You can find them on https://www.researchbytes.com/

They have got audio and transcripts.

You can find them on https://www.researchbytes.com/

They have got audio and transcripts.

Just wanted to clarify a basic question -

Why are interest payments not subtracted to calculate FCF? FCF is essentially the cash available at the end of the year after deducting operating and capital expenses. Isn’t interest expense also the cost required to run the business? I feel interest is separate from other capital allocation decisions in the way that it isn’t discretionary. You have to pay it.

For example, two companies make 100 cr of FCF at the end of the year and one has no debt while the other company has to pay almost 80-90 cr of it in interest payments, at the end of the year the cash generated is starkly different from the FCF number. Both companies might look similar if you value them using FCF but the real cash generated over a long period will very different.

There are two kinds of FCFs, FCFF & FCFE; Free Cash Flow to Firm & Free Cash Flow to Equity.

If you want to value the firm you use FCFF. If you want to value the equity in a firm, you use FCFE.

FCFE considers the interest payments.

You can get the equity value using FCFF but you need to subtract the deb value from the firm value to get equity valuation.

You might want to read/listen to Ashwath Damodaram to understand more.

Hi @ChaitanyaC - thanks for this, however when i try to download/access any doc/audio, it gives me some error. Tried from multiple devices but its same for all.

Any other way/site?

Try Internet Explorer with no ad blocking. It works. You get access to both audio and transcripts.

Also, you can check Trendlyne youtube channel.

Dear members,

Would be grateful if anyone can explain basic stock report query…

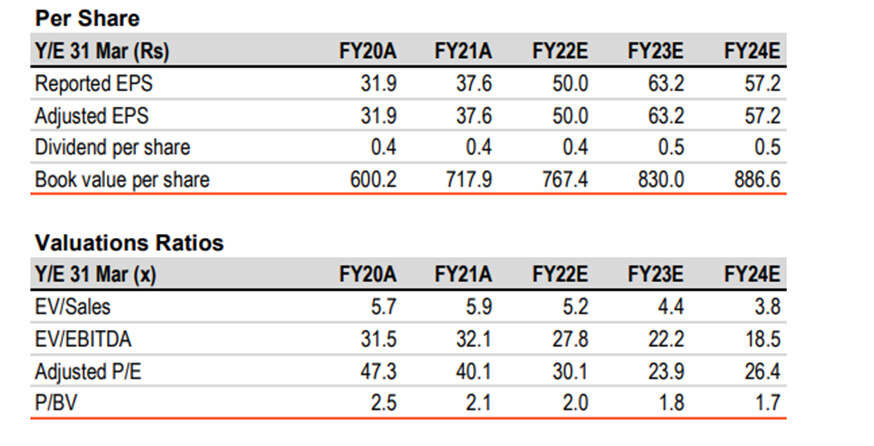

In Zydus Wellness report by BOB Caps, it is mentioned…

Initiate with BUY: We expect a revenue/EBITDA/PAT CAGR of 10%/14.2%/11%

over FY21-FY24 to Rs 25bn/Rs 5.1bn/Rs 3.7bn.

Initiate with BUY and a TP of Rs 2,185, set at 38x FY24E EPS, for 45% upside potential.

Query (1): Here 38 is PE as on March 24? Price of Rs 2,185 on March 24? So the EPS on FY24 would be 57.5?

But the financials mentioned is as follows…

Query (2): Here for FY24 the PE is mentioned of 26.4. As per the above calculation the PE should have been 38… no? Also the EPS mentioned is of 57.2 (vis 57.5 as calculated above)

If PE of 26.4 is considered with EPS of 57.2 then it will give target price of Rs 1,510 (vis target price of Rs 2,185) (!?)

How to read such reports?

Yes, correct. He is assuming EPS of FY24 to be Rs.57.5. On that a P/E of 38 at that time gives a price target of Rs.2185

Here, he is taking the current market price of Rs.1510 (or thereabouts) and dividing by EPS of Rs.57.2 in FY24 gives a forward P/E of 26.4 X. The implied argument is that since the EPS in FY24 is going to be Rs.57.2, and today’s price is Rs.1510, the stock is available at a P/E of just 26.4 times.

This latter part is a common trick used by sell side reports to show stock as “cheap” (dividing Current Market Price by future EPS). It is logically incorrect and inconsistent, since in any ratio the numerator and denominator should belong to the same time interval. Best to ignore it.

oh okay, so this is what forward PE is.

Thank you Chandragupta bhai.

Hi fellow investors.

What does everyone feel an acceptable financial leverage ratio is ? By definition, 0.5 is the maximum acceptable but in Indian context, even many businesses like PI Ind. etc. trade at >1, avg. businesses are more in the range 2-6. Is it fair to tweak the expectations and till what ranges.

Is ROA the better metric to track to ROE ?

A “good” debt:equity ratio is probably going to be different for different in investors based on the risk they are willing to take. There isn’t a magic number/range.

From the company point of view, it’s all about how they run the business and how they make use of the money. Obviously, a company that expands using money from operations that are sustainable can continue to grow without external needs. But some very good run companies have grown through debt raising as well (See Deepak Nitrite history).

If they take on debt, are they able to finance that debt without stressing the balance sheet? Are they able to put that money to best use (capital allocation)? Are they able to generate returns from that money greater than cost of that capital? These are probably some of the Qs you need to ask to judge if a higher debt company is worth investing in.

I may have failed to explain the question better here. I am well versed with debt “pros” and it’s sustainability . My ask was more in regards to looking at factors WITHOUT taking financial leverage in consideration i.e. is the business not able to generate enough FCF , cash balance etc. despite it’s maturity. Is it better to track ROIIC or ROA instead of ROE for such businesses unless the business is wanting to dive into a completely unknown and new vertical.

My apologies for misunderstanding the question.

Have found these posts by Dr. Malik on FCF and SSGR analysis helpful on evaluating how the company is doing. Free Cash Flow: A Complete Guide to Understanding FCF - Dr Vijay Malik

Calculate Self Sustainable Growth Rate (SSGR) of a company - Dr Vijay Malik

End of the day, the problem with most of the return ratios is that they are lagging indicators. If the return ratios are trending upwards, the capital/assets are being put to good use. By the time the ratios show the uptrend, the margin of safety in valuation of the stock would have probably gone. Tracking the management guidance and past track record would give us ability to judge whether that capital (debt or equity or internal accruals led) is going to be best used. This though is a subjective analysis than something objective through numbers.

Thank you!

If the share capital (number of shares x face value per share) is Rs 5 crore, and a 1:1 bonus is awarded, the share capital becomes Rs 10 crore. The face value does not change whereas the number of shares becomes double. To do this, the company transfers Rs 5 crore from its reserves to the share capital. Thus, bonus can be thought of as a form of dividend. [A company with empty reserves cannot give bonus without getting into negative reserves].

1:1 split will reduce face value from Rs 10 to Rs 5 and double the number of shares. Splitting of share reduces the face value and does not change the share capital. Thus, it is not a dividend. It is only used to half the share price, to increase liquidity.

1:1 bonus as well as 1:1 split will double the number of shares. Thus, the book value per share will become half. Bonus issue does not change the total assets or total liabilities.

A higher share price allows a company to raise funds at favorable terms, e.g., via preferential issue. If a company never pays dividend, nor issues bonus shares, it may be construed as not friendly to the shareholders. There are many listed companies (many of them cheap) that do not share gains with the minority shareholders. The market may mark down the price of such shares.

1:1 Bonus issue too halves the share price the way 1:1 split does. How will that reward investors?

Bonus issue is usually a small dividend, so it can be lost within the daily fluctuations of the stock price. In the previous example, the key difference between bonus and split is Rs 5 in the face value (and that too is not cash in the hands of the shareholders). If the share price is Rs 100, the difference is merely 5%.

In 2018, Ingersoll Rand declared a huge dividend of around Rs 200 when its share price was around Rs 650. To give such an award via bonus would require the company to give around 20:1 bonus (20 bonus shares for each share) if the face value is Rs 10. Such bonus is unheard of, justifiably since it will suddenly increase the number of shares by a lot. Point is, bonus is a mechanism restricted to a small dividend.

Hi All,

Is there a way to find out in which all indices a stock is present in? A tool or a website which will check across all the various indices such as those on BSE / NSE, MSCI etc. and return a list of indices in which the given stock is present.

Thanks.

P.S.: If no such tool exists, might be a useful feature to build. @ayushmit @Sidhegde

https://ticker.finology.in has this information.

Eg: ITC Share Price, Financials and Stock Analysis

Scroll down the page you will see a section: “Index Presence”

Regards.

Yes, got it. Thanks a lot.

Any particular reason which you can share for this query?

All the major stocks will be having their presence in all the market cap weighted indices, and as many factor based indices can be created, with little differences, some stocks will not be present in such indices. But these sometimes have only back testing history, no real time history, no ETFs or funds available to invest, and the possibility of change in their nature going forward.

I am an index enthusiast, so I am asking this question.