@Bhambri3 Pre IND AS is Indian GAAP. Company could have followed Indian GAAP and now its following Ind AS. In both accounting standards we might get different EBITDA for same year. So they have higjhlighted this

I understand that. I want to konw what is the difference in terms of accounting as most of the QSR chains are giving both numbers and the difference in EBIDTA margins is almost 150-200 bps.

Sharing for others benefit even though I asked and now answering the question.

Below business mentioned it explicitly in the Statement of the Cash Flow (last entry). Few other businesses that I explored for this topic mentioned that it’s adjusted while disclosing ‘Changes to Inventory’ under expenses as it’s an immaterial amount for them.

| // | Bayer CropScience Ltd | FY 21 | FY 20 | FY 19 | FY 18 | FY 17 |

|---|---|---|---|---|---|---|

| Cash Flow from Operating Activities: | ||||||

| PBT | 795 | 583 | 480 | 404 | 448 | |

| Adj.: | 62 | 191 | 67 | 37 | 6 | |

| Exceptional Items | -5 | 130 | - | - | - | |

| DA | 74 | 65 | 44 | 33 | 29 | |

| Finance Cost | 13 | 14 | 10 | 11 | 7 | |

| Interest Income | -28 | -19 | -14 | -17 | -40 | |

| Div. Income: FVPL | -0 | -11 | -15 | -7 | -9 | |

| Rental Income | -9 | -9 | -7 | -4 | -4 | |

| Provision - Written Back | - | -5 | ||||

| Penal Interest (Over. Reciv.) | -4 | -5 | -1 | |||

| (Profit)/loss on Tang. Asset Sold | -6 | -8 | 2 | 0 | -1 | |

| (Profit)/loss on InTang. Asset Sold | 0 | 1 | 6 | |||

| Profit on Sale of Investments | -9 | -0 | -1 | |||

| Bad Debts | 2 | 1 | 1 | - | 2 | |

| Provision - ECL(Reciv.) | 3 | 3 | 6 | 3 | 9 | |

| Provision for Indirect Tax & Other Comm. Matters | - | -1 | ||||

| Inventory Write-Off/Write Down | 34 | 29 | 34 | 18 | 13 |

2 Likes

How do warrants work and how good and bad promotors use it?

2 Likes

What factors would a seasoned investor look at to:

- Assess the strength of a balance sheet (at a point in time)

- Ascertain if the balance sheet is strengthening over time

Thank you!

1 Like

@Suyog_Patil You may want to read how Indo Count’s promoters benefitted by issuing warrants to themselves, for a song at

Basically, in this case, promoters issued warrants to themselves, right when the business was coming out of the woods, thereby diluting equity at a time that was the most damaging to minority shareholders and most beneficial to promoters.

This article also shows what happens when promoters decide to take more than their fair share of the pie, by benefitting from information asymmetry (promoters knew when exactly the company was coming out of bankruptcy, whereas minority shareholders did not).

This case study also shows us that despite what some would consider as selfish promoters, the stock went up 50x from the time these warrants were issued.

In exceptional cases such as this one, provided there are strong tail winds for the business, it may some times make sense to partner with promoters who are not the most ideal.

Like Prof. Bakshi drew an analogy somewhere between marriages and partnering with promoters “Keep your eyes wide open before marriage and partly shut thereafter.” ![]()

14 Likes

Thanks a lot, will go through the article

Per my thinking:

Near-Term Sustainability Checks:

- Current Ratio: 2x (Preferred else investigate)

- Quick Ratio: 1x (Preferred else investigate)

- Manageable Interest bearing liabilities (Debt) payment schedule | w.r.t Free Cash Flow ability of the business

Long-Term Sustainability Checks:

- Non-Current Assets < Non-Current Liabilities

- Debt to Equity: Trending towards ZERO

Liabilities Side Checks:

- Share Capital – Trending down or Remains Constant

- Other Equity/Retained Earnings – Trending up

- Debt – Trending down

- Non- Interest bearing liabilities (Anything except Equity and Debt) – Trending up

Asset Side Checks:

- Liquid Assets (Cash, Bank Balances and Investments) - Trending Up

- Trend of fixed assets and working capital assets(inventory and receivables) w.r.t growth in sales and strategy of the business

Overall Checks:

- B/S must be expanding.

- Create common Size B/S and find answers for changes (up/down) that stand out.

- Read notes to understand items that do not show up explicitly on the B/S. For example - Capital Commitments, Contingent Liabilities, accounting principles for Depreciation, Inventory, Revenue Recognition, Defined Benefit Obligations, nature of various provisions and reserves.

Note: Novice Investor. Hoping others would refine or enlighten my blind spots

3 Likes

@Apurva_Dubey In addition to what @Surender has mentioned, these are the factors investors usually look at in the balance sheet.

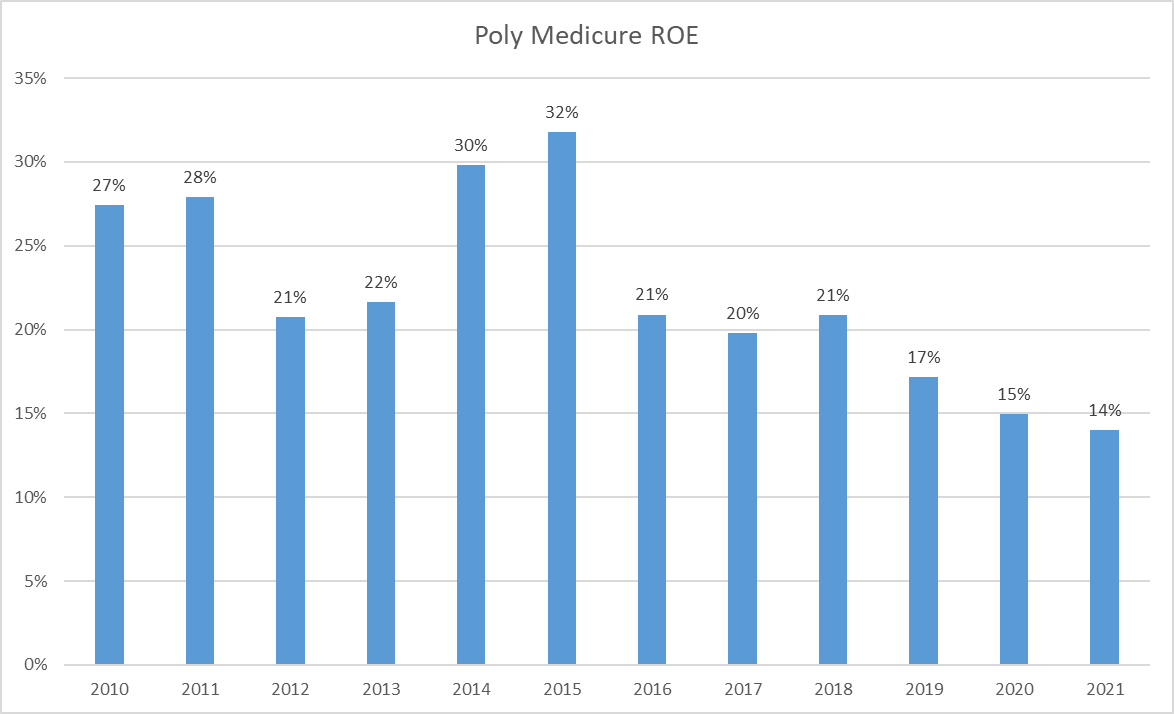

- Trend of Profits in relation to Equity on the balance sheet aka Return on Equity should ideally be increasing. Let us take an example of Poly Medicure.

From 2010 to 2015, life was good for the co. PAT & Reserves were growing in sync. And then in 2016, something must have happened to cause reserves to grow faster than PAT. Perhaps it was Capex related. Maybe it wasn’t. But it does tell you something happened and that you need to dig deeper.

The inflection point on the balance sheet in this case was 2015-16. In hindsight, one should have introspected once the ROE dropped in 2016, although the ROE was still an awesome 21% (which was comparable to similar ROE achieved just 2 years prior)

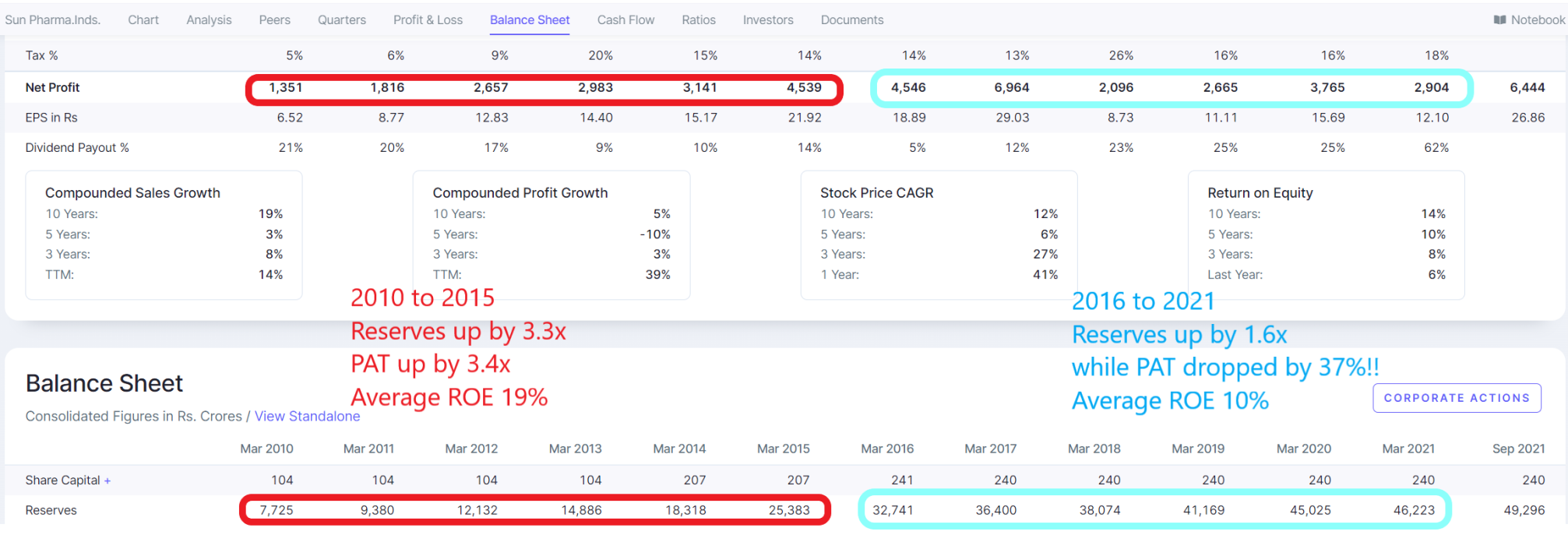

Something similar happens in the case of acquisitions. Take the case of Sun Pharma’s $3.2 Billion acquisition of Ranbaxy in 2015. PAT did not keep pace with reserves (declining ROEs) and things started to look not as rosy as they’d been pre-acquisition.

And here’s what happened to Sun Pharma’s stock price post the Ranbaxy acquisition.

Basically what used to be a multibagger growth stock has been a sob story since the time of that fateful acquisition. Sun’s name used to be taken in the same breath as that of the fast growers of the pre 2015 era but today almost nobody hears about it or at least I haven’t.

So it always makes sense to compare trends in profits vs the trend in reserves on the balance sheet.

Other balance sheet items such as receivables/payables/debt/liabilities that are accounting liabilities but not actual liabilities in the real practical world, have been beautifully covered by Prof. Bakshi in his benchmark articles on the concept of floats / negative working capital at the below links.

Flirting with Floats: Part I

Flirting with Floats: Part II

Flirting with Floats: Part III

12 Likes

If a company re invests its profit, does it need to pay tax on profit first and then re invest or no need to pay tax?

where would we find re investment of profit in statement? is it from Cash flow statement?

Dmart is expanding its operation and it needs capital. It also raised money by issuing shares worth 4000 cr. If we look at the year 2020. Dmart has made operating profit of 2128cr. and net profit 1301.

How much money does dmat have for reinvestment? is it 6128( QIP - 4000 + operating profit 2128)? or is it 5301( QIP 4000+ net profit 1301)

How to find out, how much dmart has spent on creating new stores? is it 1712? if it is the case, where did remaining balance go?

Did Dmart put remaining balance into other assets?

2 Likes

Thank you @barathmukhi @Surender for taking out time to answer my question!

1 Like

Hello guys

This query is related to demerged subsidiary ( partially owned by parent ) getting listed via IPO , in such case what benifit do existing shareholders get ?

Is any provision that they might get some ratio in newly getting listed Co or

They might get to apply this ipo under shareholders quota ( does it really benifit ? )

Most of ipo proceedings will only be used to reduce debt of parent Co ( and there by improving its valuation)

So with above options or any additional benifits , does it really benifit to existing shareholders compared to demrger option. (Case in point is Strides - Stelis).

Thanks

Dear @barathmukhi @Surender,

I have a follow up question on balance sheets;

If you were looking at the balance sheet of Future Retail in 2019, what elements would have indicated an impending doom (if any):

@Apurva_Dubey : In hindsight, finding reasons is a no brainer ![]()

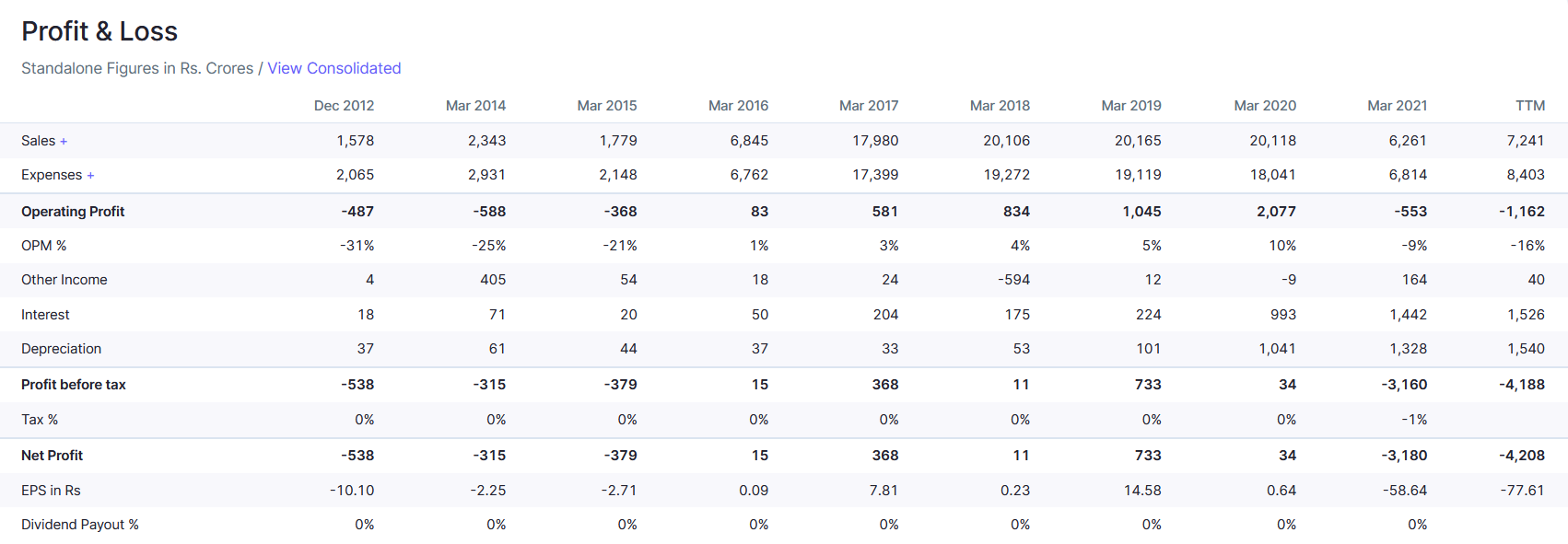

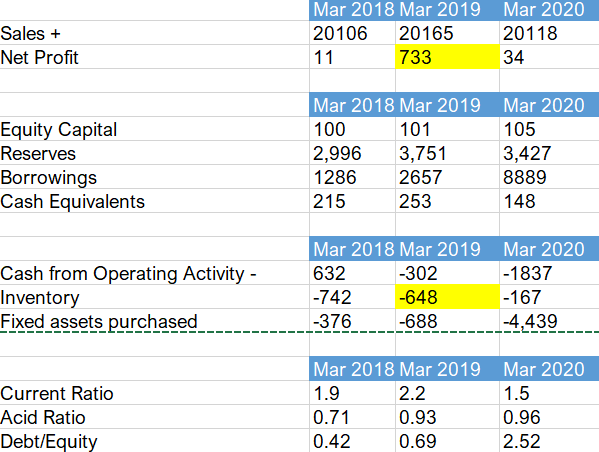

Good question as this needs a view on all the 3 statements. Just on the face of FY19 balance sheet, nothing stands out as ‘Killer’ items.

‘END’ values of the standard ratios -Current Ratio (2.2), Acid Ratio(0.93) and total debt to equity ratio (0.69) - look reasonable, both absolutely as well as relatively. But, upcoming deterioration of these ratios could be inferred as soon as one shifts focus to ‘MEANS’ leveraged to manage these ratios.

On the Income statement, 90% of the net profit (733 Cr.) is the result of Inventory buildup/gain (648 Cr.). Also, Sales growth in FY19 is NIL.

What’s the point?

- The above lever increased the total equity by that much amount. Consequently, the total debt to equity ratio did NOT slide to 0.84 from 0.69 …

Well Managed !!! - Above action sucked away 60% of the ‘Cash from Operating Activity’ …

Super Harmful !!!

Let’s do some Pre-mortem at the end of FY19:

FY20 starts → Business is a going concern. → Cash is needed to support expenses, working capital and growth/capex. → To raise funds, borrowing or diluting equity are the only options. → Ratios would have no choice but to deteriorate.

Business did both:

| Mar 2018 | Mar 2019 | Mar 2020 | |

|---|---|---|---|

| Proceeds from shares | 148 | 1 | 1,266 |

| Proceeds from borrowings | 0 | 1,329 | 5,999 |

‘Cash from Operating Activity’ worsened in FY20. Beside standard ratios, I look at another ratio that ties PnL with Cash Flow Statement:

| Mar 2018 | Mar 2019 | Mar 2020 | |

|---|---|---|---|

| Interest Coverage Ratio: Interest Expense/Free Op. Cash Flow | 0.68 | -0.23 | -0.07 |

Note:

- Never studied this business.

- Above narrative is based on numbers shown on our beloved

screener - I might be drawing bulls eye around my inferences.

3 Likes

@Mani_Starter Retained earnings are added to reserves on the balance sheet.

For deep diving, you may want to do a fund flow analysis using the approach outlined in the below video

2 Likes

@Apurva_Dubey The answer would lie outside this balance sheet, in the concept of opportunity costs.

Sitting in 2019, one of the primary reasons, one would avoid this business would be the lack of tail winds for the sector. Most entrepreneurs are tail wind tigers. Without tail winds for a sector, even the best of managements struggle to make meaningful returns for shareholders.

Yet, if we were forced to consider this business, I would deep dive into their cash flow statement. Something was certainly not right with their working capital management. I would deep dive into increasing inventories and decreasing payables.

Btw, based on hearsay, what I know is that this co. has a history of not valuing inventories the way they should be.

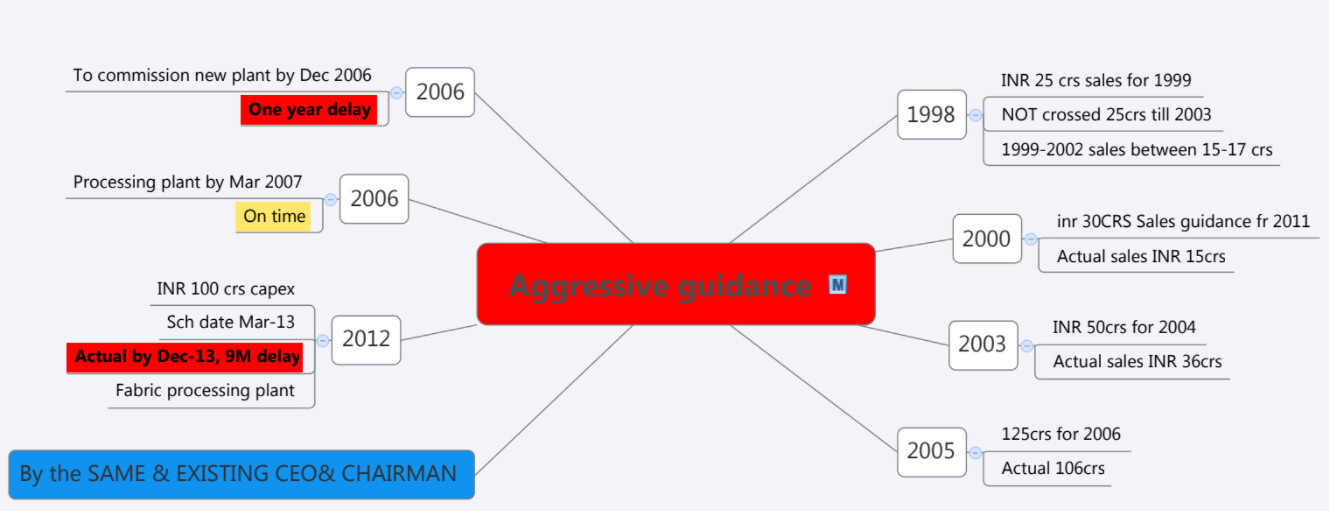

The point is not all answers lie in the financial statements and some red flags are spotted in things like management commitment vs delivery, accounting policies, debt aversion, etc. At the risk of digressing from the topic, to give you an example of red flags not found in financial statements, here’s one. This was an analysis by one investor to check whether Kitex Garments’ management was aggressive in their guidance or were they being conservative and it became clear conservatism was not present at all.

This holds good for Future Group’s management as well.

In 2017, Mr. Biyani was saying they will target 1.50 Lac Crs by 2022, implying a CAGR of 53% over a 5 year period.

Actual numbers until 2019 were way way way off the mark.

Hope this helped ![]()

7 Likes

@Apurva_Dubey Just adding a slightly different angle:

An important thing in investing is to eliminate stocks early. Not to waste time analyzing wrong type of stocks. There is no shortage of good businesses in India, valuation and timing is where the skill lies.

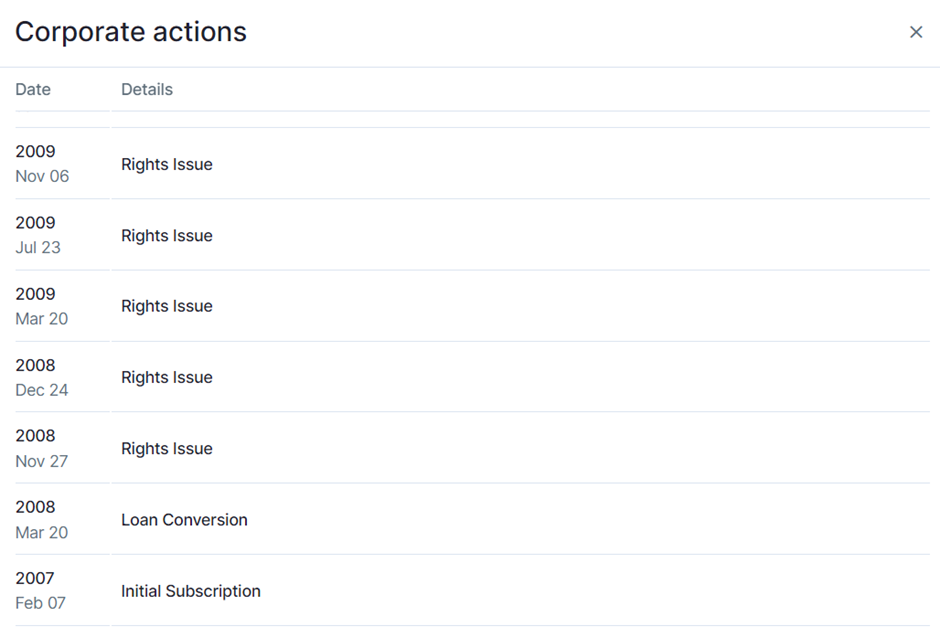

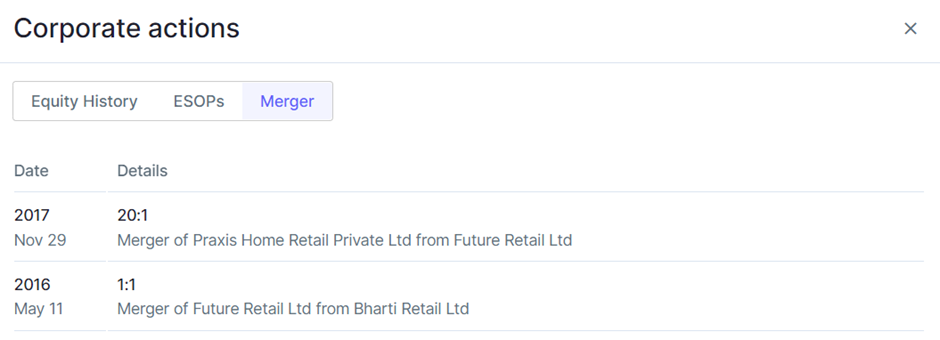

Sitting in 2019, a 60-second glance at Future Retail’s numbers would show this:

Share Capital base moving from Rs.533 crore to Rs.1399 crore, then down to Rs.9 crore and back up to Rs.109 crore? What really is going on here? For comparison, here is the share capital of Asian Paints:

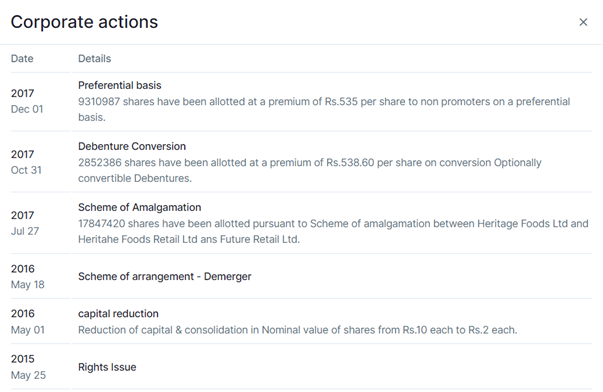

Coming back to Future Retail, we dig a little more and find this:

And this:

Merger, Demergers, Rights Issues, Capital Reductions, Loan Conversions, Debenture Conversions, Preferential Issues…this has been going on with this group ever since last 15 - 20 years that I can remember. They have been playing with their corporate structure like an infant plays with a toy. Forget predicting the future, one cannot even analyze the past here because no two consecutive statements will ever be comparable. Such things don’t happen by chance, they are by design.

If one wants to buy Red Flags, Future Retail has plenty of options ! ![]()

22 Likes

Can anyone please suggest me some good books to read and learn on options trading. For both beginners and advanced or any good professional courses that you can suggest to learn

@Chandragupta @barathmukhi @Surender – many thanks for taking out time to answer my question. There is a book worth of knowledge in these three responses

1 Like

@barathmukhi has said rightly about the ROE. I would like to add my experience here. I used to screen companies which were having very good ROCE and ROE and that is how normally we are taught, invest in companies which have solid return ratios for shareholders. I dont say it is wrong but at the same time its not entirely correct, which later I realized.

If one screens companies which have excellent ROE/ROCE, the companies that come up on screen are the likes of Asian Paints, Infosys, TCS, Abbott etc where ROEs are more than 40-50. If one had invested, say 3 years back, in such companies would have ended up making decent amounts of money at portfolio level.

But I find extremely large sized returns are given by those stocks where the ROE/ROCE is continuously increasing on account of improving sales and consequently, increasing profits. Here not only the stock price gets rerated on account of increase in profits but PE itself many a times gets re-rated.

The recent example is Laurus. When we had started investing, if I am not wrong, the ROCE was 16. A normal screener with ROE greater than 20 would have excluded the stock and that is how I used to eliminate stocks in the past where ROE was less than 15-20. But we all know what happened later to the stock. It was a time bomb ticking. Operating Leverage, Margin expansion, increased sales, profits and ROCE from 16 went to 30s. PE got rerated and stock price went of the roof. Bharat may be having many such examples.

3 Likes