This post deals with overall introduction to the International Generics industry

At the outset, kudos to all the folks (@crazymama @ankitgupta @ananth @Donald @spatel ) who as industry outsiders tried to crack the International Generics puzzle and have been making their best efforts to track Indian pharma industry. I have some past working experience in the Industry and am happy to share my understanding of the subject and look forward to collaborate with interested folks. [@stockcollector]

Thanks to @Donald for creating this thread dedicated to International Generics (IG). [Having opened this thread in VP Expert Network, he should also get ready to open his wallet to foot my bill for anti-anxiety medicines that I need to consume to write posts that justify the Expert tag ![]() ]

]

This thread intends to cover all aspects of the IG value chain (R&D to Sales in International Market). In a few months, all of us (who are interested in understanding this domain) should have greater clarity (or confusion - some of the existing notions must get shaken!) on functioning of this industry segment, the key risks from investors’ point of view and understand the limitations (due to information asymmetry) that retail folks have to deal with.

Laudable work has already been done by VP community folks in the following threads: [If there are more, kindly point them and I will add them to the list]:

-

ValuePickr Generics Pharma Dashboards - Focusing on asking the right questions!

-

VP CHINTAN BAITHAK GOA 2015: Ananth Shenoy: GENERICS PHARMA PIPELINE BASICS

-

VP Chintan Baithak Goa 2017: Ankit Gupta: Challenges for Indian Pharma Cos

Though many members are already familiar with various aspects of the International Generics(IG) business, I am going to initiate coverage (this is the closest I will ever get to write an Equity Research report ![]() ) with the basics.

) with the basics.

Absolute Basics

For people who are new to the sector, it is essential to understand the fundamentals of New Drug Development (also known as Brand / Innovator / New Chemical Entity) and Generic Drug Development.

New Drug Development

- Developing a new medicine that has specific mechanism of action and target disease(s) indication.

For example - drugs like Ramipril, Perindopril are ACE Inhibitors which are used to treat hyper-tension and heart related ailments. This video will make it clear:

Now, the process of New Drug Development:

Summary of US FDA’s framework for approval of New Drugs.

The distinction between New Drug Development and Generic Drug Development:

Brand / Innovator / NCE (New Chemical Entity) Drugs:

- Drug Development Cost - [upto bringing the drug to market] - Around 1 Billion USD. [Varies depending on the type of drug - but this is taken as a general benchmark number]

- Time taken to develop the new drug - Around 10 Years

- Out of 1000s of potential molecules, only a few get designated as drugs capable of treating a disease wherein their benefits of treating the disease indication outweigh their side-effects. During 10 year period of 2009-2018, 271 New Drugs were approved by US FDA - making it an average of around 30 drugs per year. [The comparable number for biologics is 85 but we are NOT discussing biologics and biosimilars here.]

- Patent term period - 20 years. There are complexities and nuances - but in a general sense the new drug gets a patent term of 20 years. There are various patents related to the new drug. The most basic being a composition of matter patent that is held for the mother compound (the new chemical entity / compound) and its derivatives. Patents can be challenged through non-infringing routes of development or a direct invalidation challenge to the patent claims filed by the innovator. The patent term begins from the date of filing. And by the time the drug is finally approved for marketing by a regulatory authority (like US FDA) around 8 years maybe lost by the innovator company. Hence there are patent term restoration rules.

- Regulatory exclusivity - Drug & Health regulatory agencies like US FDA provides exclusivity other than patents. A snapshot of the type of exclusivities provided by US FDA is given here.

- Clinical Trials are essential for proving - safety, effectiveness, efficacy. Done in 4 phases - Phase 1 : 20-80 (normally healthy) volunteers - objective is to see drug safety / adverse reactions. Phase 2 : A few hundred patients(100 to 500) - objective is drug safety + efficacy. Phase 3 : Upto 3000-4000 patients - drug efficacy / effectiveness, whether the drug’s benefits outweigh its risks / adverse reactions. Drug approval is done after Phase 3 results. However, Phase 4 continues post drug approval to check long term impact of the drug on human body.

Generic Drugs:

- Drug Development Cost - 1 Million USD to 5 Million USD . So this is around 1% to 5% of the Brand / Innovator drug. [1 Mil. - Simple products, 2-3 Mil. Complex Products, 4-5 Highly Complex/Speciality products.] [Most generic companies sell products in many regulated markets/territories. Their drug development process is focused on the first market where the product is intended to be launched or the most promising market. For making product filings in other markets, they reuse as much data and protocols that were developed for the first filing. The cost for dossier extension would be around 0.5 to 1 Million USD.]

- Time taken to develop the generic (from the API stage) - Around 3-4 Years

- Generic is developed based on literature published by the Innovator - reverse engineering is done for generic drug development.

- Can be launched only after Innovator’s patent term (in the relevant territory) has lapsed OR the patent is challenged by generic. But, normally, CANNOT be launched upto 5 years from Innovator’s launch because of Data Exclusivity granted to Innovator drugs. [i.e. the Generic CANNOT submit its drug application using Innovator’s data]

- NO Clinical Trials.

- Instead Bio-Equivalence is used to demonstrate that the rate and extent of generic drug’s absorption in the body (or at the intended site) when compared to Brand/Innovator does NOT have statistically significant differences. Get this fact clear - Generics do NOT have to prove efficacy / effectiveness of the drug!!. Innovator has already proved that the benefits of using drug outweighs the risks and hence is suitable for treatment of certain disease indications.

What is International Generics?

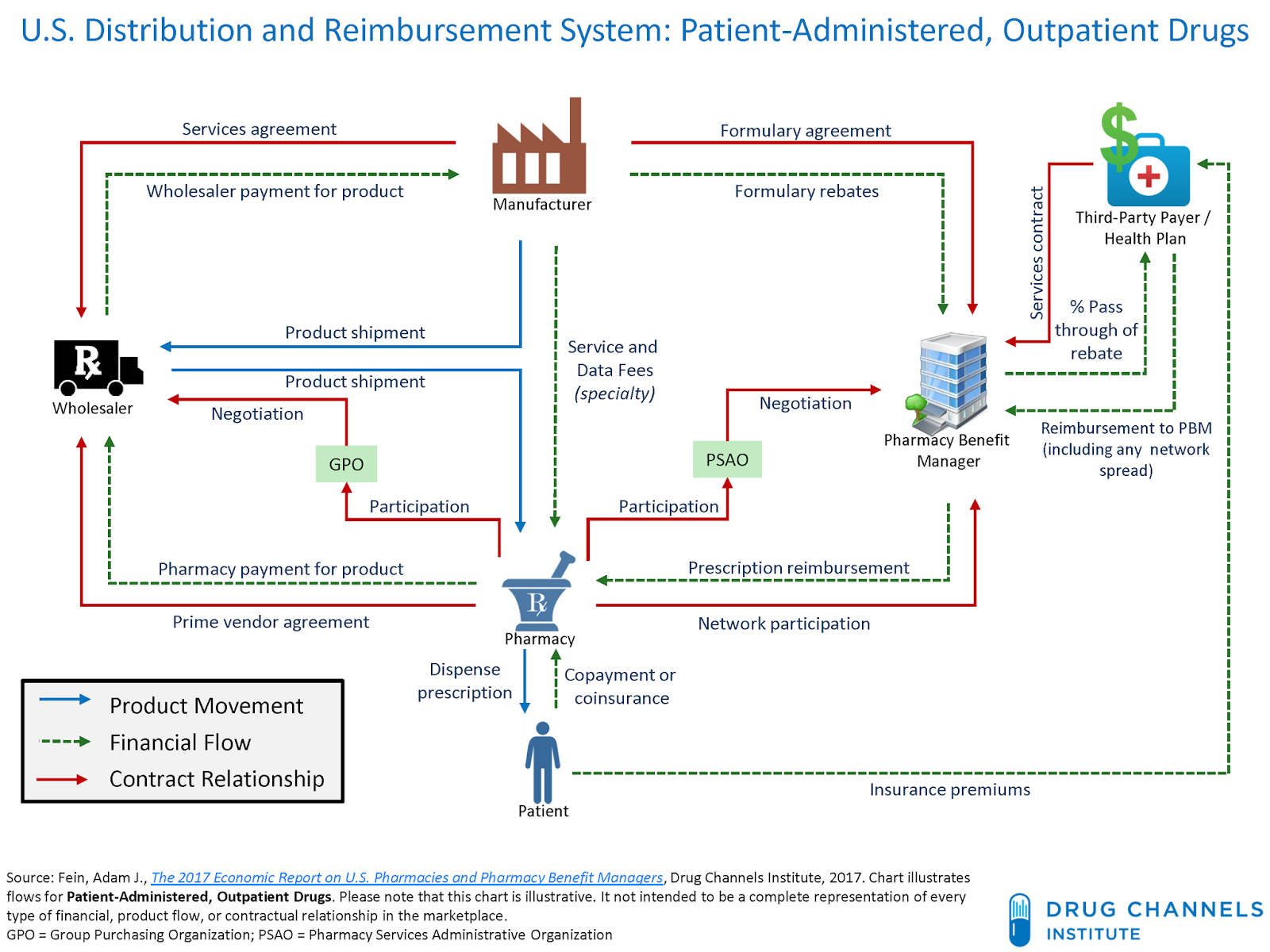

The term encompasses generic drugs market across the world - having regulated as well as non-regulated / semi-regulated markets. Normally, when reference is made to International Generics, it is for regulated markets i.e. those countries/territories where a health and drugs regulatory agency (like US FDA, MHRA UK, EMA EU, ANVISA Brazil) has codified (rather stringent) regulations for submitting an application (normally known as Dossier or US Specific ANDA) that is reviewed and approved explicitly before the drug can be launched in the respective market.

Not only does the final drug (known as Formulation or FDF - Finished Dosage Form) require submission of application, but an application - Drug Master File (DMF) or Active Substance Master File for the Active Ingredient (i.e. the medicine in its raw form - called as Active Pharma Ingredient / API / Bulk Drug) is also required.

What does generic drug development process look like?

Companies pursuing generic drug development will have the following processes and operating models:

- Product selection - This is the stage where company identifies drugs which have a sizeable market (or even promising therapies in advanced Clinical Trials Stage - like Stage 3) in a particular geographic territory/country and across all the major regulated markets where the company intends to market the drug. The company creates a “business case” or “project initiation document” that captures the following:

-

Volume - In terms of No. of tablets, No. of capsules (for Oral Solids), other units - ml, mg, gms etc. for other routes of administration like Opthalmic, Injectables, and Dermatological products. Volume is of paramount importance; because while the annual Brand Sales for a drug may be a few billion dollars, it may be driven solely by exorbitant prices (one pill selling at 1000 USD) and low volumes. So even if 3-4 generic companies can crack the code and get their marketing approval, the resultant market maybe a tiny fraction of the brand market.

-

Price per unit/SKU and Market Size - Volume multiplied by the prevailing / expected price per unit/SKU will give the Market Size (Value) In $ Million. Guesstimates of annual brand drug sales and probable generic sales are worked for the next few years. This is done primarily using Industry specific databases / solutions provided by organizations like - IQVIA, [Please do watch the forecast link video given on the IQVIA page - will give you the overall idea of what is involved in the process], IPD Analytics, Clarivate Analytics Cortellis, Symphony Health etc. Expected competition from other branded drugs that treat same disease indication, generic competition, and Price Erosion scenarios are worked out. [Price Erosion defined: Assume the Brand / Innovator drug was sellling at 100$ per bottle. If the Generic drug sells at 2$ per bottle then 98% is the price erosion.]

-

Guesstimating the expected market size involves several intricacies like:

(a) Products which are not facing any generic competition when the business case is being worked out - The Gross-to-Net data for Brand drug sales may not be accurate. (This problem is specific to US Market)

(b) Products already facing generic competition when business case is being worked out -

Brand Net Sales + Generic Net Sales → with market share captured from Brand as well as Generics and Price erosion to both the market sizes need to be applied.

(c ) Existing Brand Sales may NOT reflect the appropriate base value of the market size ($ Mn and/or Vol. / Units) - Brand sales Value (price) or Volume is going to get affected by another competing product [different NDA / Brand small drug product] which treats the same disease maybe through a different mechanism of action. i.e. instead of Generics, a piece of the existing pie is taken away by a different Brand/Innovator. -

IPR Landscape around the world and priority of market launches - If generic companies launch their products after all patents of the brand/innovator expire then their operations are NOT going to be commercially viable. Heart of running a successful generic company is getting the IPR Strategy right! And Pharma IPR is a complicated matter. The company will scan IP landscape across all the territories and decide the development and launch strategy for each territory. The IP needs to be scanned for FDF/Formulation as well as the basic drug APIs. Generally, the dossier / ANDA development will be done for the most promising territory (say USA) and then it is extended to other markets; reusing data and protocols as far as possible.

-

API (Active Pharmaceutical Ingredient) Source - Well the equation is simple - No API = No FDF / Forumation. Companies who are vertically integrated will try to have their own API in the filing. If the API is not inhouse then it will tie-up with an API manufacturer. As a part of derisking strategy, more than one API source may also be used in filing - because API switching after drug approval is a long process taking minimum 6 months.

-

Estimated cost of manufacturing (Conversion Cost) - Depends on the type of product and expected commercial batch size. Normal Oral Solids could be between $5 to $15 per 1000 tablets/capsules, Oncology / High Potency drugs would be significantly more expensive because they require special containment facilities.

-

Company’s competency (R&D and Manufacturing) in developing the drug.

-

After evaluating the above parameters (and maybe some more), the company decides whether it should add a drug to its R&D grid/pipeline. Depending on the outcome of subsequent stages, some of the selected drugs may not see the finish line.

-

R&D / Chemistry stage to develop API (Active Pharmaceutical Ingredient - the real medicine which strikes the disease) drug development - also known as Chemistry - because we are developing/synthesizing new molecules. Actually, strictly speaking, not new molecules, but development of existing molecules through literature search and reverse engineering.

API drug development can be done in-house or APIs can be outsourced from an API manufacturing company. Or a combination model - some APIs are manufactured Inhouse and some are bought from API suppliers.

Manufacturing APIs need KSM (Key Starting Material). Again the KSM maybe made inhouse or (generally is) bought from KSM suppliers.

The development of API starts in R&D center of the company at a Lab-Scale. The molecule is developed using literature available on the API used by the brand drug and studying the API (through dissolution and other analytical methods) . Route of synthesis is decided, tweaked and analytical tests are performed to check whether the molecule developed is same as the desired API. Pubchem can be accessed to understand chemistry of the molecules/compounds. -

Scale up of API - Molecule developed in R&D is at Lab-Scale i.e. would be upto few grams to few 100 grams. The reactor sizes would be like 1KL- 3KL. Once it is established that R&D has successfully developed the molecule at Lab-Scale, it is scaled up to higher batch sizes in pilot plant or commercial plant. The larger size batches manufactured are preserved / stored for recording stability data and all the necessary documentation for Active Substance Master File / DMF is prepared. In case of vertically integrated companies, the ASMF / DMF would be filed only around 4-6 months before their Dossier / ANDA submission. Because filing an ASMF / DMF too early would reveal the drug development pipeline to competitors.

Successful Scale-Up is of paramount importance. One cannot assume that if a 1 KG batch is stable and consistently successful then 20 KG, 200 KG or 2000 KG will also be successful simply by increasing the ingredients and reactor sizes by factor of 10x. The typical properties of each API make each stage of Scale-Up challenging. [On a lighter side if a non-technical person like me tries to do scale-up from 20 KG to 200 KG by increasing the ingredients and reactor size by 10x then we can expect to see some SpaceX style rocket launches from the reactors ]

]

All finalized batches of API have Certificate of Analysis (COA) which certifies their properties and accompanies the regulatory submission or shipment to customer site / captive facility. The API manufacturing process looks like this. Its like a typical chemical manufacturing/synthesis process with lots of bad odor and high temperature around the manufacturing facility. -

Formulation Development - Just as the case is with API, the company may (a) Do Formulation development in-house (b) Get it done externally - outsourced external devp. (c) Do in-house development for some drugs and outsourced for some. Formulation development first happens at lab scale inside the R&D center. The formulation development of generics is always done with reference to a Reference Listed Drug (RLD). Scientists access literature related to the brand/innovator (or the RLD if the brand/innovator is not available) drug, and use reverse engineering techniques involving dissolution and analytical methods to develop the formulation. Once the drug is formulated at lab scale, depending on the route of administration of the drug, the appropriate Bio-Equivalence activity is carried out in various phases.

-

Bio-Equivalence (BE) - Reiterating what I wrote earlier. BE is used to demonstrate that the rate and extent of generic drug’s absorption in the body (or at the intended site) when compared to Brand/Innovator does NOT have statistically significant differences. Get this fact clear - Generics do NOT have to prove efficacy / effectiveness of the drug!!. Innovator has already proved that the benefits of using drug outweighs the risks and hence is suitable for treatment of certain disease indications. There are different BE strategies for different types of drugs. Pharmacokinetics of the generic and RLD/Brand drug are to be compared and their difference is to be demonstrated as statistically insignificant. BE is normally done in first in the Pilot phase with limited no. of volunteers (would be less than 20) and drug dosing / drug application results are checked. If Pilot phase results are not successful then depending on the situation - either the protocols are redesigned and por even the formulation may have to be redeveloped. Once the Pilot phase results are promising then BE is taken to Pivotal stage. Pivotal Bio stage is a full-fledged BE study with greater no. of volunteers (upto 40). If Pivotal Bio fails then the company may either go through reiteration of protocol redesign, formulation development, Pilot BE and Pivot BE or looking at the market scenario, product potential and time and resources required for redevelopment, the company may decide to stop the drug development process at this stage. If Pivotal Bio is successful then preparations are done for technology transfer to scale-up the batch size and manufacture the drug at Pilot Plant / Commercial Plant for exhibit / regulatory submission batches.

-

Scale-Up and Exhibit Batches - Upto Pivotal Bio stage, the formulated drug was being manufactured at Lab-Scale. (e.g. Few 100s or 1000 tablets.) Once Pivotal Bio is successful, all the blood, sweat and tears are ready to create the ground for manufacturing Scale-Up / Test batches (net practice) followed by Exhibit / Submission batch. [Scale-Up batches would be of the size around 100,000 Tablets.]

The current regulations require 6 months of stability data for the exhibit/submission batches. The entire set of documentation for filing Dossier/ANDA is prepared during this 6 month waiting period. On elapse of 6 months, the stability data is included in the Dossier/ANDA application and it is sent to the regulator! Phew!

-

Regulatory approval (or rejection) and IPR clearance - The general reviewing and approval process is explained succinctly here. After the application is filed:

-

First hurdle to clear is RTR (Refuse to Receive) - Though one can contest against RTR, but not having RTR is what companies aim (and hope) for.

-

If its ANDA filing then the patent certification (Para I, II, III, IV filing) is of great importance.

Note : In US filings, ANDA filing (Para IV) is considered an act of Patent Infringement and the US FDA is involved in the Para IV filings with 30 Month Stay etc. In other markets, actual commercial launch is considered as an act of Patent Infringement and their Drug & Health Regulatory bodies are NOT involved in the patent litigation between Innovator and Generics.

US ANDA filings related core part: Quoting directly from US FDA website: -

The Hatch-Waxman Amendments amended the Federal Food, Drug, and Cosmetic (FD&C) Act and created section 505(j). Section 505(j) established the abbreviated new drug application (ANDA) approval process, which permits generic versions of previously approved innovator drugs to be approved without submission of a full new drug application (NDA). An ANDA refers to a previously approved new drug application (the “listed drug”) and relies upon the Agency’s finding of safety and effectiveness for that drug product.

-

The timing of an ANDA approval depends in part on patent protections for the innovator drug. Innovator drug applicants must include in an NDA information about patents for the drug product that is the subject of the NDA. FDA publishes patent information on approved drug products in the Agency’s publication “Approved Drug Products with Therapeutic Equivalence Evaluations” (the Orange Book) (described in more detail below). The FD&C Act requires that an ANDA contain a certification for each patent listed in the Orange Book for the innovator drug. This certification must state one of the following:

-

Para I that the required patent information relating to such patent has not been filed`

Para II that such patent has expired;

Para III that the patent will expire on a particular date; or

Para IV that such patent is invalid or will not be infringed by the drug, for which approval is being sought.

-

A certification under paragraph I or II permits the ANDA to be approved immediately, if it is otherwise eligible. A certification under paragraph III indicates that the ANDA may be approved on the patent expiration date.

-

A paragraph IV certification begins a process in which the question of whether the listed patent is valid or will be infringed by the proposed generic product may be answered by the courts prior to the expiration of the patent. The ANDA applicant who files a paragraph IV certification to a listed patent must notify the patent owner and the NDA holder for the listed drug that it has filed an ANDA containing a patent challenge. The notice must include a detailed statement of the factual and legal basis for the ANDA applicant’s opinion that the patent is not valid or will not be infringed. The submission of an ANDA for a drug product claimed in a patent is an infringing act if the generic product is intended to be marketed before expiration of the patent, and therefore, the ANDA applicant who submits an application containing a paragraph IV certification may be sued for patent infringement. If the NDA sponsor or patent owner files a patent infringement suit against the ANDA applicant within 45 days of the receipt of notice, FDA may not give final approval to the ANDA for at least 30 months from the date of the notice. This 30-month stay will apply unless the court reaches a decision earlier in the patent infringement case or otherwise orders a longer or shorter period for the stay.

-

The statute provides an incentive of 180 days of market exclusivity to the “first” generic applicant who challenges a listed patent by filing a paragraph IV certification and running the risk of having to defend a patent infringement suit. The statute provides that the first applicant to file a substantially complete ANDA containing a paragraph IV certification to a listed patent will be eligible for a 180-day period of exclusivity beginning either from the date it begins commercial marketing of the generic drug product, or from the date of a court decision finding the patent invalid, unenforceable or not infringed, whichever is first. These two events - first commercial marketing and a court decision favorable to the generic - are often called “triggering” events, because under the statute they can trigger the beginning of the 180-day exclusivity period.

-

In some circumstances, an applicant who obtains 180-day exclusivity may be the sole marketer of a generic competitor to the innovator product for 180 days. But 180-day exclusivity can begin to run - with a court decision - even before an applicant has received approval for its ANDA. In that case, some, or all, of the 180-day period could expire without the ANDA applicant marketing its generic drug. Conversely, if there is no court decision and the first applicant does not begin commercial marketing of the generic drug, there may be prolonged or indefinite delays in the beginning of the first applicant’s 180-day exclusivity period. Approval of an ANDA has no effect on exclusivity, except if the sponsor begins to market the approved generic drug. Until an eligible ANDA applicant’s 180-day exclusivity period has expired, FDA cannot approve subsequently submitted ANDAs for the same drug, even if the later ANDAs are otherwise ready for approval and the sponsors are willing to immediately begin marketing. Therefore, an ANDA applicant who is eligible for exclusivity is often in the position to delay all generic competition for the innovator product.

-

Only an application containing a paragraph IV certification may be eligible for exclusivity. If an applicant changes from a paragraph IV certification to a paragraph III certification, for example upon losing its patent infringement litigation, the ANDA will no longer be eligible for exclusivity.

- Commercial launch

-

Once the regulatory approval is received, the company may launch the product with no IPR litigation (clean launch) or with ongoing IPR litigation (At-Risk Launch).

-

If the generic company loses IPR battle, then “At-Risk” launch can prove to be quite costly. Teva and Sun had to pay USD 2 Billion to Pfizer for at-risk launch of Pantoprazole (Protonix). Apotex paid 76 USD Million to Astra Zeneca for Omaprazole (Prilosec).

-

The company can have its own front-end / subsidiary company in the foreign market or can launch the product with a marketing partner.

-

Depending on the product(s) involved in the agreement, the model with marketing partner may take any of the forms:

(a) Pure profit sharing - Products from India are transferred at an agreed Transfer Price (COGS+ Manufacturing Margin). Profits are calculated on quarterly basis (after accounting for Net Sales, COGS, SG&A and other expenses). The profit sharing is generally in the range of 20 percent to 50 percent of the net profits earned on products. The SG&A (Selling General & Admin Expenses) are however charged flat as a % on the Net Sales number. In many cases this SG&A itself is a substantial profit for the Marketing Partner. Generics does NOT require field-force. The fixed cost structure doesn’t change much by taking new marketing agreements.

(b) Pure Transfer Price model - The manufacturer sells at fixed transfer prices to the marketing partner. The manufacturer margin is fixed irrespective of the prices in market. The upside of profits from net realizable price in market belongs to marketing partner. However, if market price is under pressure then the marketing partner will work on negotiation towards revised transfer prices.

(c ) Hybrid of (a) and (b) - Upto certain level of market prices the transfer price is fixed. Beyond a level there is profit sharing etc. -

For selling through own front-end - most regulated markets require country level and state level registrations of the company. Also there are restrictions on who can register the company (i.e. only local nationals are allowed in many cases). The supply chain is generally managed through 3PL. The front-end team broadly performs demand forecasting, contracting, negotiations, market intelligence and competition sensing functions. Generics do NOT require any field-force marketing efforts.

Some recommended Industry Resources

-

IQVIA / IQVIA Institute (previously known as IMS) is the go to source for understanding macro scenario of all the major IG markets. Regularly publishes reports and webinars regarding prescription drug markets.

-

Healthcare Triage’s YouTube channel - Has lots of easy to understand information on US and Other Healthcare markets.

-

EdX course by Harvard - Prescription Drug Regulation, Cost, and Access: Current Controversies in Context.

-

The Generic Challenge book by Martin Voet

-

US FDA - CDER - SBIA Webinars and SBIA page for information on this matter

-

Bottle of Lies book by Katherine Eban

-

Pharmacology and drug families - PPT - PHARMACOLOGY – Simplified, not Mystified PowerPoint Presentation - ID:4496054

Character limit reached for this post. Will continue in subsequent posts.

| CNBC")

{kind=link}

{kind=link}