Of course. When one gets experienced, he looks at things in a nuanced way. For absolute beginners, the results you have mentioned are just fine - Asiants Paints, Infosys, TCS, Abbott and the likes. When one starts investing in such companies, unless there is a threat to the underlying business, which the managements of such businesses are aware of, there will not be capital loss. So for beginners, investing in stocks with a set of defined filters will be beneficial. And as one progresses, can differentiate and understand businesses on the merits of qualitative and quantitative parameters, there are many paths to choose.

I have a very newbie / unseasoned investor problem.

My portfolio has grown big with a lot of tail stocks (total 50+ and tail may be 30+) which I have taken up as tracking positions.

Now I am struggling to reduce the number of companies to trackable few (say 20) but since all look to have great future I am not able to let them go.

How should I proceed and trim the portfolio to 20 companies?

I know tail stocks even if they double they won’t make any meaningful impact on the portfolio.

If I sell all the tails I might be left with 20 out of which some of them may not be as great as the tails I had let go.

Because of this fear I am not able to sell the tails.

As buffet says for a question why you have not invested in X company ? His response was "I cannot attend every party in the city "

Take an approach something like this

You group them first based on the sector

Identify which sector has strong tail winds

From each of the group find which business you understand most and you have bandwidth to track them on qaurterly basis.

If you still have more than one in each group then do financial ratio analysis , compare the immediate growth triggers. This will help you to consolidate.

It is also perfectly fine to take a basket approach in one sector.

This is part of the journey. Most people when they gain experience, slowly gravitate towards core and satellite PFs, as they are convinced of their picks. Takes time.

Nothing wrong with having a 50 stocks PF either, or even 70, in the sense that if the tail is meant to be a tail. If there is no expectation from the tail, and if you can afford the loss of capital, allocated to the tail, leave the tail be and focus on your core PF. But if there is an expectation, there is a concern, and can allocate time, follow the tail regularly, and if some of the tail stocks show promise and progress, and if you are convinced, you can allocate meaningfully and move such stocks to the core PF. This happens too, and these need not be sunrise businesses, these could be century old business too.

It all boils down to why is a particular stock in the PF, does it meant to be a long term one - one that could be held for a few years, or a high growth stock - one that will be held until proven otherwise, or a fancy one - ride the momentum and get out, a cyclical, a contrarian, an undervalued, what is it?

I am sure you can answer yourself, because you are clear about the status of your PF, failing to do so will result in clutter. Having a small body and long tail may look odd but it is not clutter, it is a design.

A high ROE co. will not necessarily mean high returns for shareholders because most high ROE co’s are priced accordingly by the market.

If one is looking for above average returns, one needs to focus on situations where the ROE is turning better. In most cases, this happens in companies where the profitability is increasing due to tail winds for the sector caused by factors beyond the company’s control.

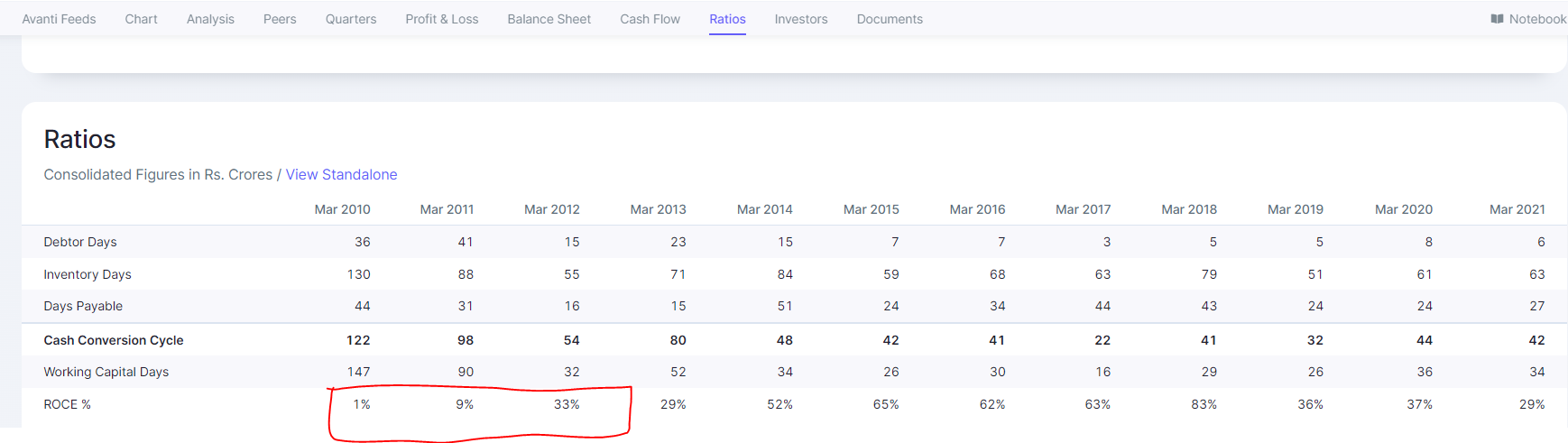

Take Avanti Feeds for example.

Before 2010, it was a loss making co. hence negative ROE.

And when things turned around, starting from 2012, their return ratios just took flight.

Even until 2013-14, the stock used to trade at single digit PE multiples because there were apprehensions about whether or not the growth / ROE would sustain. Some of the posts on the Avanti Feeds page are worth reading and re-reading on the kind of challenges an investor goes through mentally when return ratios go from single digits to high double digits.

Highest levels of mismanagerment in one of the most regulated areas of India. Something that has made India a laughing stock in foreign media and probably something each one of us is laughing at too. NSE

This is hugely concerning. Thanks for sharing. The Rs 3 crore fine is not even slap on the wrist. There should be punitive fine in this case (may be 100-1000x) so that such behavior is not repeated. SEBI has made a joke of the whole case having failed to identify this baba.

Most concerning is the scam happening inside NSE, see there is co-location scam, and people are demanding through investigations, there are numerous evidences now, and still SEBI is doing nothing. There is whole lot of big people involved in this scam, and everyone in the system is getting monetary reward by some way or other.

low float low equity has both sides it could become illiquid stock as well and become multi bagger if company has good growth ahead in my opinion fine organics could be low float multi bagger .low float means less freely traded shares and low equity means less outstanding shares

Hey, read ur response. Just wanted to understand , in your mid para you mentioned about pick a company where you understand its business. What exactly do you look in such cases?

Each co will claim it has competetive adv over others.

A gain on inventory will never appear in any companies profit and loss account because of the accounting standards/Indian accounting standards.

As per the accounting policies the inventories are always to be valued at lower of cost and net realisable value considering prudence. Hence, there will be no unrealised profits which will be recorded on unsold inventory.

As far as write down/write off for inventories is concerned it would also not appear seperately and would be forming a part of changes in inventory in p&l account. Further you may look out for “provisions for slow/non moving inventories made” in annual report or other disclosures.

what is the difference between direct assignment and balance transfer in HFCs from the HFC perspective? Why do we hear balance transfer is bad and direct assignment is good?

In both cases, they got the processing fee, they service the loan for some time and move/sell/transfer it to other party, all the interest will be accrued to other party and not the HFCs. In both cases, they get upfront money during the transaction.

In case of non-repayment, for direct assignment, they have to use their workforce to do the recovery effort, but in case of a balance transfer, the loan itself is bought by another HFC/Bank, so they will do the recovery effort.

I understand BT will reduce the AUM, but the same will happen in the case of direct assignment. In many concalls i hear analysts are giving a worrying sign incase of BT, but the same company is willingly doing direct assignments.

I have a share manpasand beverages which is not trading in exchanges since 2020 and shows in demat account. Now i need to book this as loss and consider in the next IT filing. Any body know what is the procedure ?

Can someone point me to the place where I can find transcripts / audio for quarterly con calls / investor calls (i want to get the quarterly calls transcripts specifically for Nitin Spinners)?

I think this may be mentioned somewhere already where to find it but I could not locate it as the browser search function does not work on all the articles of the thread. Hence apologies for asking this again and thanks in advance.