Many thanks for that .I will try to explore it.

Can some one tell how companies gives warrants to non promoters.and how after converting warrants into share non promoters can sell their shares

Hello

Please help

Please share the sources of online videos for basic understanding of stock market

If someone has any link of such videos please share

Thanks

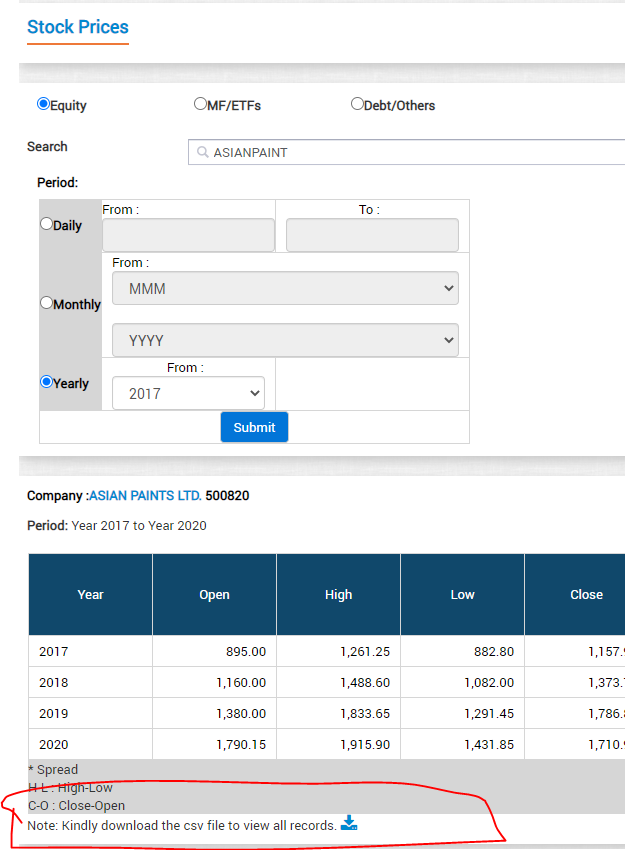

@Manojlion For specific stocks you may use this link to download daily, monthly or yearly stock prices. Stock Prices

Doing this for 500 different companies may be a tedious task though.

1 Like

@Yumnam_Chandrakumar There are no straight answers to this question.

For one, we can look at ROCE / ROE for a company, compared to the given company’s peers in the same industry.

For example, a textile business delivering a consistent a 20% + ROE can be a starting point to investigate whether the company has a moat or not.

Another way to quantify would be to look at margins of the company during tough times / down cycles in the industry. If the management was able to deliver high margins even during tough times, the next level of analysis would be to figure out as to what were the factors that helped the company sustain those margins when everybody else in the industry was bleeding.

We could also compare margins & ROEs of the company vs it’s peers, over several years to figure out whether the company really has some kind of an advantage against it’s competitors.

1 Like

@StonePitbull Uttar Pradesh State Mineral Development Corporation was one company that was wound up via the National Company Law Tribunal.

There are also ongoing proceedings against West Bengal Mineral Development & Trading Corporation (WBMDTC), a government of West Bengal undertaking.

3 Likes

Can anyone guide with the following…

If one buys A company shares which has holding of say 25% in B company. If the A company shares are discounted price does it mean he is getting a good deal. Is it a direct financial translation… ?..

E.g alembic ltd holds 29% of alembic pharma. @77 v/s 977

Please check the below thread on the forum

Hello guys,

I am relatively novice in the world of investing and stil trying to come upto the speed on various aspects like understianding intrinsic details of Balance Sheet, P&L etc. as well as the business operations aspeccts. So pls. bear with me of my question below looks stupid.

Regarding the P&L statement of a business, my head is still trying to come aound the fact that the Depreciatin is taken as an expense. I am not able to understand why is this so? As I know depreciation is the reduction in ‘Book Value’ of an Asset / CAPEX done. So its not an actual expense during that period / FY. As such the cost of the CAPEX / setting up teh Asset is already catered for in the initial funding of the Aseet via debt or internal accruals. So why is it listed as an expense in P&L?

Think of it this way…a person buys a car for 100000 to run it as a taxi. The life of the taxi is 5 yrs. It means that the value of taxi will reduce by 20000 after each year. At the end of first year, 1 lac will get reflected in cash flow statement and the balance sheet. Now, lets say he earned 50000 as revenue. His fuel, maintenance of car and driver salary expenses came to 25000. This will be deducted from the revenue in P&L. Now the 20000( depreciation of the taxi) will also get deducted from the revenue as this was the value of taxi spent/foregone to generate this revenue. Once this is deducted, he will be left with 5000 as profit. We need to remember that this is the accounting profit. The cash flow will be higher as depreciation amount is still left as cash with the owner. This will continue for 4 more years till asset is fully depreciated.

3 Likes

Hi can someone help me clarify how to understand the difference between ROCE and ROE. My understanding is that if ROCE>ROE this means that interest rate paid by company for debts is higher than the overall return company earns on its total capital.

If this is correct I cannot understand the below figures for Dixon Technologies

- ROCE: 27.23 %

- ROE: 18.19 %

Does this means that company’s borrowing cost is even higher than 27% ?

On the surface, it certainly seems that way, doesn’t it? But don’t read too strongly into this. The best way to think of this is - once the debt is paid off, the RoE should rise to more or less become equal to the RoCE (because that is the return the business inherently generates).

There could be many reasons that the RoCE is greater than RoE even if the business inherently generates returns more than cost of debt. A common reason could be that the business may have taken a loan to invest in something that may mature only later, but the interest starts getting due. So on paper, it looks like the new investments are returning lower than cost of debt, but that is only because they are not mature. E.g. new stores that may mature only 2-3 yrs down the line. Or a new plant where the moratorium period ends and interest starts getting due, but the plant has some time to go before capacity utilization reaches mature state.

Returns in RoCE is calculated before tax whereas in RoE if calculated after tax.

1 Like

Thanks, makes sense now

Can the long gestation investment be removed from ROCE calculation. I thought ROCE considers all the capital employed by business. Irrespective of when and if that capital will generate any return.

First off, if you are calculating RoCE before tax, then @Nagendran_Krishnamoo’s explanation is the best one.

If you are looking at both post or pre-tax and still find a difference, then the nuance I mentioned could be one cause.

Here is an example. A company invests INR 10 lac to open a new retail outlet. He puts in 5 lac himself (equity) and balance 5 lac is a loan (debt).

Typically retail outlets take some time to mature and become popular. Say, footfalls in year 1 are 2,000; then 5,000 lac in year 2 when the store matures. Accordingly, the profit generated by that store goes up in year 2. Say return on capital (a simplified RoCE) was 7.5% in year 1, and 15% in the mature year 2. This 15% is the stable-state RoCE i.e. the long-term return the store generates.

Here is how the math will work for year 1:

RoCE = 7.5% = 7.5% x 10 lac = INR 75,000

On this return, interest of 10% on the 5 lac loan has to be paid = INR 50,000.

So the equity holder gets INR 25,000 (i.e. 75,000 - 50,0000) against the INR 5 lac he put up.

So RoE = 25,000/500,000 = 5%

Thus RoCE of 7.5% is higher than RoE = 5%. But this is only because the asset is not mature. In the next year, when the store matures and RoCE becomes 15%, then the story reverses.

Note that this ignores taxes. This is the “business” explanation after taking tax out of the game.

So the thing to look for when RoCE > RoE is if the company has made such investments. And does the RoE rise slowly over time as such assets mature…

2 Likes

Help!!! Our dear Mr Buffett has famously said to avoid the trap of EBITDA. And we know how he always said that the depreciation should be treated as an expense. They why does in the owners earnings that he calculates, he adds back depreciation and other non cash expense to the reported earnings? Shouldn’t he subtract them all together to form a more coherent picture? While I know that in accounting you do add it back while calculating cashflows but am still trying to figure this out. I am also not an accountant so any help will be appreciated. Any insights? @ayushmit sir @Donald sir @hitesh2710 sir.

RoE is (Net income / Equity) or (EPS / Book Value)

RoCE is (Earning before interest and tax / Total Asset)

If the company is highly leveraged, and RoCE is greater than the cost of borrowing then RoE will be greater than RoCE. And if it isn’t leveraged (that is, not a lot of debt in balance sheet), the RoE will be less than RoCE.

It is a good sign when RoE is less than RoCE.

6 Likes

My understanding of the Owner’s earnings -

In Buffet’s calculation the depreciation and other non-cash expense is taken in negative form so addition means subtraction in principle.

Owner earning = EBITDA - Depreciation & Amortization - Non-cash expense - Maintenance CAPEX

Remeber, not to consider the expansion CAPEX but only the CAPEX required to maintain the competitivenss of current business.

The basic insight is Capex required for maintenance of competitiveness of current business should not be included in earning while calculating intrinsic value. In some business, calculating intrinsic value by using only the net income can result in overstimation of its actual value.

1 Like

I have a very basic query on diversification.

If I go by investing principles of someone like Ben Graham and keep my portfolio concentrated to 10 stocks, how should I diversify these across sectors?

My naive idea is to choose one across 10 different sectors. With ofcourse 5-15% between each company/sector. Is this too much diversification? I know it depends on the amount of time I am willing to spend tracking or following my companies closely, are there any other factors to consider while diversifying across sectors?

Sorry for such a noob question, but it has me startled