In the balance sheet when CWIP is increased from 1 to 6.

in the same year , under the sub heading of capital wip of cash flow from investing activities there is decrease of 5 crore.

the above process is understandable.

but in the next year , in the balance sheet when CWIP decrease from 6 to 4 .

there is a increase of 2 crore in the cwip under the sub heading of cash flow from investing activites. how does this money comes back which has been spend last year itself

I have read at multiple sources that we should read Independent Auditor’s Report but I am not aware what to read/look out for in the report ?

Also, If the objective is only to identify financial fraud, does reading Auditor’s Report for Bluechip firms is valuable

Would be really helpful if anyone can share any links/docs which guides on how to extract information from Auditor’s report

Hello,

Is there a resource where AGM videos/transcripts have been complied for recent AGMs.

Looking specifically for Jagran, VST ind, godfrey phillips and ITC.

Thanks

How to calculate Sharpe Ratio in excel using stock closing price and volatility data provided by NSE? Thanks Sir.

@barathmukhi what is the difference between capacity utilization vs asset turnover ?

2 Likes

Capacity utilisation essentially means how much of the capacity is currently being used for production. Eg:- suppose you have a plant that makes 10 units and currently 6 are being produced. Capscity Utilisation is 60% and 40% remains unutilised.

Capacity utilisation is a very good concept when it comes to cyclicals or companies where a substantial capex has been done but the capacity remains unutilized due to low demand or regulatory approvals not being completed. Eg:- Laurus between 2017-2019 and Syngene currently (expect approval from Usfda in FY24). Another example that comes to mind is indoco remedies where the capacity is built but remains underutilized due to regulatory issues. Now, since the regulatory issues have been resolved, Utilisation levels will start to inch up. Also check Apl apollo 2.5 million capacity and how much it was utlilized as a homework in 2019-2020+for Balkrishna industries from 2017-2019. Will be good for you to get the numbers from the concalls and presentations

Coming to Asset turns:-

-

Gross Asset Turns or also known as gross block turnover. Reflects the sale that is generated by per Rs of gross asset on the balance sheet. Eg:- You bought Machinery for your business worth let’s say Rs10 and that helps you to do sales worth Rs 15. We can as an example say the gross asset turns of the machine is 1.5 times. This helps analysts or from a business point of view to analyse what the future potential of the sales could be if more machinery is added or the Utilisation of past machinery increases (what peak sales could be achieved).

-

Net Asset turns or also known as net block turnover reflects the sales that are generated from assets net of accumulated depreciation.

Suppose you bought the machinery worth Rs 10 and you use a straight line method of depreciation. After 2 years, the value of the machinery on your balance sheet would be Rs8. If machine is generating Rs 1.6 worth of sales. Then net block turnover is 2 times. Sales/Net Assets.

Important to note what you see on the balance sheet is nothing but Net fixed assets(not gross fixed assets). As depreciation is a contra asset (those assets that reduce Assets on the balance sheet) and is indirectly charged off from P&L which reduces the retained earnings on the left side (liabilities) and reduces the Fixed assets on thr right side (assets side). Thus, a balance sheet balances.

To get gross assets you need to look at the scehdule of Property, plant and equipment given in the annual report.

Coming to marrying Asset turns with Capacity Utilisation:-

Asset turns increasing leads to an increase in capacity utilization. As it indicates that you’re able to generate more sales using the same assets. Perhaps the most recent example here is:- Laurus Labs in the recent times. Where 60% of gross block was lying idle, basically generating 0 topine. As utilisation picked up, gross block turns improved and we got an explosion in operating leverage and margins. Check the Pat growth in last 2 years.

You can use Asset turns to forecast sales too. Eg:- Navin Fluorine is doing 2 seperate capital expenditures (capex/additon to fixed assets)

First one is in a MPP, where they are investing 195 crores. Expecting asset turns of 1.35 to 1.45x. Thus, to forecast sales simply multiply 195 by 1.35 or 1.45. peak sales of 260-280 crores.

Second one is HPP plant, where they are investing 435 crores. 365 crores for the plant and 70 crores for power generation plant (captive). Contract is worth 2800 crores over 7 years basically back of the envelope 400 crores a year. 435 crores of assets generating 400 crores of sales. Reflects asset turns are 0.9x.

Additionally these two capex will lead to sales growth by 660 crores. Using this data point you can make a rough guesstimate about the future sales of the co.

I hope this helps, in case any doubts. Please post, will reply

Disclosure: invested in Navin, Syngene, Laurus,Indoco & Apl Apollo. Not sebi registered.

27 Likes

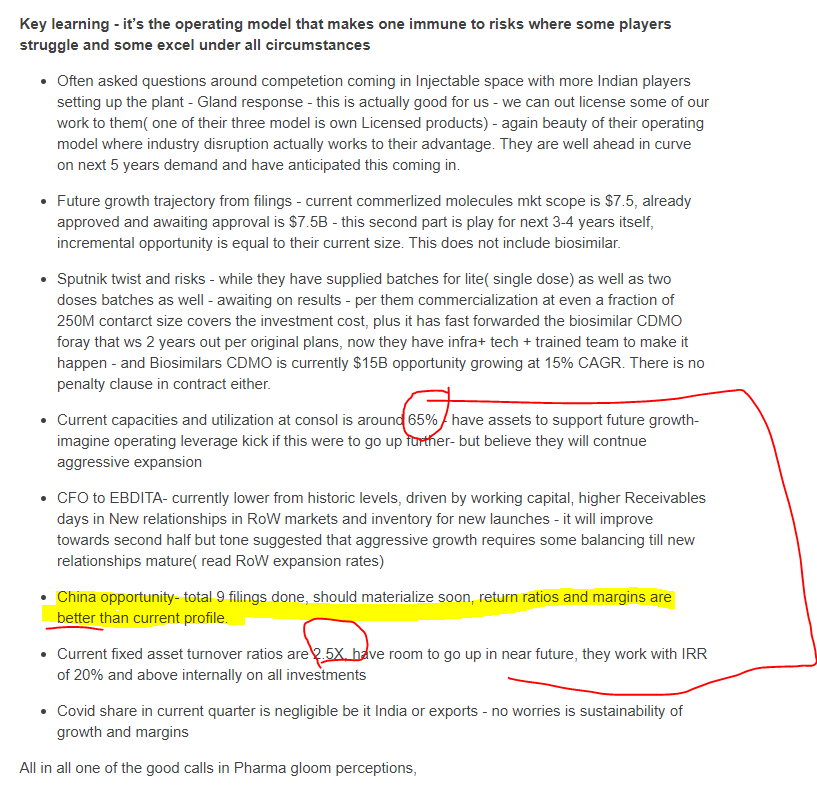

Current Utilisation of 65% implies the same as mentioned above. Given it’s a Cdmo Business, usually chemicals and Cdmo cannot do more than 80-85% Utilisation (you will have to check for gland) due to change over times+2.5x implies. For per rs of fixed asset they deploy they generate 2.5 rs of sales

Disc: not invested. Started tracking

8 Likes

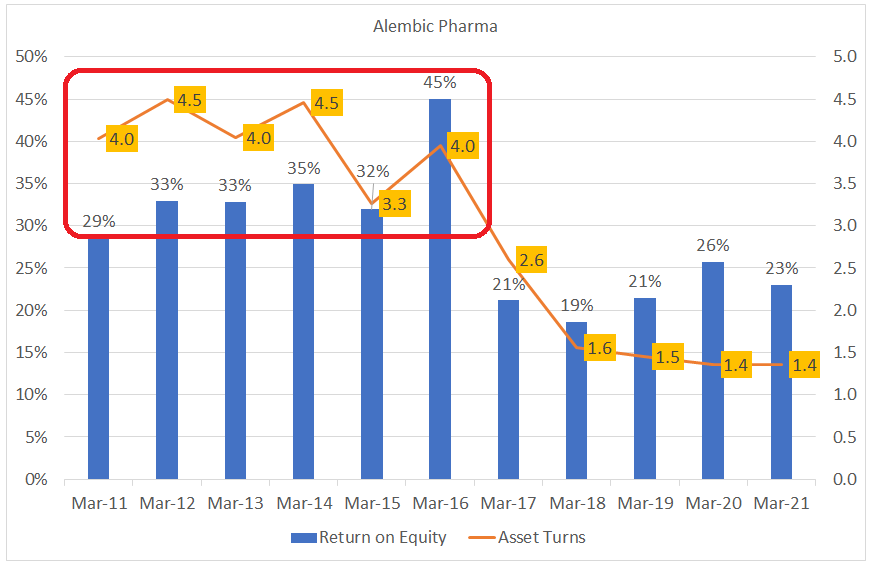

Adding onto what @Worldlywiseinvestors has said, lets take an example of Alembic Pharma.

From 2011 to 2016, every rupee of their net fixed assets was producing 4 rupees of sales, on average, and return on equity was a cool 30% plus.

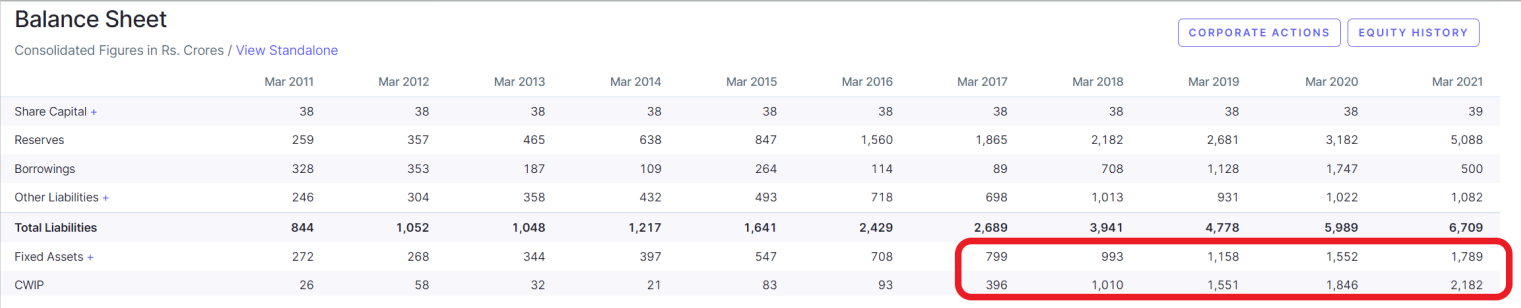

And then something happened on their balance sheet, starting from 2017. Their Fixed Assets + Capital Work in Progress started shooting up.

What this means is that they invested heavily in their capacities but weren’t able to monetize them. It’s like a milker buying a cow and not being able to milk it, leading to a drop in return on equity which Mr. Market does not like, unless the drop is temporary and there is short-medium term visibility about when

the company will be able to pep up it’s ROE, back to pre-capex levels.

This happened partly because the co. was not able to get a regulatory approval for its injectables facility from the US FDA and all the Capex that they did over the years is yet to bear fruit.

As we can see from this example, capacity utilization and asset turns are a critical variable in determining which way the company’s return on equity will swing.

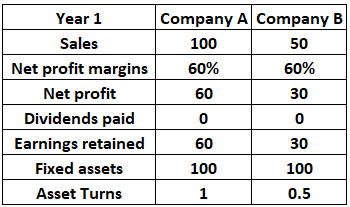

Let’s take another example.

-

Company A produces 100 Crs of sales using 100 Crs of Fixed Assets, with 60% Net Profit margins

-

Whereas Company B can produce only 50 Crs of sales using 100 Crs of fixed assets, with the same 60% Net Profit margins as Company A.

If we suppose both companies have a target of doubling their sales next year, how will both companies fund the Fixed Assets needed to double their sales.

Clearly Company A is in a better position because comparatively it has an asset lighter business model than Company B.

While, Company A will need 40 Crs of external funding via debt, Company B will need 70 Crs of debt, which will put it in a tough spot.

Hope this answers ![]()

Disc: Exited Alembic around 1000 levels earlier this year.

25 Likes

Thanks for making it easier to understand.

1 Like

Can we get a very basic meaning of Return on incremental invested capital…??

Cam some one make a ratio for it on screener.in?

Hello,

When is this likely to get implemented.

Thanks

1 Like

Can we get a basic gist of the meaning of the term "Return on incremental invested capital?

Can some one make a ratio for it on screener.in ??

1 Like

You can keep checking trendlyne or alphastreet youtube channels. They track most companies and upload the recording within 3-4 hrs.

Can somebody try to answer for below query please?

Hi - excerpt from Aavas earnings transcript, could someone please help opine why CPs are not considered a prudent borrowing practice, and possibly also pros and cons of various borrowing mechanisms like subordinated debt, securitisation, etc. -

Despite the higher short-term rating of A1+, we continue

to maintain zero exposure to commercial paper as a prudent borrowing practice.

Thank you so much

1 Like

Can someone pls help understand the valuation of Honda Siel… Despite decreasing Ebidta the stock did not show much negative reaction apart from the initial dip… I know one day stock price movement may mean nothing, but still a little curious and would appreciate any inputs…

I don’t follow Honda Siel, so cannot comment why it did not fall despite posting loss in the quarter. But this is a natural occurrence, sometimes price falls despite good results, sometimes it does not fall despite bad results. When expectations are high and not met, price falls, and when bad result is anticipated and a better result is posted, price goes up.

One cannot simply provide a company-specific reason as to why the price did not fall, without knowing what has happened and what will happen. The management may have already mentioned about the quarter’s sales and profit, may have given some guidance for the next few quarters too. Stock prices fall when there are sudden surprises or great expectations are built up, or simply taken to elevated levels with no fundamentals to support, along with many other reasons. So the market may have already anticipated this kind of result or may have expected an even worse result, which when did not happen, reacted and made the price go high.

Price has moved up, volume is also the highest in a month, so looks like no surprises with the result.

1 Like

Thanks @ChaitanyaC; Agreed, expectation setting is an important task of the management.

And surely as you say, with High Volumes and increase in stock price, its safe to assume that the results had no negative surprises…

With no increase in Sales I am just contemplating if Honda Siel is a good stock to own; specially since at 18+ PE I dont think its cheap… Future maybe decent with limited competition - Is the only positive i can think of…

Median PE is 22, so may be the current PE is not high. Not that it would revert to the median PE, but saying this on a historical basis. But as you have mentioned you have been holding it for years, I presume you did not buy at the CMP years ago, and you are not adding more.

Certain stocks test the resolve of the investors, despite their knowledge and experience both in the market in general and the stocks in discussion. One may have to wait for years to get the expected return, or worse, to get the principal back. Part of the game. So patience is also a virtue here. On one side there will be stories where patience paid handsomely, and on the other side, there will be countless missed opportunities for getting stuck.

I have no idea what Honda Siel does, so cannot comment which side it falls to, and my views are general and random thoughts.

1 Like