While studying a paper company, I observed that paper industry is one of the cheapest sector currently (P/E of 5 to 6). In past too, sector usually traded cheap at average P/E of 7 to 8. While I understand this is cyclical industry but so is steel or cement (& in my view cyclicality in steel is much more than paper) but still they trade at relatively higher multiple. Could someone please guide how to interpret this?

In typical cyclical industry P/E

When the EPS is high, then the P/E becomes less but the high EPS is not sustainable hence the PE rerating does not happen in case of cyclical industry. Eg - J K paper

When the EPS is low(earning destroys), then the P/E becomes high(It is not due to rerating of PE).

Eg - Tata Steel

Everything is cyclical but paper and steel are deeply cyclical.

Cement is not too much cyclical.

2 Likes

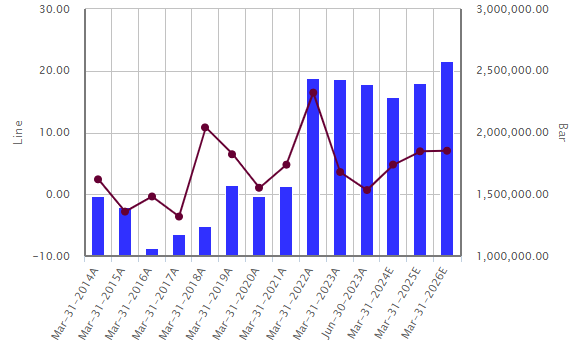

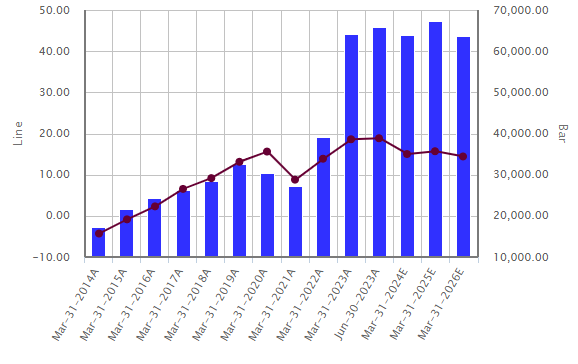

Thanks @royatirek for the response. I usually see companies revenue & margin to check if the company/sector is cyclical or not. Please see below charts for steel and paper industry (vertical bars depict revenue while line chart shows net profit margin).

For tata steel, while, revenue’s are increasing but margins are fluctuating, hence yes, it is cyclical.

However, see below chart for JK paper

I see both revenues and margins growing consistently. Should we still consider this as cyclical?

2 Likes

Market thinks so as the rerating in the paper industry is not happening.

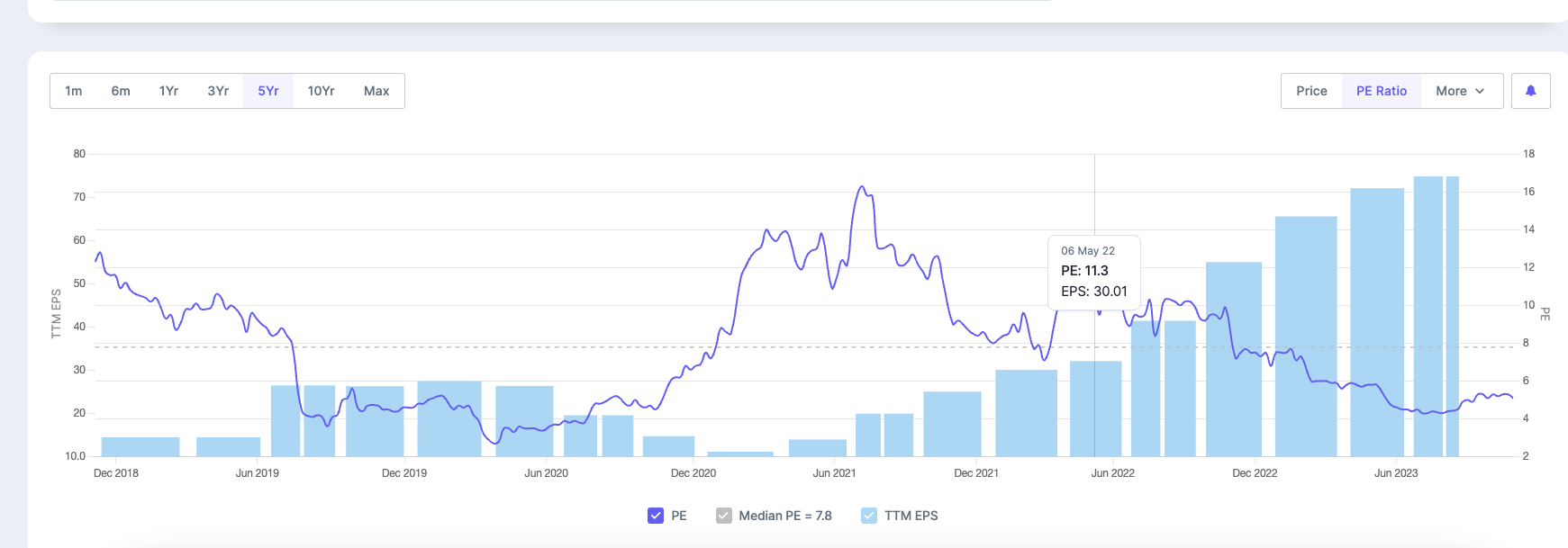

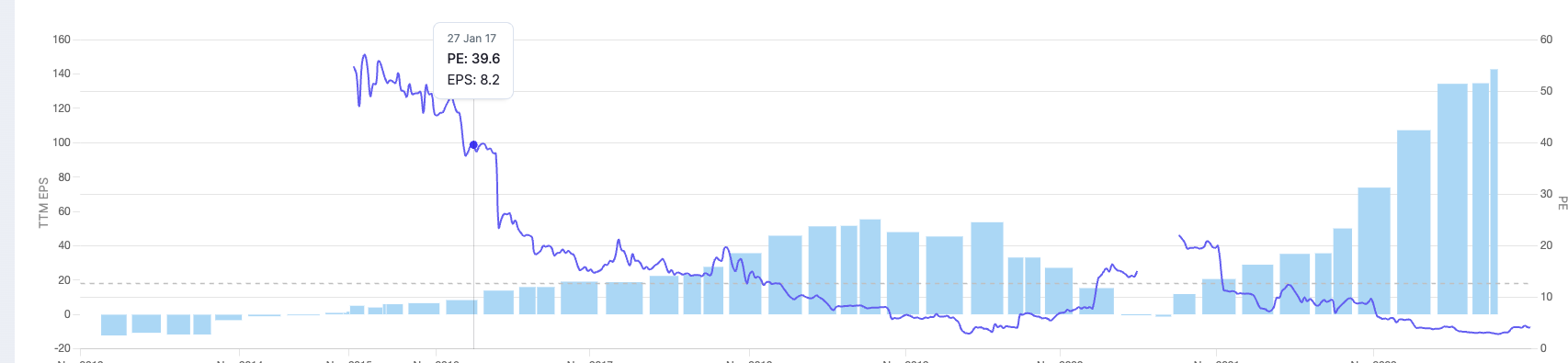

I normally look at the EPS. PE vs EPS of 10 years for JK paper Ltd. (I must admit that it is looking less cyclical after your answer)

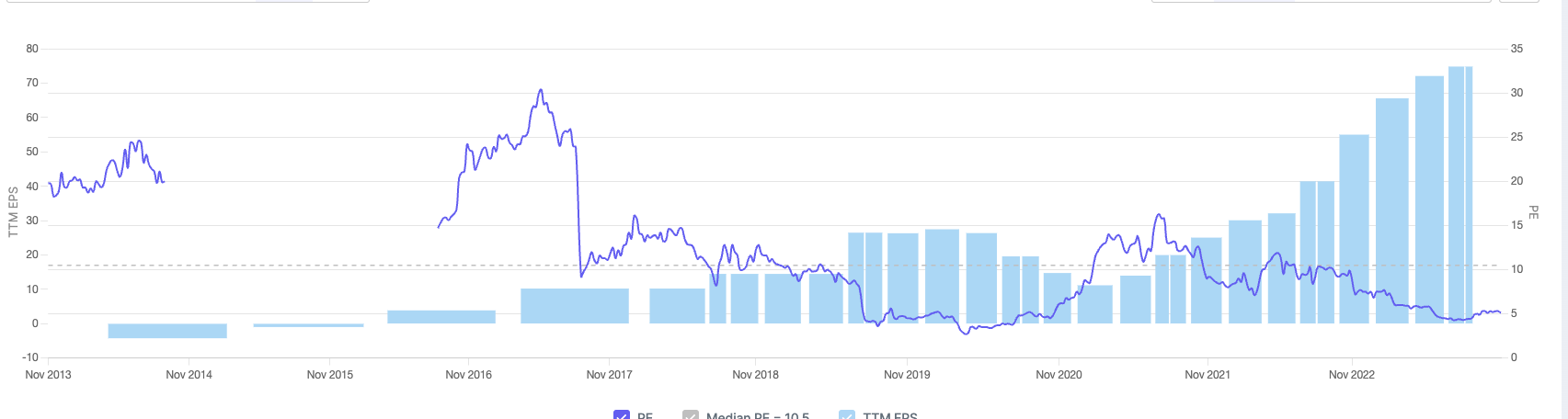

Andhra Paper

If it is able to sustain the net profit margins for very long time, hence changes of rerating can be there. It is only possible if this time by your research you can know that something is different this time or JK paper is a different beast.

From the article(How to do Business Analysis of Paper Manufacturing Companies - Dr Vijay Malik)

In cyclical industry, each time investors and owners think that this time is different and invest in capacities.

Though there are only few companies that are able to become consistent compounder from being a cyclical company.

In the article there is also a case study on Century Textiles & Industries Ltd,

I am not expert in the paper sector and hence will like to not answer it further.

Disclaimer - Not even a novice in a paper industry and take my feedback with the pinch of salt.

3 Likes

Hi,

I want to invest in small or micro cap companies in US. Does anyone knows any ETF or Mutual Fund from US market which invest in small or micro cap? Like we have MOSL Micro cap 250 index.

Also how can we gain knowledge about small/mid cap listed companies in US. We know about Indian companies as we grew up there and used the products. But it is challenging to find small/mid cap companies. e.g. if we have to find wire and cable companies similar to Poly cab or any solar company, I have no idea to shortlist the company. So any pointer will be helpful

No of units will not increase, but NAV value will increase. This is same whether the fund is growth fund or dividend type(IDCW).

1 Like

Hello all,

I have a query after looking at performance of companies like RACL, SBCL, AngelOne ,MapMyIndia etc.

What should be the approach for a new investor when looking at companies with good result? Because these companies are in growth phase or already grown a lot, there valuation will always be on expensive side. What option does retail investor have in such scenarios? Does one wait for the correction in these companies or simply ignore these one and look for newer options. ?

This is not from a point of FOMO but when you encounter companies with good recent past record this question can be natural.

Thanks

There cannot be a standard one size fit all answer to all these companies. Its specific to each company. I can share my views about RACL . Auto ancillary companies are always dependent for their sales and price on big OEMs while.on raw material supply side they are dependent on big metal companies . So from both sides they are squizzed and hence not in a great position to expand their Profitability. So I sold it within weeks of realising this mistake. Since business model itself has no moat, I would.never care about its valuations. First business then valuations. Always.

1 Like

Thank you so much. This gives me a good prospective.

1 Like

There are always exceptions, the one just keep going. Example Mold Tek packaging. They should be squeezed from both sides as they do business with big companies. But they have created their niche.

RACL also seems like this. Going after high margin business, not going for mass produced vehicles but with luxury vehicle manufacturers.

These are my views only, do your own diligence.

Cheers

1 Like

Mold-Tek I am.holding. Its not.comparable to Auto ancillary companies. Mold-tek is diversifying into many sectors, be it Paints, FMCG, now even Pharma…And within each of these sectors, many big companies its working with. So they do have Pricing power. They are not totally helpless like auto ancillary. Correct me , if I am wrong.

Mold Tek does not have pricing piwer. Mold tek budiness practise is that allows it to earn good margins.

When you work with like of Asian Paints or Nestle or something and you are intermediary you do not have pricing power. They will just hung you dry to last drop to increae their margins.

What boxes they pack, others can also pack.

What they do to pack those boxes, others cannot do easily.

This is not mold tek thread, so will not discuss further.

Disc: not invested

1 Like

Is there any website where we can see industry category of each listed company? e.g. for each company, is there any place where we can see if it is finance or auto or chemical company? Not sure if this information is present in BSE or NSE website

On screener you can see from which sector it is alongwith its peer companies too.

I was looking for entire dataset of listed companies along with their sectors. It will be time taking exercise to go through each company on screener and finding its sector. Hence I was asking if this information is already available somewhere

Sector-wise companies/stocks were available on money control. You may want to check that out.

1 Like

Hi folks,

I have been following this company called Sigma Solve ltd since last couple of years and they seem to be doing well.

I have question regarding their recent corporate filing. So their majority of revenue comes from Sigma Solve Inc (a subsidiary of Sigma Solve ltd) which they owned 60% earlier and now it is raised to 100%.

I don’t understand how the raising to 100% is done (as there is no outflow of cash). following is the statement which i don’t understand.

Here is the corporate filing

Sigma Solve Inc. is the Subsidiary

Company of Sigma Solve Limited

(“SSL”). SSL held 59.81% stake in the

Subsidiary. However the said stake of

59.81% has raised to 100% as a result

of Buy Back of Securities floated by the

Sigma Solve Inc. SSL has refused to

participate into the Buy Back of Sigma

Solve Inc. and as a result today when

the Buy Back has completed in Sigma

Solve Inc. the stake of SSL in Sigma

Solve Inc. is 100% and made it its

Wholly Owned Subsidiary. Also, there

was no Outflow of Cash from the funds

of the Company.

Totally going by what you posted, I understood that SSL hold 59.8% stake in SSI, remaining stake were with some other shareholders. Now, SSI has bought back few of its own shares (40.2%) and since SSL havent participated, all shares that were bought back were from remaining shareholder portion. Effectively, post this, there were no share left with other shareholders and hence SSL became 100% shareholder of SSI

1 Like

thanks for your response. I dont uderstand why there is no outflow of cash from the funds

of the company for purchasing these shares?