In this case, since taxable income is below basic exemption limit of 2.5 Lakhs, the balance 50,000 can be adjusted against short term/long term capital gains. Tax needs to be paid on the remaining STCG/LTCG.

For example, if your STCG is 70,000 and all other incomes are 2L, you can adjust 50,000 against STCG and pay tax of 15% only on 20,000.

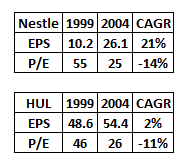

Point is in 1998-99

EPS growth of Nestle 14.7 vs HUL 31.5.

Nestle PE 54.6 vs HUL 47. Roce and ROE both for HUL are much better than nestle.

HUL seems far better than Nestle.

Stock performance:

In 2004 (Five years post above study): Nestle 1.26 x vs HUL 0.74 x

To date: Nestle 47.7 x vs HUL 17.3 x and Nifty 20.6 x (HUL underperformed nifty).

In hindsight with just a number, we may have chosen HUL. Why despite the great numbers Nestle outperformed HUL?

Any insight - probable reasons? Looking for views from the senior members or VP friends who may have studied both HUL and Nestle? Or any old articles etc will help. Thanks.

I don’t think the comparison is not fully correct, as the PF of their products are not the same. Despite being labelled as the same category, if the products are different and unique and if the companies derive sales and profits from these products, the comparison does not give us clear insights.

I don’t know what products they had 22 years go, but now their products are different with the exception of coffee.

HUL although has many products, has competitors too in almost all categories. Nestle on the other hand kind of enjoys monopoly with baby foods, Cerelac has been for ages. Not to mention Maggi until the arrival of Yippee, still Maggie is number one and Yippee number two.

I don’t have the sales contribution and profit contribution of the aforementioned products of Nestle, but when there are products in the market, with no competition and the quality does not deteriorate, and more and more people start buying these products, sales, profits and share price will go up.

Agree to @ChaitanyaC. Seems the recent number says the same / Nestle may be better than HUL - (Don’t have data of historical number).

Some more stuff to think.

Most important: One Mr in 1999 had known that Nestle will outperform HUL and that is Mr Market. Hence M gave a higher valuation to Nestle (PE of Nestle was higher than HUL in 1998).

Current ratios:

Ratios / Nestle vs HUL

Mkt Cap: 1.91 L / 6.58 L (3.44 times)

PE: 86.5 / 79.2

ROCE: 139 / 39

ROE: 106/29

Sales G 3 yrs: 10.1 / 9.78

Sales G 5 yrs: 10.3/7.88

Profit G 3 yrs: 19.3 / 16

Profit G 5 yrs: 18.6/14.4

Divi: 1.01 / 1.11

Sales Ann: 12369/39783

Profit Ann: 1968/6748

Profit Margin: 15.91/16.96

As per current numbers (3/5 yrs) Nestle is ahead of HUL except for profit margin.

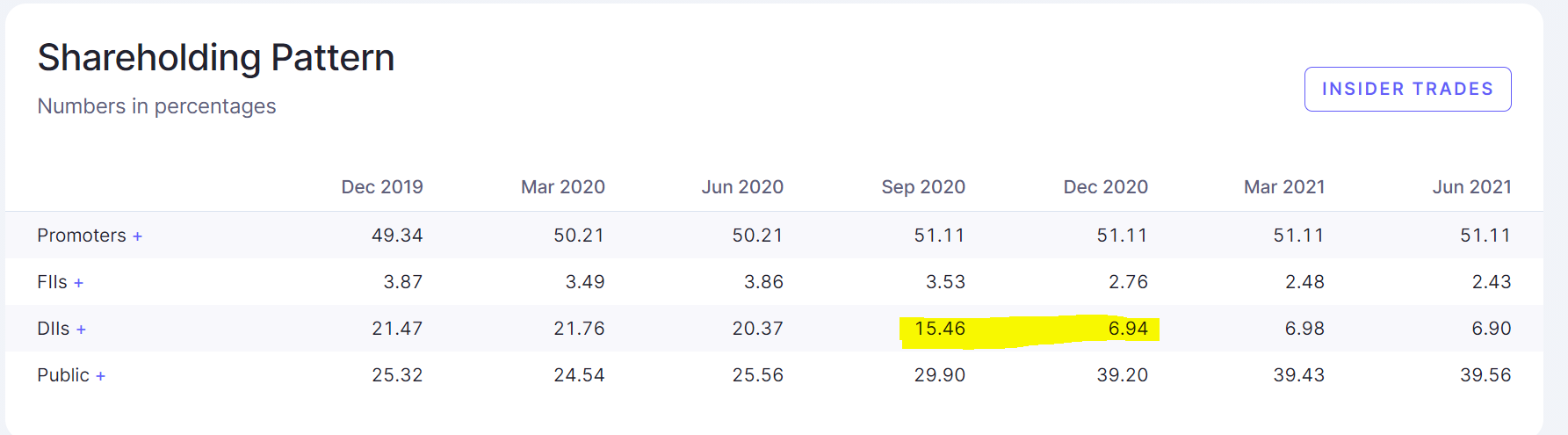

I’m trying to figure out something that I noticed for a company that I was reading (SHIL Ltd) which I find strange.

So the company was having a DII ownership of ~15.5% at the end of Q2-2020 and most of the DII’s exited the stock and at the end of Q3 2020 DII Ownership was ~7%.

So that’s more than 8% of the company’s equity sold.

So I was trying to figure out that isn’t it viewed as negative as DII’s were selling heavy?

On the contrary, I noticed that the share price rose more than 60% despite heavy selling by DII’s. Most of the selling happened in Nov 2020 where the share price went from 75 to120.

One this to keep in mind is that this company was formed in Dec 2019 after the demerger of Consumer, Retail & Building products of HSIL into SHIL. Not sure if it plays any role here?

Don’t know if this is a dumb question… trying to learn.

Not really in this case.

DII’s received the shares due to demerger. Generally, DII’s have internal rules that does not permit microcaps ( demerged company would have been ~ 600 Cr. Mkt Cap, considering 7.23 Cr. as No. Eq. Shares and Mkt price of INR 80) in the portfolio.

I was hoping the same. But is there any reason they (DII’s) waited almost a year to do this ?. i.e. company got delisted in 2019

I’ve known few demergers like Solara (demerged from Strides), Aarti Surfactants (demerged from Aarti industries) these kept hitting lower circuits from the day the demerged entity was listed (You can check from charts) as DII’s were forced to sell as their Investment policy statement or SEBI rules do not let them hold the shares of the demerged company due to its size.

If the same rule applies for SHIL too then why sell after a year?. I am not aware of many SEBI rules that are in place, can someone help me understand this!!

Let me try to answer why HUL under-performed Nestle by a wide margin between 1999 & 2004.

Both HUL and Nestle seemed to have been market darlings in 1999, based on the high PE multiples assigned to both cos at the time.

HUL’s share price had gone from ₹49 in 1988 to ₹2250 in 1999, compounding shareholders returns at a superb 42%. I don’t think similar share price data is available for Nestle.

And what happened post 1999 is that HUL went from being a fast grower to a stalwart (not even a stalwart since it didn’t even grow at prevailing interest rates at the time) and people who bought at any price (BAAP investing as it is called today ) were left holding the can, at least temporarily. I can imagine why some of them might have even lost patience and exited at sub-optimal returns too.

Meanwhile Nestle compounded its EPS at 21% CAGR, beating HUL & a majority of other listed cos of the era, hands down.

The lesson for me is buy & hold (referring to HUL in this context) is fine as long as it doesn’t turn into buy & forget. The difference between both approaches is night & day.

Buy & hold some times involves opportunity costs (think what would have happened if one had owned Hero Honda or an HDFC Bank, both of which were doing much better, instead of HUL at the time) and one should not go for the buy & hold approach unless one is okay to under-perform the market for several years in a row and yet not lose sleep over it.

Also, it is okay to switch horses when the one that you’ve bet on has slowed down for whatever reasons.

Thanks, @barathmukhi for taking the time to educate us. Appreciate it.

Got the answer.

Dil mange more…

Wondering if you have or are able to find the market cap of both in 1999?

Also EPS and P/E from 2004 to date (Similar to what you indicated from 1999 to 2004).

Hi, I have a question related with tax filing. I don’t know which thread I should ask. Hence I am asking this question here.

I have some small cases which rebalance every week or 1-2 times in a month. It result in lot of transactions in the financial year. So I want to ask from the people who are doing trading or having small cases, how do you file your taxes with these many transactions(potentially resulting into short term capital gain) as we have to report all the scripts sold within the financial year. Is there any easy or automated way of doing it?

I am using Zerodha. I know we can get P&L statement from Zerodha. But if it has lot of transactions, we will have to make a entry for each transaction in the ITR. So I was wondering if there is automated way to make these entries in ITR.

I also find many difficulties on this. ITR needs date of sale, date of purchase, qty, etc. how can you fill consolidated on these informations. Also most of the times one scrip is sold many times or purchased in different FYs. Each scrip needs multiple entries in ITR

I have zerodha and ICICI direct as brokers. Why can’t their P&L report be in sync with columns of ITR. Each one has its own report columns, with unique difficulties to feed.

Please guide if any simple way to file consolidated.

Have you used online ITR2 facility …The ONLINE ITR site is very friendly to use … Pl try it

Only in case of share bought pre Jan 2018 you are expected to do stockwise entry . This data can be prepared easily as ICICI direct gives all this details stock wise , date wise along with FMV , purchase and sales expenses along with cap gains computation

You need to organise this data under following columns by doing PIVOT on ICICI direct data

“What counts in the long run is the increase in per share value, not overall growth or size”. Can anyone shed some lights on this statement? Can a company produce a value without increasing its size and growth. Do we have any example companies which is applicable for this statement ?

Does it mean, your investment becomes multibagger even though no increase in market cap?

It is easier to enter details this time if grandfathering provisions are not applicable. only one consolidated entry is possible for STCG. Purchase date can be mentioned as 01-04 and sale date can be mentioned as 31-03.

For LTCG, it is better to upload an excel file with proper dates and buy sell values

What is important is the values entered of STCG and LTCG should be correct.