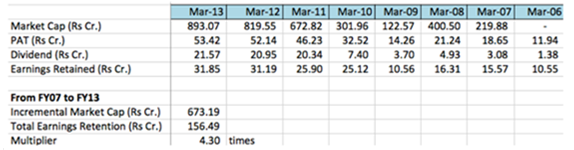

Coming back to good capital allocation, I like the idea of the company being able to create more market value for every rupee of earnings it retains.

For example this is from a post written on Kewal Kiran by Prof. Bakshi. Between 2006 & 2013, Kewal Kiran Clothing retained 156 Crs of profits in their business. During the same period their market cap grew by 673 Crs. This means the company had created 4.30 bucks for every rupee it had retained.

A 4.3x multiplier is a good indicator of good capital allocation because there are a lot of cases where the opposite is true and the incremental market cap is a fraction of the earnings that the company retains over a given time period.