Also One more unrelated query :

Everybody talks about one’s own core competence and while selecting stocks , one should not go out of competence area…But what I am confused about …I am creating a portfolio of atleast 5 sectors with 20 -25 companies…How can I be competent in so many sectors and companies? And if I follow Charlie Munger where he says " Play the game, which you can win" means stay within your competence…Then my circle of competence is so small that I may be able to shortlist just 1 or 2 companies and even that competence is so fragile …That i cant be so sure about…

You are forgetting one important point - time. With time in equity markets, a lot can happen, which more often than not surprises in a positive way. Practice as with in every other field, in equity investing too makes one better. And as Buffett said successful investing takes time. This is very much true, every great thing, every great endeavor takes time. So everyone starts at some point, finds their circle of competence, and owning to different reasons, like family, education, profession, natural ability, some understand quickly, some take time.

After gaining some experience, one can try to expand wings, look at adjacent sectors or a sector that is in demand, or a sector which one in interested in. So while a circle of competence does exist, for many reasons, it is not written in stone, it is not a biological limitation, a person can very well expand it. And if one has expertise in his own domain, then he can look at sectors that are adjacent to his, so on and so forth.

Bears make money too, not just the bulls, so even if the circle is small but competence is good, one can still make money. Say if one chooses only FMCG and IT, he can still make money, provided he has both FA and TA knowledge, because sometimes an entire sector goes into consolidation. Munger said to take a small thing and be serious about it, our own Dr. Hitesh also says the same thing, to keep things simple but be good at them.

I believe this is all part of the journey, until one finds a method, simple or complicated, which makes him satisfied, comfortable and beneficial. Up until then, one can expand in the pursuit of gains, monetary or otherwise. Strengthen what you have and stretch your wings.

On a side note, not every quotation or a phrase said by great investors apply to us. It is often being said that one of Buffett’s rules is to never lose money, but he himself had lost money a few times. So, as all such quotations are not mathematical formulae, we should absorb the essence, not take it to the tee.

This concept is near to my thoughts, hence all this banter. I used to invest in a lot of names, without having any basic understanding at the beginning of my journey, not anymore. Now I have started looking for holes even in the biggest names like Titan or Asian Paints, and could not bring myself to invest in them or allocate small, despite those businesses being relatively near to my circle of competence. This has happened because of some time spent in the market.

My 2 cents.

3 Likes

But then…Our portfolio will be lopsided. We cannot invest into just 2 sectors like you said FMCG and IT.And gaining and expanding competence is a very slow and lengthy process. It cant be done over a short period of time. But constructing a portfolio and allocating capital is a short time process. I cannot keep aside the cash to deploy over 10 years, when I will get sufficient competency in varied sectors.

What I feel is…For a Portfolio construction, We need to identify 5-6 important sectors of the Indian Economy and Then 2-3 top companies in each sector will be selected , based on basic parameters. And then you can start doing deep dive into each of them, If while doing deep dive, you come across Titan, which is not generating consistent profits or sales or losing its moat or its too much of a hassle to cater to ever changing tastes and preferences of customers, you may drop that company after a while , from your portfolio…But to start with, One cannot start with just 1-2 sectors or 2-3 companies. May be we can take help of Fund managers of different AMCs and learn from them, the general rules of portfolio construction. After all why SENSEX is made up of 30 stocks and NIFTY is made up of 50 stocks? There must be some thought process gone into that. It cant be arbitrary. I m not saying that we need to choose all 50 stocks.But proper sector presentation has to be there into your portfolio. After all , finding multibagger individual stocks doesnt make you wealthy …Its CAGR of overall portfolio and consistency of that CAGR makes you wealthy.

I gave FMCG and IT as examples, sometimes some sectors go up and down, one does not have to look at sunrise sectors, because he has no such need. For example, a software engineer with professional experience and expertise may choose only IT, because he knows about it and may not have time to learn about other sectors, and he may even stay invested, or invest more, even if the sector is falling or undergoing consolidation, because he knows that it will go up sooner than later and will reward him good. People invest in cyclicals for the same reason, they know when the cycle will turn.

These all are personal preferences and choices, depending on one’s own professional and financial state, one can choose as to how to invest. People with very busy professional life may not have adequate time for research, and some people can afford time as they want to make good money which may not happen with their current job. There are many ways to skin the cat, many paths to choose from. One can invest in indices, and learn the tropes of direct equity, and slowly move completely, depending on the knowledge, experience and conviction gained. Or one can invest in the promising sectors.

I have read about many kinds of statements from members. Members with concentrated PF who would not look at any other companies, members who have invested in more than 50 stocks, members who would not touch a high PE no matter how actively discussed it is, members who invest only in out of flavor or cyclical, members who get in and out stocks quickly, members who stayed invested for years, members who just dabble, etc etc. To each his own. Their decisions are theirs, in the sense that, they may not be applicable to us the same way.

Broadly speaking I would say, it all depends on time, capital, affordability of loss and expectation, along with the obvious knowledge, experience etc. Then, one can choose whichever path he deems fit for himself and start the journey, change the path if need be or stay the same course.

1 Like

What happens when the price of a company falls and dividend yield remain same.

For eg If I buy coal India during the IPO price ( 350rs) 12yrs back and I am getting the same dividend amount but the share price of coal India has reduced almost 50%( 189rs) from the IPO price can you give clarification on this please

Dividend Yield = Dividends paid / Market Cap

Market Cap changes with fluctuations so yield % will also constantly change. Higher market cap (stock going up) will mean a low Div yield % if the company pays the same dividend amount and vice versa. Coal India’s dividend has gone from 6000Cr 10 years ago to 18000Cr at times to 10500Cr this year. Being a heavy cash flow rich company, it does give out a lot of dividend and since it is government controlled, the dividend amount is based on government decisions to an extent.

Bottomline: Track dividends paid by the company and its trend over the years rather than the dividend yield as that is a transient value.

3 Likes

What happens when Reliance comes out with IPOs for retail and Jio arm. I presume current shareholders won’t get any preferrential allottment and will need to apply via the normal process to gain shareholding in subsidaries. Since, holding discount will start applying on Reliance, won’t current shareholders see significant market cap erosion ?

Hello all,

Have a very basic question.

Let’s say TER (expense) is around 0.2% for a liquid fund, does that mean if I put in 1 Crore in such fund even for 3 months, that I will be charged 20,000 as TER? Idea is to park lumpsum funds somewhere so as to systematically transfer them into equity via staggered investments, but paying 20k as expenses might mean a losing deal. Why does one then just into liquid funds? Because I don’t expect it to generate enough income to beat TER in 3 months. What am I missing?

Regards

Yogi

TER is included in the NAV. We can look into the increase/decrease in NAV to see if we do lose money.

Since your holding period is 3 months, we can easily look into the 3-month rolling returns to get an idea. The increase/decrease in NAV is the gain/loss at hand.

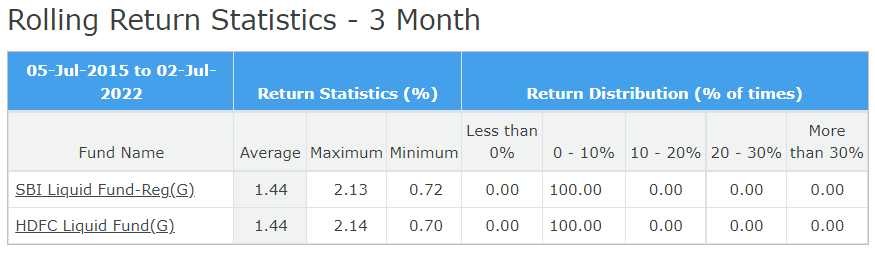

Below is from Mutual Fund Rolling Return | RupeeVest

Over the last 7 years, every 3-month holding period has seen a positive return after all charges (like TER). So, in your example of 0.2% TER, the fund would have incurred that expense annually. But after accounting for these expenses, (assuming average from the above table), you would have got 1,01,44,000 at end of 3 months (since TER is included in the NAV)

Btw, TER calculation is expressed as an annualized percentage…

1 Like

@Mudit.Kushalvardhan Circle of competence does not necessarily mean being good at 1/2/3 particular sectors. It can also mean developing skills in a specific strategy of investing such as deep value, Growth At Reasonable Price (GARP), momentum, Technofunda, Dividend/Earnings yield investing, CANSLIM, Cash bargains, Coffee Can, etc.

There are 2 approaches to solving this problem.

Approach 1

Suppose we choose to get better at the GARP style of investing, then it means learning all the nuts and bolts of this strategy across various market cycles, understanding what works and what doesn’t.

Let’s take GARP. For example, if I were a GARP investor today, would I buy the stock of Dmart today based on their latest quarterly results, given that the stock trades at a massive 150 PE? And if the stock does not meet my idea of a reasonable price, then I better stay away from it because it strays outside the boundaries of my circle.

Staying inside my circle becomes critical when my style of GARP investing does not work under certain market conditions. So if GARP was working during the last bull market and it isn’t working during the current drawdown, then I need to exercise patience and stay inside my circle and wait until the times when GARP will start working again.

There will be times when your style is going to be out of vogue and if you keep trying to shift and you move to something else, you’ll never really get good at any one thing. It can sometimes take years and years to master just one system and I haven’t seen too many people, maybe just a handful, who can multitask many different investing styles.

William O’Neil (or one of his disciples) said - “One of the biggest mistakes you can make is to walk away and stop doing your routine just because the market is currently in a correction. That’s how you miss the next big winners. The best stocks form bases during a market correction then shoot out of the gate right when a new uptrend begins. If you want to catch the next crop of leaders—and cash in on the big profits they deliver—keep doing your routine even when (in fact, especially when) the Market Pulse says “Market in correction.”

O’Neil is basically asking us to keep doing what we were doing when the market was in favor of our style of investing and not stray outside.

Approach 2

The Little bets approach.

This is from one of my fave articles on experimenting in business, investing and so many other areas of life.

"Amazon CEO Jeff Bezos is famous for his drive to take bold bets and experiment on projects that often fail. That approach has led to many flops within Amazon, like its Fire Phone or hotel booking site Amazon Destinations. But it’s also what made major hits like the Amazon Web Services or Kindle devices possible.

One area where I think we are especially distinctive is failure. I believe we are the best place in the world to fail (we have plenty of practice!), and failure and invention are inseparable twins. To invent you have to experiment, and if you know in advance that it’s going to work, it’s not an experiment.

Most large organizations embrace the idea of invention, but are not willing to suffer the string of failed experiments necessary to get there. Outsized returns often come from betting against conventional wisdom, and conventional wisdom is usually right. Given a ten percent chance of a 100 times payoff, you should take that bet every time. But you’re still going to be wrong nine times out of ten.

We all know that if you swing for the fences, you’re going to strike out a lot, but you’re also going to hit some home runs. The difference between baseball and business, however, is that baseball has a truncated outcome distribution. When you swing, no matter how well you connect with the ball, the most runs you can get is four. In business, every once in a while, when you step up to the plate, you can score 1,000 runs. This long-tailed distribution of returns is why it’s important to be bold. Big winners pay for so many experiments."

Here’s another one from Bezos - "If you’re good at course correcting, being wrong may be less costly than you think, whereas being slow is going to be expensive for sure"

So the key ideas from Bezos that we can apply to investing are:

- Be willing to experiment on projects / small investments that you initially perceive “could fail”. The keyword is small.

- One cannot learning without failing. Again, the failure needs to be small.

- Experimentation is necessary to get to the top or to figure out what you are good at.

- Big winners pay for soooo many experiments.

In this very forum, I know of a smart small cap investor who primarily invests in micro caps (a lot of them sub being sub 100 crs market cap cos) that practically nobody looks at. This probably led him to 100s of failures because small caps are inherently riskier and way more volatile than mid and large caps. But it also led him to multi bagger stocks such as

- Ajanta Pharma at 300 Crs Market cap

- Avanti Feeds when the whole co. was available at 35 Crs Mcap

- Mayur Uniquoters at 250 Crs

- MPS at 250 Crs and so on.

Notice that each of the above are unconventional businesses. Each one of the above were considered untouchables by the market because of a cocktail of varying biases such as anti-pharma bias, cyclical sector bias, perceived crooked promoter bias, high promoter salary bias, related party transaction bias, etc. Yet, he seems to have experimented with cos that were outside his circle, perhaps failed in some of his small (and maybe big) bets, persisted, and landed some big winners.

Cutting losses quickly

Another big idea when it comes to thinking of experimenting with one’s portfolio is that of stop losses. Over our investing careers, we can and will go wrong with some of our bets that are outside our circle and there is no shame in cutting losses quickly, note down our learnings, improve and move on to the next set of experimental bets. These stop losses can be based on price action, business results and/or both.

As Bezos says, be good at course correcting. Basically, kill small experimental bets quickly and gradually build conviction and allocate more capital to big winners that are working out as expected or better yet, working out wayyy better than what our biased minds expected at the time of our first buy orders in those experimental small bets.

21 Likes

Very apt analysis. Your post gave me another line of thinking about Circle of competence. I always used to think, its about sectors and companies, never really thought this dimension of competence regarding a style of invetsment. Thank a lot.

1 Like

If shares in PMS are held by the PMS investors in their own demat account (retail/public category) then how/why do PMS house names like Abakkus, Sage One, Old Bridge, Marcellus etc. appear in bulk deals?

@sahil_vi @Chins @arjunbadola others?

1 Like

May be they have a Model Portfolio of PMS and then as per that model they make purchases and sale in the portfolio of clients, in respective clients’ dmat account.

1 Like

PMS providers have a custodian (usually one of the known brokers) who actually holds the shares. My guess is these calculations are based on transactions via the custodian account.

1 Like

What is difference between Marketplace vs Platform vs e-Commerce with example?

Hi-

Derivative market is forward-looking at least by a quarter. I am exploring this field in recent times. I have 2 Qs and would appreciate any thoughts or a good resource around this?

- Do you use any indicators (E.g. India VIX, Option Chain Analysis - To find Support/Resistance, Volatility Skew, and Put-Call Ratio) from the Derivative market to sense the mood of the market participants in the near term? If yes, could you share your approach with an example for a layman?

- Do you manage the portfolio risk using extreme OTM Puts? What’s been your experience- Pros & Cons? Is it worth doing?

TIA

Regarding Annual Reports

It’s already results season for FY23 Q1, but many companies are yet to provide Annual Report for FY22. Few questions:

- Is it mandatory for companies to publish Annual Reports?

- Isn’t there a deadline given for companies to publish Annual Reports?

- Till what time can we expect to wait?

Thank you for any help.

1- I think yes else many will not publish.

2- A cut-off may not exist. But, it shall come before AGM.

3- If they make you wait so much, better to switch businesses.

Just answered from my common sense. No data to back it up.

1 Like

There are many members in the forum, in thousands. And they are different from different professions, different age groups and have different priorities.

There are many members who have PF threads. They have different investing styles. You can check these threads to understand their investing styles. Some may go by the numbers, and some by the business. Some mathematical, some quantitative and qualitative aspects.

And of course, some members don’t change their styles, but change stocks, and some tinker with their styles. Not all 't explicitly mention what they look for before investing, but it is more than explained in their rationale for their stocks.

So if you are interested and have not done it, check their threads, it will be helpful. It may feel like scratching the surface and an occasional deep dive.

2 Likes

Just 1 query about Annual reports in general. I read Annual reports regularly now a days. But what I feel is , other than reading qualitative factors like product categories, Capex done or innprocess and managment discussion, other financial statememts, be it Balance sheet, cash flow or P and L, all these are available in screener and even we can easily compare it with previous quarters and Years. So doe it male sense to read financial statememts in Annual reports?

Qualitative factors and discussions , offcourse yes but can we rely on screener for financial statements?