Yes. “Share Buyback’s by company” do this magic.

1 Like

I have a small doubt with respect to dividend and ex-dividend date. In order to be eligible for the dividend, the investor needs to have shares in his demat before the ex-dividend date. But because of the settlement period which is T+2 days and for example, if I buy shares on 10th and the ex-dividend date is 12th, will I still be eligible for the dividend?

As far as what I understood, the shares must be there with the investor before ex-dividend date and on the record date, your name should appear in the list of shareholders but I’m not so sure because of the settlement period.

I came across following in GoodYear India Annual Report 2021 (https://www.bseindia.com/bseplus/AnnualReport/500168/69031500168.pdf)

Sections Name : Commitments

I am not sure how to interpret this amount of 32.26 Crore

Does that mean it has been paid as advance already or it is just a commitment ?

If this is an actual amount, which section of Balance sheet should I look upto to see the same. Also , what does it mean when it is mentioned that it is not recognised as liabilities ?

Hi all,

Need help regarding Tata Chemicals… Am confused to hold this stock or not for long term… I bought Tata chemicals over Deepak Nitrite 4 months ago and regret my decision. But due to Lithium ion plant business news of Tata chemicals am holding to it. ROCE and ROE is very bad for Tata chemicals

Am new to equities, please advise if i can hold on to this or exit n buy a better stock

Thanks!

You have to have the shares in your account by the record date and not by the ex-dividend date. The ex-dividend will be prior to the record date due to the T+2 settlement we have and as such the ex-dividend date is shown in stock broker’s platforms, so that we know if we want to buy we should buy by the ex-dividend date.

Although EPS does not equate to value, lets for a minute assume it does, for the purpose of this exercise.

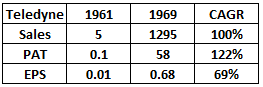

One very famous example, quoted by Warren Buffett is that of Henry Singleton of Teledyne and here’s how Singleton worked his magic and increased shareholder value faster than he grew the company’s business.

From 1961 to 1969, Life was good for Teledyne because it was growing off a small base. Sales, profits and EPS were consistently growing at very high rates every year, due to several mergers/acquisitions. Think of it as the Berkshire Hathaway of that era.

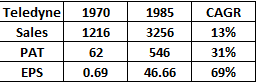

But then it became too big and Teledyne’s business slowed down and Singleton was having trouble growing it at the previous decade’s triple digit growth rates.

And this is where Singleton’s exceptional capital allocation skills were displayed. Although, PAT grew only by 31% (low by Singleton’s previous benchmarks), EPS still grew by a mouth watering 69% per annum. Pure brilliance in capital allocation.

When EPS grows faster than PAT over long periods of time, combined with other things that we would normally consider before investing, chances are that the guy running the show is a genius and we should look into partnering with him.

7 Likes

Many Thanks Barath. Interesting. Just one question

EPS grows faster than PAT, is due to increased ROCE?

If you can through some more lights.

Thanks again.

1 Like

EPS growing faster than PAT = Buy backs

EPS growing slower than PAT = Dilution, unless the dilution is value creating, which is not true in most cases.

In exceptional cases such as Teledyne/Berkshire, EPS growing slower than PAT may be a good thing because the jockey is more focused on long term value creation and rightly not worrying about short term dilution.

This math holds good for most cases and for value creating lenders as well, Gruh Finance, for example.

5 Likes

Hi Bharat, thank you for your help. Investing is really fascinating and that book is very interesting to read. I did not know that capital allocation can have significant impart on value creation.

1 Like

can u please name the book

Dear members - a noob question, I keep hearing that the PAT growth more or less aligns with the EPS growth in the long run. However, for a lot of Coffee Can companies we keep hearing, I see a big disparity and the PAT growth looks fairly abysmal in some of the most celebrated lots. For example -

Pidilite -

Asian Paints - somewhat less stark but still significant -

I’d think this could be attributable to the strength & quality of these companies with ROCEs upwards of 30%, large addressable market, consistent CAPEX. Any insights on if there is always going to be a PAT/ EPS growth disparity with such companies, and how does one value these companies.

Thanks & Regards,

Mohit

1 Like

Hello all,

My relative (former employee and retired long time back) held ITC shares with Karvy. Currently the shares are with Karvy. That is the only information we have currently. He doesn’t even know Demat account ID or whether was it in physical form or Demat too.

Now how to track the number of shares held and transfer it back to a new Demat account? Any help would be really appreciated.

Thanks!!

Not sure if this is the best way, but the list of unpaid and unclaimed dividend is made public on every listed company’s website. That can be a starting point. See if your relative’s name exists. If it does, you know he is still a shareholder in the company’s records. You can then approach the Company Secretary with this information and he should be able to guide you on how to go about claiming your shares. Since your relative is an ex-employee, hopefully company people will be more cooperative than usual and help him claim his due.

1 Like

XIRR can be calculated in excel. Formula is =XIRR(Values, Dates, Guess).

Need help as to How to interpret XIRR - what does it really mean and how to judge vis-a-vis absolute return in portfolio.

e.g. Portfolio absolute return =10% but portfolio XIRR=50%

- Does this mean money is growing at 50% yearly?

- Why are the two return measures so different ( 10% vs 50%) ?

- 10% return looks average while 50% looks outstanding. Cant figure out how to understand / assimilate the two metrices meaningfully.

1 Like

For timeframes less than 1 year, XIRR makes little sense. For timeframes > 1 year, it shows you the annual returns (assuming 100% re-investment), in other terms it gives you the Compounded Annual Growth Rate(CAGR) for your portfolio.

if Rs. 100 becomes 200 in 4 years, Absolute returns = 100%, but CAGR (or XIRR) = 18.9%

2 Likes

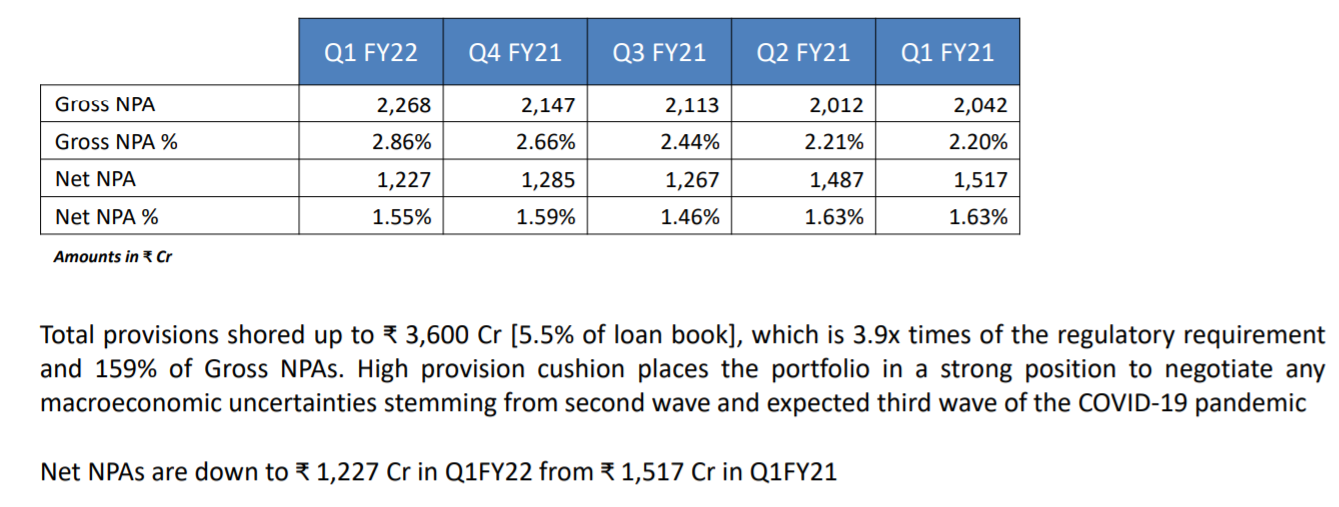

When I am looking into the Q1 FY22 investor presentation of IndiaBulls Housing Finance, GNPA reported as 2.86% of the loan book and total provisions mentioned as 5.5%, but NNPA is 1.55%. So far, I thought NNPA = GNPA - Provisions, But here that’s not how NNPA looks. I see this similar difference in some other firms also. How this calculation works?

Provision is made for known and unknow (predicted) NPAs. The equation (NNPA = GNPA - Provisions) is correct when you know what part of provisions has been made against the known GNPA and what part against the predicted ones.

@Chandragupta thank you for your response.

From the old records, we somehow managed to get the NDSL Demat account details. I think we have a good hold now.

Now few questions

- How do we know currently which bank account and phone number is linked to the DP account?

- If we need to update the same how can we do that?

Thank you!!

Hi, Please approach NSDL directly or the DP (if you know). They should be able to guide you.