Trade receivables as a trend should not be ignored. Receivables in tandem with revenue growth can be accepted. Yes when there is profit and which is used in capex or r&d should be accounted in free cash flow.

1 Like

Dear all,

Very recently since Covid lockdown, I have started education myself about the Indian equity markets. So far in my education journey I have read blogs, VP posts, watched youtube videos, participated in 1 VP Europe call (thanks to @rajanprabu and @harsh.beria93), finished reading rich dad poor dad, intelligent investor (wasn’t easy! ![]() ) and started one up on wall street (feels much better).

) and started one up on wall street (feels much better).

Thanks to the above encouragement from @Donald here goes with my most basic questions:

-

What is the single most important aspect for a company/share to proceed in value (in the eyes of the equity markets)? Free cash flow? Earnings? Net profit? Revenues?

My understanding so far from all videos and reading has been free cash flow. -

P/E ratio, is it really the very basic first thing to be seen for investors (I found tonnes of videos about it)? I personally got lost quite often in the industry PE, peer PE comparisons (still being new at this). Is there something else as a KPI to start with?

-

No matter how well a company does, what if no DIIs or FIIs or MFs notices and/or invests in them? Their value essentially won’t increase right?

-

How influential are the FIIs, DIIs and MFs in the Indian equity markets? Can a retail investor or in general retail investment section influence stock price (assuming available direct capital is much lesser as compared to xIIs)?

I understand these questions are extremely basic; I would nevertheless appreciate your valuable inputs.

Thank you,

Sameer

PS: Collaborators, this is my first post on VP. Kindly excuse me if wrongly posted. Please advise and will move it elsewhere.

1 Like

@sam11owen FCF is not a one size fits all kind of an answer.

FCF is important in companies which don’t have the room to grow. Eg: Colgate, HUL, etc.

But in a high growth high ROCE co, a lack of FCF can be beneficial, because it means, the co. can compound all retained earnings in the business at high rates of return.

In general a sub 15-20 PE is an ideal starting investment point, assuming all other quality parameters have been checked.

There are exceptions to this 20 PE rule, because a fast grower can still be a bargain at 30-40 PE. Eg: Page Industries in 2011, 2012, when it’s PE was between 30 & 40 was still significantly undervalued. Even if one had bought at perceived “high PEs” back then, they would still have a subsequent 7-8 bagger.

There are many such examples.

Apart from PE, one needs to look at growth & ROCE, besides other forensic accounting parameters

It is better to buy into stocks before FIIs enter, than after. So if you can identify a stock before FIIs enter, then the money post re-rating is all your’s. One of the market cliches being “Go where the puck is going, not where it is.”

3 Likes

Thank you @barathmukhi for your detailed responses. As mentioned, slowly growing into more areas. Will build a better pictures with more such ideas (ex. FCF vs ROCE relation and growth vs PE expectations)

The point you mentioned about entering before FIIs, would it be fair to interpret what you are saying, that for such a case, one needs to primarily research/look at micro and small caps (which are still the so called “hidden gems”)

From my understanding so far, most if not all mid and large cap companies have good FII investments.

Correct. Micro cap, small cap and a lot of mid caps have little or no FII interest. Now there are some small cap and mid cap mutual fund schemes with lower AUMs that still specialize in these areas but they are few and far in between.

1 Like

I use a slightly modified version of P/E, which I call Future P/E.

Generally, a high P/E means that the market believes the company will have a high growth rate.

Price has 2 parts embedded in it - 1 part which values the current book value of the share and the other part which values the growth the company can have. So, I remove the book value part from the price to get a better understanding of what sort of growth has the market factored in for the stock.

P/E = CMP/EPS

Future P/E = (CMP - Book Value)/EPS

1 Like

@starpointer97 thank you for your input. I will need to do some more reading on this to appreciate better.

Hello All,

I have been using my free time to learn about investment since last one year. Watched more youtube videos and everybody talks about good capital allocation is the key for business to succeed.

Is there any way to find out that how good/bad a company is using its capital? Can we find out about capital allocation from annual report? or is it just to understand from a business perspective?

Regards,

Mani

@Mani_Starter One of the easiest ways to figure out whether or not a management is allocating capital well is to compare the ROE delivered by a company vs it’s peers from Screener.in

If a company has high ROE compared to it’s peers it generally means capital allocation is good.

Just like every other market rule, this rule might have exceptions, but works in most cases.

4 Likes

Can some assist with treatment of Right-of-use assets line item in financial statements?

Just wanted to understand the legitimacy of considering the line item as an asset on balance sheet instead an expense on P&L? Is it because the payment is done in advance?

Regards,

Hi,

Please visit this post and the attached external link to understand about the changes w.r.t IND AS accounding standards - Impact of Indian Accounting Standard Ind AS 116 Lease Accounting on indian industries

Thanks. This is helpful.

1 Like

I do have one very basic question I feel I should ask and that is -

Is value investing still possibe ?

Or is it now an outdated concept in today’s world with so much information available so easily ?

@AVB What is your definition of value investing? Is it something like deep value which Ben Graham used to do and some people still do, wherein you pick up a cigar butt stock which still has a few puffs left?

Other forms of value investing include cash bargains, special situation investing, dividend growth investing (think ITC in the correct context) etc. which require an altogether different type of an investing mindset.

Yet another form of investing is buying growth at reasonable price aka GARP. (Peter Lynch kind of investing)

Going by data for Indian stocks for last 2-3 decades, and several multibagger stocks within VP like Kaveri, Ajanta, Astral, Avanti, Mayur, Balkrishna, Shilpa, etc. GARP works best in the Indian context.

It is not a one size fits all kind of an answer and depends on what works for each individual’s own investing psyche. Value works for some people who fret at the thought of paying very high PEs while GARP works for some people who are a bit more price elastic. So besides the examples I have quoted above, figuring out what works for oneself partly answers whether value investing works or not

3 Likes

Hi Everyone,

Wanted to check what tool people are using to check their portfolio’s performance against indices like Nifty, Nifty next etc. Since we purchase at different points of time and at different prices, it is a bit difficut to track portfolio performance. I saw on some boards people were able to draw out graphs of their portfolio performance against the indices. Is there an excel available somewhere for the same.

Any help would be appreciated. Thanks

1 Like

My personal approach is to track the performance of my portfolio just the way Mutual Funds track theirs… I am following the steps given in this blog post

Measuring individual portfolio performance against the benchmark indices

One modification I made to the above - tracking an index like Nifty will not include the dividends… you will need to track against Nifty TRI. Instead, I track against a nifty ETF since ETFs include the dividends…

Currently, my portfolio is purely midcap and so I am checking my NAV against the NAV of M100 (MOSt Shares Midcap 100)

Hello,

Is there a site where I can see this years’s agm proceedings of companies.

Thanks

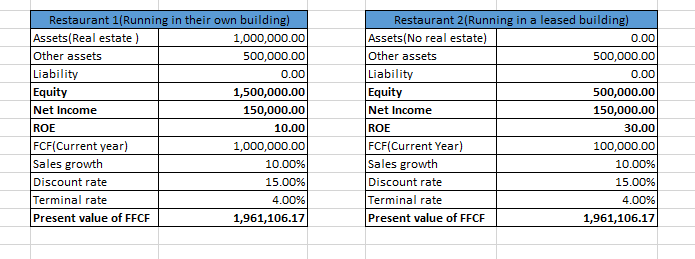

A really stupid question. Why are we not adding share holder’s equity while doing a DCF. Shouldn’t the value of the investment be future earnings discounted to present + current equity projected to the future. For example I have done DCF for Infosys using a discount rate of 15% and its coming out to be around 170,000 Crores(using 5 years projection+ terminal value using 4% perpetual growth).If I calculate 10 years projected cash flow discounted(Not using the terminal value), its coming around 120,000 crores. Current share holders equity is around 65,000 crores. So basically I am valuating a company with 120K Crores projected cash flow for 10 years and around 65000 in cash reserves/equity to 170,000 Crores. Isn’t too conservative. If I am really planning to buy out a business in real life using this method would anyone accept this offer?

1 Like

Current equity has value only to the extent it produces future cash flow. So once you are discounting all the future cash flow, you need not separately add up current equity. Otherwise, it amounts to double counting.

2 Likes

Thanks Chandra.

Lets say I am planning to buy a restaurant and valuating 2 restaurants with similar cash flows. Restaurant 1 is having their own building and restaurant 2 is working in a leased building. Both have zero liabilities. If we value them using DCF both are having same DCF value. But in real life should the one with more equity(in this case real estate asset) demand more price ? Should we use a higher discount rate for the one with less equity in that case ?