Note: Contacted IQVIA, and they gave permission to cite their publicly available reports. The citation to be given is:

Full Report Name . IQVIA Institute for Human Data Science. Month/Year of the Report publication

This post is about US GENERICS MARKET- EVOLUTION OF INDIAN PLAYERS, IQVIA/IQVIA Institute for Human Data Science, February 2019.

Unless otherwise indicated, all charts, excerpts used in this post are from the aforementioned report.

The report can be downloaded from here.

[Please download the report ASAP. IQVIA may archive it in future.]

This is a brief report - around 12-15 pages with charts and graphs. So does not warrant summarizing much. Everybody should read it in full.

Nevertheless, I would like to drive home the point that US generics is a BUYER’S Market.

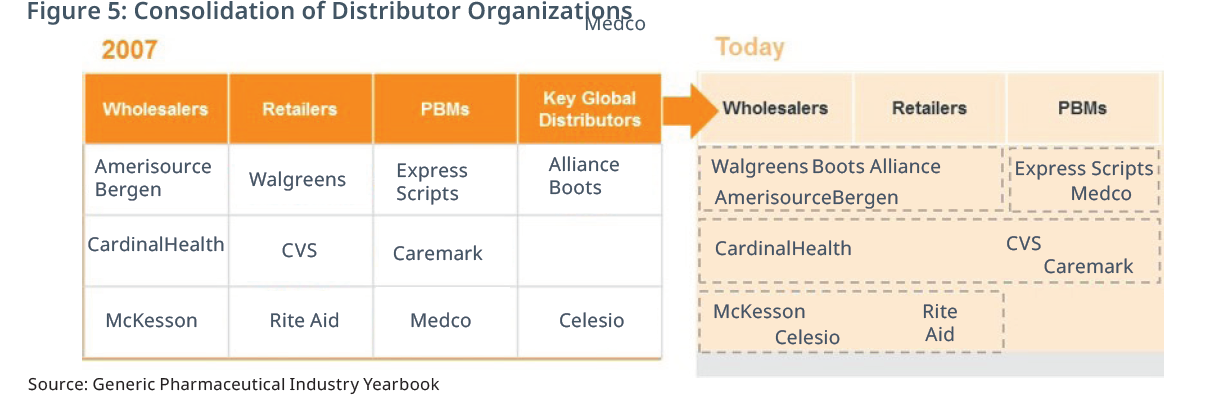

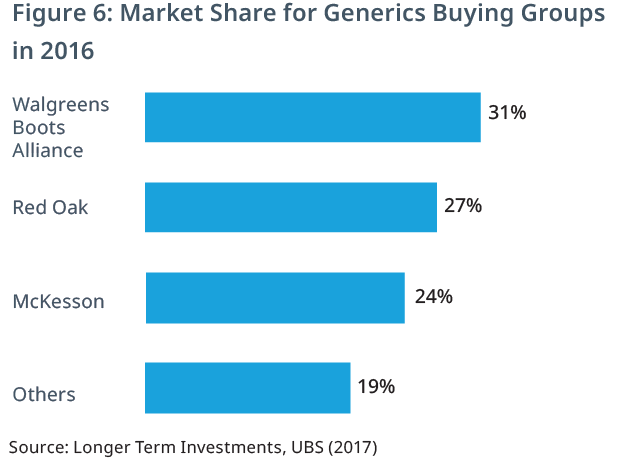

Sharing a paragraph and reference to couple of images from Page 6 of the report.

Blockquote

About a decade ago, US had more than 10 pharmaceutical distributors contributing to ~80% of the US generic market. However, the last decade has been witness to consolidation (Figure 5) so much that the top 3 players — WBAD, Red Oak and McKesson OneStop, have contributed to >80% of the US generics market (Figure 6).

Blockquote

McKesson, CVS Health, AmeriSourceBergen(ABC) are ranked 7, 8 and 10 on Fortune 2019 list (by revenue).

Following them are Cardinal Health and WalgreensBootsAlliance at 16 and 17.

CVS and Cardinal Health have a JV for generic sourcing. The resultant JV company is Red Oak Sourcing. And CVS also aquired Aetna Health Insurance. So, ladies and gentleman, CVS is in Wholesale Distribution (through Red Oak / Cardinal JV), Retail Pharmacy, Health Insurance (Aetna) and PBM (Pharmacy Benefits Manager). CVS is in the entire value chain of US drugs distribution! Maybe someday FTC will scrutinize it - but till then it has enough muscle to bully suppliers.

And the other folks - Walgreens, McKesson, ABC, Cardinal, et.al are known bullies. Well if you command 80% of market share in wholesale distribution and have downstream retail presence as well then suppliers (drug manufacturers) are going to be at your mercy!

Perhaps the only saving grace currently for Drug Suppliers is that the US Government still DOES NOT have a mandatory reference price limit and tendering system for its Medicare (Part D) and Medicaid programs. The US Govt. is the insurer (payor) for around 30%-35% of the US population through these two schemes. Currently, the laws DO NOT allow US Govt. to influence prices under these two programs. Will have a separate post elaborating that.

Imagine being a me-too drug supplier having 10 competitors and selling perfect substitutes of the products/drugs in such a market!!!