@ChiragD Margin of safety does not come from diversification. It comes from a positive expected value. But comes from big winners.

For more insights into this concept go through Prof. Bakshi’s video @ https://www.youtube.com/watch?v=pfsbVlrV2y0

@ChiragD Margin of safety does not come from diversification. It comes from a positive expected value. But comes from big winners.

For more insights into this concept go through Prof. Bakshi’s video @ https://www.youtube.com/watch?v=pfsbVlrV2y0

Hi Donald,

I have been trying to change my valuepickr user name. But not sure how to go about it. Unable to see it in FAQs too. I can change my name by going to my account, but user name seems default ?

My sincere apologies if I am asking the wrong person / at the wrong post. But wasnt sure how to go about it. Hence checking

Hi @kartik_bhat

I don’t think u can change ur user name, u can change ur name though. I checked under all preferences.

Hi,

Can someone assist with free websites providing skewness and kurtosis data for individual stocks/scripts?

Thanks in advance.

Recently I have been thinking about large caps. Can they become multibagger? How large can a company be in terms of market cap?

Please share your thoughts or recommend me some material which could shed some light on it.

Always doesn’t mean never. And in between always and never there is a gap. And we should think deeply about that gap.

Look at the revenue growth of companies like Avanti, Page, Relaxo, Bajaj, etc and you’ll see why revenue growth matters. A lot ![]()

All things being equal, it is much easier for a smaller co. to grow than a larger co. But that doesn’t mean larger co’s can’t become multibaggers. If the valuation is low enough, then yes large caps can become multibaggers. But the problem is when a large cap is at a low valuation, you may find it difficult to gather the courage to buy it.

Here’s one from Howard Marks - When the Time Comes to Buy, You Won’t Want To. The best time to buy generally comes when nobody else will; other people’s unwillingness to buy tends to make securities cheap. But the factors that render others averse to buying will affect you, too. The contrarian may push through those feelings and buy anyway, even though it’s not easy.

But as an investor, there are better chances to find big winners in small & mid caps because

From an auditor’s standpoint, smaller co’s are easier to audit compared to larger co’s

There’s usually lesser bureaucracy in smaller co’s vs larger co’s and decisions are made instantly by the top guys running the show. Which in turn means, better efficiency top-down.

Lack of liquidity in small caps turns off some off the big boys, which mean there’s a wider gap between price and the actual value.

Smaller co’s have a larger chance of getting taken over.

And here’s one from Ralph Wanger - Chances are, things have changed enough so that whatever made you a success 30 years ago doesn’t work anymore. By concentrating on smaller companies, you improve your chances of catching the next wave.

And this is from one of the wealth creation studies - “So, one thing is certain. If you want multi-baggers, you are unlikely to find them among the ranks of larger companies. You will have to

rummage the small-cap and micro-cap space.”

Thank you so much! Was looking for this type of detailed answer.

Could also recommend me any books to under micro caps companies? If any.

No books but, old annual reports of companies like Ajanta Pharma, Avanti Feeds, Pantaloons, Titan, etc are the best case studies I have found on the net.

Also, you can consider reading all the starting few posts for the below companies to see how things play out over time.

These posts are classics in their own right.

Hello Value Pickers,

I am a newbie investor and new to the forum as well. Thanks for all the great content.

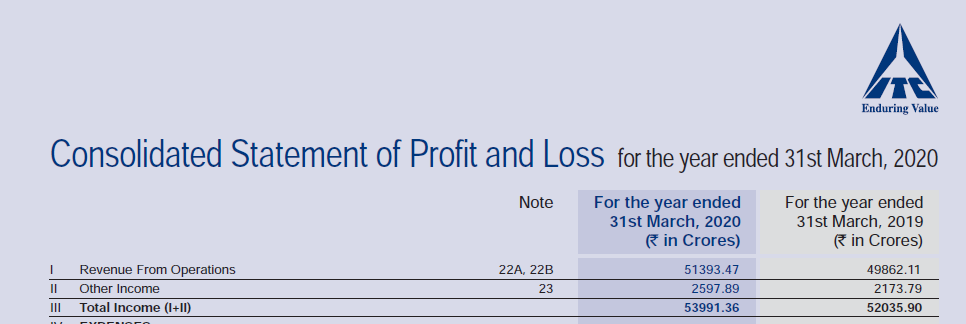

I am in my learning phase and trying to do fundamental analysis of some stocks. I am looking at the company annual reports of ITC and trying to do some basic ratios etc. But I found some discrepancies between the annual report data and data available in Screener.in or tickertape.in. I tried my best to find the reason for the discrepancies and losing sleep over that. Thought of checking with you guys. Below are the data from P&L statement where I am finding mismatch.

From the Consolidated Statement of P&L , the revenue from operations are 51393.47 crores and other income 2597.89. Total is coming to be 53991.36. But screener.in shows a different number, 49388 crores

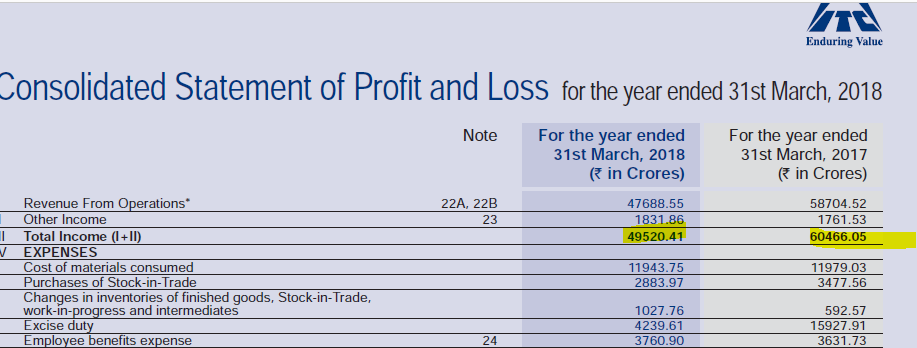

This consistently different for ITC(Other companies it seems to be in alignment with annual report). As per the AR, the revenue in 2017 is 60466 crores and 2018 is 49520. Which is a decline of about 18%. But every website reported a different number(A positive growth).

The revenue numbers are 42768 and 43449 crores in screener website(Other websites are also having similar values)

I might be missing some basics. But I am kind of lost. Appreciate your help.

Excluding other income sales was 47688 Crs. And Excise duty was 4239 Crs. 47688 - 4239 = 43449 Crs, which is the number that is showing up on Screener.

The logic seems to be that ITC is collecting Excise duty from it’s customers on behalf of the Excise Dept.

You will need to check if this is true for other years as well.

Another thing. A lot of companies restate their numbers every year after the annual report is released due to order cancellations, inventory revaluation, etc.

Sir many of the pharma companies say divis lab,alembic laurus etc have negative 10 years free cash flow.what to be think in this.and in 10years free cash flows are negative in every year and reserves are increasing why it is so.

Wrt fast growing companies like Alembic, laurus, divis, etc. we should not be worried about FCF at all.

For example, Pantaloons was a co. whose stock price went up by more than 100x between 2003 & 2008, before tanking. It was diluting equity, high on debt and growing rather recklessly, resulting in a lack of FCF.

In the same era, Trent Westside was producing FCF but not growing and the stock came nowhere near to Pantaloons in terms of the returns it had provided. So a lack of FCF in the case of Alembic shouldn’t be a worry.

There’s always one thing or another to worry about.

This is a summary of concerns investors had based on the 900+ posts on the Ajanta Pharma thread.

The emotional roller coaster that investors were experiencing was nothing short of a suspense thriller

• Will they be successful in the US market?

• Pricing Power risk

• Approvals won’t translate in sales & profits for Ajanta. For eg. Shilpa had approvals but hadn’t been able to monetize those approvals for 2 years

• Aggressive Capex & R&D putting pressure on near term margins

• Higher working capital requirements (North of 25% of sales)

• Forex risk due to a USD/INR fluctuation

o Re-rating is over at 11 PE. 15 PE is high (and might have been a reasonable assumption back then)

o Income Tax raid due to R&D exp that fell in a grey area

o Operator manipulation

• Unichem was a comparable opportunity to Ajanta, but went nowhere

• Promoters pledging shares

• Delivery volumes less than 20%

• Stock is too volatile… Too many 20% plus drops. A 40% correction… Would have been difficult to hold

• Already missed the bus. It has already gone up so much. How much more can it possibly go? This was in Oct 2013, much before it went up even more.

• Will the high margins sustain?

• Promoter integrity issues - First generation promoters of Ajanta had a lot of question marks about their integrity and corporate governance.

• Numbers are so good. Could they be fake?

• Growth slowed down. Is the slow down temporary or permanent? Will previous high growth rates ever come back? May 2017

• Return ratios dropping

• Promoters reduced stake

• Not all ANDA approvals are commercialized. For Ajanta Pharma, only 30-40% of approvals turned out to be economically viable

• Africa business took a hit because WHO stopped bidding. NGOs stopped funding WHO and WHO stopped buying medicines for Africa from Ajanta Pharma

o Reduction in African tender business due to 15-20% price erosion and stoppage of procurement from some countries

o US business fell by 63% due to consolidation of buyers

• Margins dropped from 36% to 26%, due to stagnant sales and increasing expenses

• Marketing unapproved drugs manufactured by another company

The above analysis of Ajanta’s (which was a 60 bagger between 2010 & 2017) thread helped me realize, well that’s life for a Pharma investor.

Disc: invested in alembic & laurus

Thank you so much sir to clarify me in details

Hi all,

I wish to know if my method to calculate free cashflow is correct because I believe the way cashflow statement calculates it: net cashflow from operating activity less capital expenditure, may or may not show actual facts.

If we calculate it this way, even loss making companies can have a positive cashflow as net cashflow from operating activity is positive as they are supported by high cash credit from creditors.

So how I calculate this for any company is:

From Income statement : Profit before interest and taxation

Add: from income statement : depreciation/amortization/other written off intangibles

Less: from Income statement : Interest paid

Less: from cashflow statement: Tax paid

Less: from cashflow statement: capital expenditure

Answer: free cashflow

I have also marked from where I am taking the numbers.

Then I divide each year free cashflow by previous year equity base, to see how profitable a company is, >18% is a good sign as per my understanding.

Please criticize/support this approach and correct me if am totally wrong.

Even if a company is supported by cash credit, it pays out interest expenses right. This is accounted for in the Net Income. So CFO would start from Net Income and adjust for Non cash related items like changes in receivables, inventories, depreciation etc. Here the interest income is ignored as it accounted for in the income statement. Does that make sense?

Hi everyone,

I wanted to understand the price of a commodity like Maize in the indian market. For this i was looking to see maize prices on NCDEX for last 10 years. Would anyone happen to know how i can do that? I went to the website:

but i could not find the price, only a blank chart.

Sorry @eyesice, if I steered you into wrong direction, but here I am not talking of companies like banks/nbfcs which depend heavily on their interest come. I am trying to look at companies like ITC, reliance, eicher motors, etc which, ideally , should not depend upon interest income. Another reason for excluding interest income is I want to focus what company is earning from core business.

No I was talking about interest expense that the company generally pays for its debt obligations. Net Income accounts for Depreciation, Interest, Tax Paid. Now in CFO - non cash expenses like depreciation, receivables, inventories are added back. Note that interest expense and tax paid are not added back. This gives a true sense of how much cash goes in and out of its day to day operations. Now if you subtract Capex, this would give you the remaining cash that was basically not required to run the business during that year.

In your calculations, I think the difference is that you are not accounting for non cash items like change in receivables and inventories.

Yeah, I am not focusing on trade receivable, trade payables. Debtor turnover ratios and creditor turnover ratios are enough for me to guage how fast the company gets/pays cash from/to debtors/creditors.

My only fear with the way cfo is shown is that I have seen many loss making companies having positive cashflows and even having free cashflows. That’s I had to resort to this way. What do you guys say ??

Accept or refuse ?