“Buffett is essentially talking about return on invested capital. If a company invests $100 in something at the cost of capital of 10%, which in turn earns $7 in earnings forever, it would have a market value of only $70 ($7/10%), failing the $1 test. Earnings of $11 or more would pass the test. When companies make the decision to invest in M&A, CapEx or buybacks, they must make a conscious effort in evaluating if the potential returns would be meaningful and not capital destructive.”

Cost of Capital (CoC) is a theoretical concept. Arithmetically, CoC is the weighted average of the cost of debt and cost of equity. Cost of debt is straightforward – it is the interest a company pays on its loans. Cost of equity is much more nuanced.

In theory, cost of equity should be the return demanded by equity shareholders to provide capital to the company. But what is this return - where to find it or how to calculate?

The simple answer to this is – you can’t. Equity shareholders provided funds to the company when the company was formed – that might be many years or even decades ago. They would also have provided funds intermittently thereafter – if there was a Rights Issue, QIP or other such events. Equity shareholders also provide funds to the company every year through Retained Earnings, assuming the company is profit-making and does not pay out all its profits as dividend. In all such cases, equity shareholders have expectations of getting a minimum something in return. That is the cost of equity, but no one really knows what it is.

Cost of capital is also defined as the opportunity cost of money – what the capital provider can earn by investing the same money elsewhere, since that is the benchmark he will use before investing in this company. But once again, it is not possible to put a precise number to it.

In all this, you will notice that expectations of investors like you and me who buy and sell in the secondary market do not come into picture at all. Their investments do not directly impact the company in any way. Therefore I started by saying that Cost of Capital is a theoretical concept. IMHO, it has no direct relevance to us in our investing. One only needs to understand it conceptually. And for tangible calculations, better to focus on RoE and RoIC since Equity (Net Worth) and Invested Capital are available with precision.

I tried to search whether Saurabh Mukherjea has explained how he calculates Cost of Equity (I have not read his book) and came across this article. Here, he simply adds up the risk free rate of 8 % and a “risk premium” of 6.5 -7% to get a cost of capital of 15 %. Read the article – it explains his thinking quite clearly.

Under law, a listed entity is run by its Board of Directors & Management( needless to say that promoters have command over the board in this way or the other in most of the cases). However if the company has no identifiable promotoer, the board, shareholders and the articles of association would be the guiding factors.The SEBI regulation has mandated a minimum 25 percent of public shareholding but there is no legal requirement of minimum promoter holding.

Agree with @VijayShetty , there are instances of companies with no promoter holding yet very well managed professionaly. Thereby resulting in great returns in long term for retail investors like us. Few noteworthy examples are ITC, L&T, HDFC, ICICI Bank etc.

There is a independent director on the board whose main duty is to protect the minority shareholders like us. But most promoter held companies appoint someone complaint to this post who will go along with whatever they want.

Yes , indeed . Also many times these independent directors turn out to be mute spectators for prolonged visible wrongdoings in the company much to the comfort of promoters only (for their vested interests) . The dominance prevails by means unholy nexus wherein independent directors chose not to red-flag so many issues related any ongoing malaise. No wonder we have many former senior bureaucrats jumping on the boards of the companies with deep pocketed remunerations right after their retirement , justifying the concern raised by @VijayShetty.

Is it right time invest in Metal or Mining stocks now as there is US Trade deal with China on table, and it will confirm soon? If yes which is the Company can invest which gives safety, and also benefit of Commodities cycle. Thanks.

US trade deal with China can have short term impact on the industry parameters. And honestly speaking these geopolitical turmoils are not in our hands neither we can gauge their uncertainty . As a retail investor we should first think of long term investment horizon (wherein short term geopolitical hiccups could also be taken care of) given the cyclical nature of Metals & Mining businesses. Also one should be able to pay some attention towards understanding the markets in which these businesses operate.

So we would be better off asking ourselves if Metal & Mining stocks are right areas to invest in, rather than thinking of timing the investment first . Because if we can strike a balance between long term investment horizon and potential in the subsequent market , then possible downswings in business cycles should be taken care of by means of longevity of the investment period.

We can enlist following points to briefly analyse India as a market to have the potential for the growth of Metals & Mining Sector :

Demand Growth :

India is a energy hungry country with ever increasing demand for power, reflecting huge appetite for coal based thermal power. Cement industry in India ( propelled by Infrastructure & housing spend by government) will aid the growth in Metals & Mining sector. Demand for Iron & Steel is also set to continue over a long time given the strong growth expectations (albeit with current economic slowdown hiccups) for the Infrastructure , Automotive Industry & Residential Building Industry.

Attractive Opportunities:

There is a significant scope for new mining capacities in iron ore, bauxite and coal and considerable opportunities for future discoveries of sub-surface deposits. Also massive infrastructure development needs of the country will continue to provide lucrative business opportunities for steel, zinc and aluminum producers.

Policy Support :

Over the years govt has realized the potential of Mining & Metal industry and has come up with various initiatives such as :

a. Increasing FDI caps in the mining and exploration of metal and non-metal ores to 100

percent.

b.National Mineral Policy for transparency, better regulation and enforcement of balanced

social and economic growth into the sector.

c.Implementation of Mining Surveillance Systems to curb illegal mining activities.

Competitive advantage:

India benefits from a strategic location that enables convenient exports to developed as well as fast-developing Asian markets. It also holds a fair advantage in cost of production and conversion costs in steel and aluminum.

So above from above points, we can sum up that India as a market has enough potential for bringing in growth avenues for homegrown Metals & Mining Companies. Specifically on a long term basis.

And as far as picking up of safer companies is concerned , we can have quantitative approach for arriving at such companies by analyzing them on following Growth & Safety Parameters :

# Financial Health - strong balance sheet with sustainable debt levels, strong cash flows

and minimal pledged shares

# Past track record - in terms of earnings and revenue history, past earnings growth

analysis, Various performance indicator ratios such as RoE, RoCE etc

# Competitive advantage over its peers.

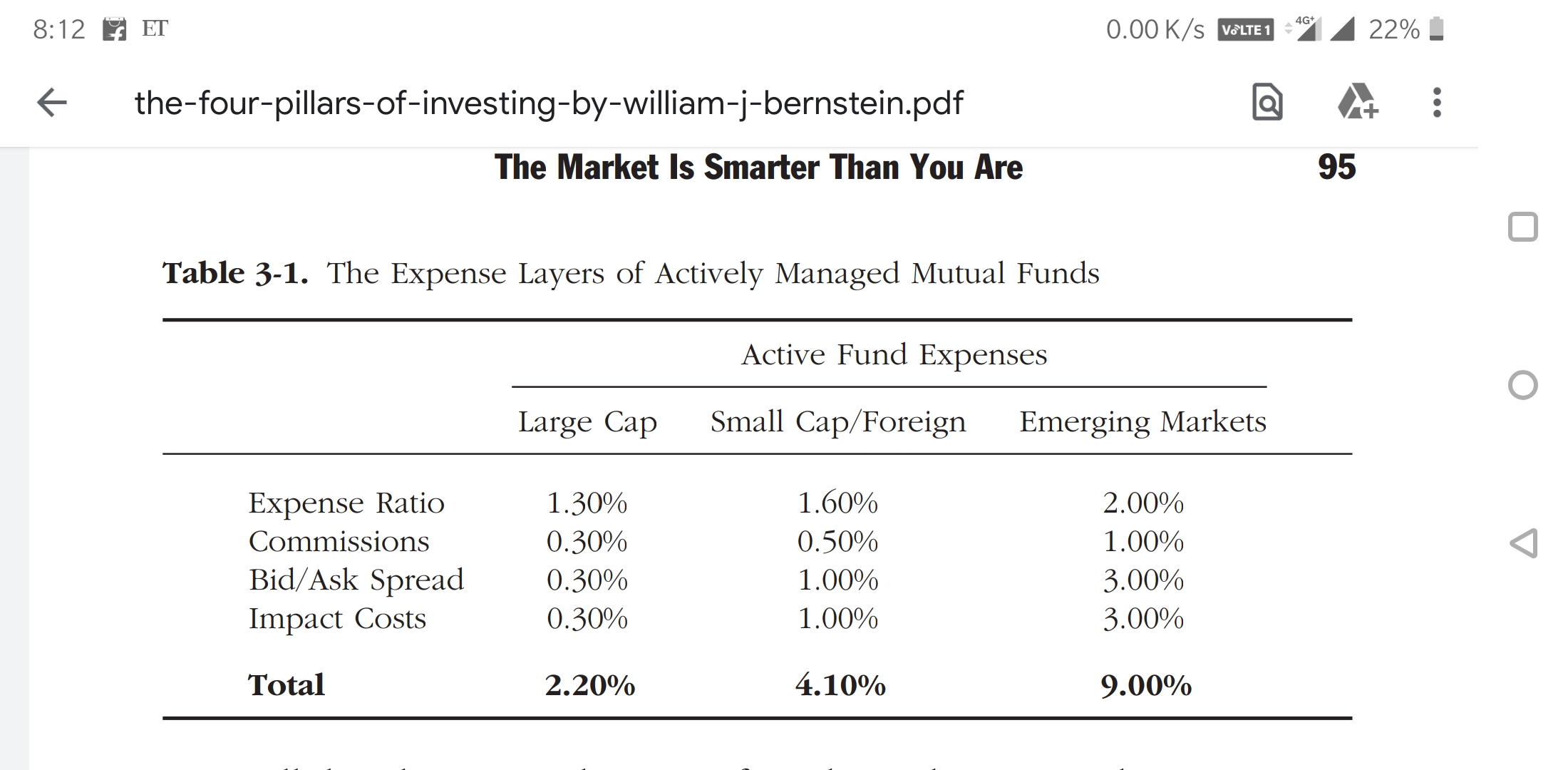

The above screen shot is from the book “four pillars of investing” by William J Bernstein. It shows the table containing different costs associated with mutual fund investing.

The last two costs, viz bid/ask spread cost and impact costs which account for 3% each, are they applicable in indian context also? Could you throw some light on to that? Thanks in advance

Bid-Ask cost is a fancy way of saying there’s low liquidity in the stock.

Let’s say you’re planning to buy HDFC Bank at Rs. 1280 tomorrow. Every day, multiple Crores of shares are being traded in HDFC Bank. So when you place a Limit Order for Rs. 1280, you can be assured that the trade will be executed at the best possible price within Rs. 1280. This is because the Bid-Ask spread as they say or the difference between the highest Bid and lowest Ask, probably within Re. 1 or so. Re. 1 as a percentage of Rs. 1280 is 0.078125%, which is nothing.

But if you are buying a stock with low liquidity, let’s say DHP India. It is currently quoting at Rs. 470. Let’s say you want to buy it at Rs. 470 itself. Even if you place a Limit Order at Rs. 470, there’s very little guarantee that it will be executed. Ask prices are likely to be all over the place. Your best best is to place a Market Order (Before very carefully verifying the descending order of Asks for the Quantity you want). So instead of Rs. 470, you may end up with say, Rs. 475-80 as the Average price for the transaction(s). In this case, the Bid-Ask spread could be as high as, say 1-2%. Whatever be the case, this is an additional cost on the investor imposed by low liquidity.

For very large sums of money, I can see this being a problem. In fact, I remember Mohnish Pabrai saying that the difference between his first and last purchase in Rain Industries was as high as 50% - meaning there was not enough liquidity, even across several days, for the quantity he wanted to purchase in Rain. For retail investors with smaller sums of money, I don’t think this is a big problem. Just make sure you always place a Limit Order. If you can’t due to low liquidity, make sure you place a Market Order only after carefully reviewing all the Ask prices corresponding to the Quantity you want.

Why is it that over 90% of the investors I meet focus on sales, profit margins and other ratios but don’t even calculate the basic cost of equity. Investments in bonds and other fixed instruments seem dull to many investors today but why do most of them don’t take the time to take out the returns they should get from a portfolio of companies or a singular company in that matter before investing?

I apologize if my question is not in line with the forum thread. Please message and I will ask for deletion.

(i am trying to give answer as a cost of capital as it includes borrowing also in addition to cost of equity)

Practical answer : if someone says his hurdle rate of ROIC is 15% or 20%. Usually it covers the cost of capital sufficiently to become profitable

Prof Aswath Damodar share a excellent paper on this where he studied more than 8000 US companies and on average cost of capital was 8% according to him (and it’s not a fixed number it goes on changing)

So practically taking gross number which should more than risk free rate of India is fair enough

Theoretical answer : read his paper and decide your self

I totally agree with you Ashit.

But just to be on the safe side. Take it as 9.5 and see the magic.

Thank you for sharing the pdf.

It was refreshing rereading it.

If you have any other cases on WACC, please do share.

The 50th Percentile Cost of Capital in India is actually closer to 13%. Meaning for an Indian company with average Risk, at least 13% should be the Discounting Rate (That is, if you believe in CAPM).

@dineshssairam

Dinesh I have some doubts

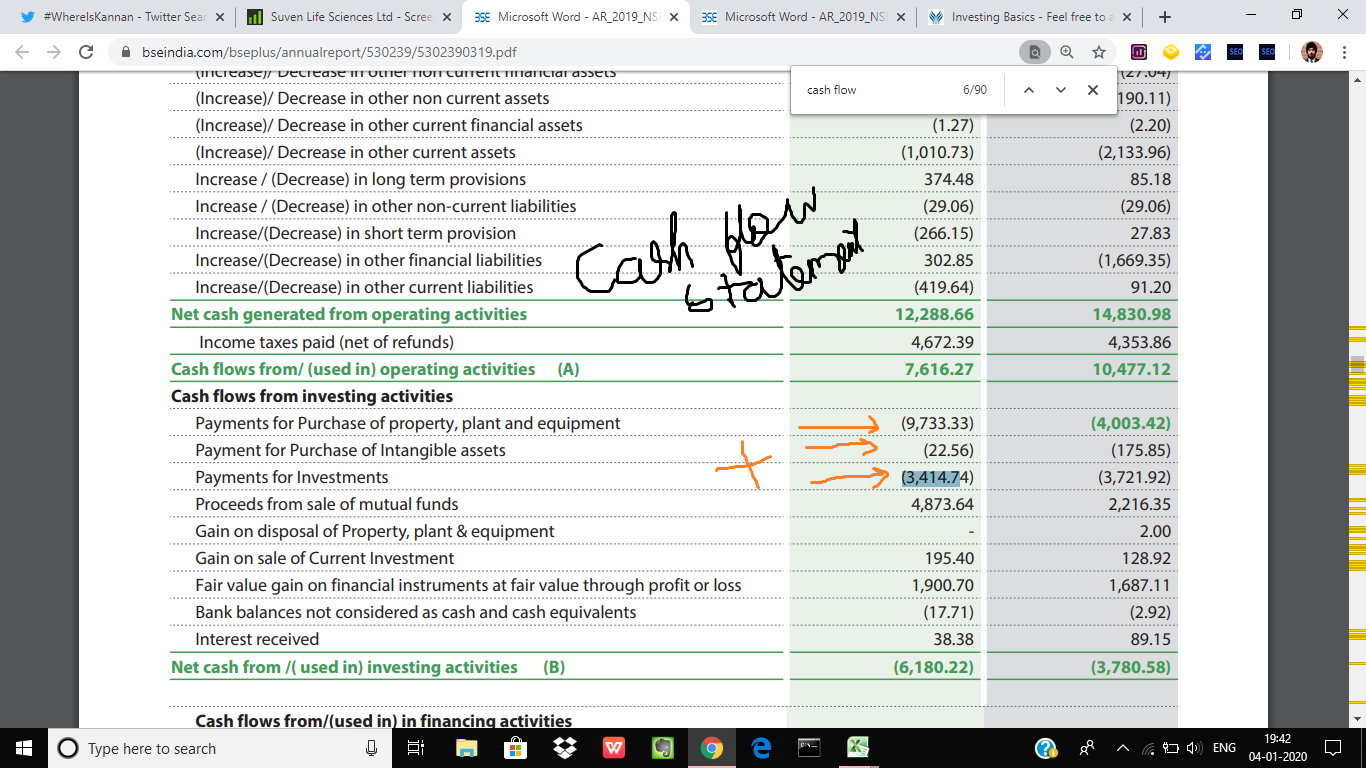

I am in the topic of net capital expenditure.

What i try to do is select a particular topic and try to practice it till i get adept to the subject.

According to Damodaran, the formula for

Net Capital Expenditure= Capex (from cash flow)-Depr.+R&d expese-Amorti+Aquisition

I have attached excel file where i have calculated the figure please let me know what you think about it

The company is Suven Lifesciences

I have calculated the capex by adding purchase of property + intangible assets+ investments

My question is that some of the investment goes into fixing the existing assets (repairing machinery, parts etc)

How to remove that expense from the above calculation?