Rival Watch:

Found a slide from an Air India document. Sharing it here with my opinion.

One of Air India’s major margins comes from international travel, and this is something Indigo has struggled with. I think this is one reason why Indigo appointed Pieter Elbers as their CEO, given his strong reputation for building an international airline.

For a country like India, we do not have enough airports, nor do I believe we have absolute premium demand. At some point in the future, domestic operations will become commoditized if they aren’t already. The simple reason is that all types of carriers offer the same fare for the same route. Hence, it’s a natural transition to shift to international operations. I believe this is why Indigo has made significant changes in its management.

Indigo has done phenomenally well in the past with domestic operations, but the future lies in international markets. This explains many of the changes we are seeing—stretch seats (business class), a loyalty system, and hot meals. All these will eventually lead to higher margins in the future.

Right now, despite having the largest capacity in India, Indigo is still lagging in the international market. The main reasons are narrow-body aircraft and bilateral rights. Narrow-body aircraft can fly a maximum of five hours, but this comes at a cost: fewer passengers and disgruntled passengers due to no hot meals and uncomfortable seats. The experience on a two-hour flight is vastly different from that of a five-hour flight. To make matters worse, on the routes Indigo operates internationally, foreign carriers often offer a superior and more comfortable product (wide-body aircraft) at almost the same cost. Case in point—Singapore Airlines operates the A380 on the same Mumbai-Singapore route where Indigo uses the A321. There’s hardly any price difference.

I personally think this is what’s hurting Indigo at the moment, and it’s where Air India is taking a lead.

Indigo has taken the initiative and ordered wide-body aircraft. However, these won’t be arriving anytime before 2027. Regarding Air India, I believe they are not as focused on domestic operations. You might argue that Air India Express (AIX) fills that gap, but if you look at the latest winter schedule, even AIX is adding more international flights.

Back to Indigo: I think they are currently focusing on strengthening their existing stations, which means adding more Indian cities to an international destination they already serve. For example, Colombo was previously connected only to Chennai. Now, it’s also connected to Delhi, Mumbai, Bangalore, and Hyderabad. This is a good step. On the tourism front, the sector is performing well, and many Indians prefer to vacation abroad in destinations that aren’t far from India.

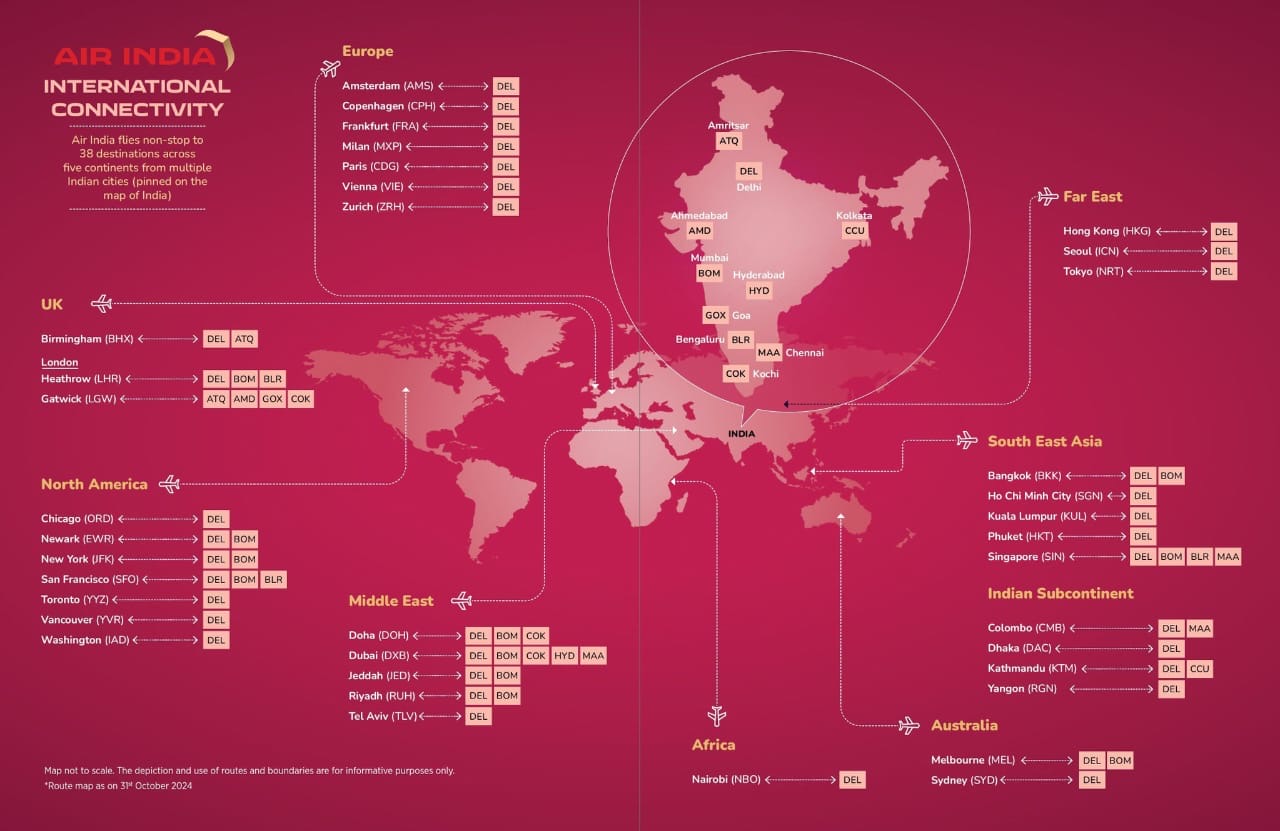

However, what differentiates Air India from Indigo is that while Indigo is primarily connecting Indian passengers internationally, Air India is positioning itself as a transit hub via Delhi and Mumbai. This means Air India can cater not only to domestic demand but also to passengers from other countries transiting through India. For example, a person from Georgia can fly to Colombo via Delhi.

On wide-body operations, Indigo has wet-leased 777s from Turkish Airlines. Perhaps the idea is to train their crew on it. But from the feedback I’ve seen, the experience has been extremely subpar for passengers. Since it’s a Turkish aircraft, regulatory issues have been a problem. I suspect this has been an expensive experiment too. So far, these operations have been riddled with issues. For example, flights have been downgraded to an A321 with a technical stop, and passengers on Twitter are sharing horror stories. On the brighter side, using the Turkish hub in Istanbul, Indigo is able to transit passengers to Europe and the US. The pricing has been softer, but the overall experience is not up to the mark.

While Indigo has always been cost-focused with a single aircraft type, this strategy might hurt them in the current scenario. Air India, on the other hand, has been scrambling for any available aircraft—narrow or wide-body. They’ve taken five Delta 777s, six aircraft from Etihad, six A350s from Airbus (originally destined for Aeroflot), and 55 737 MAXs that were meant for Chinese carriers. While they are still much smaller in fleet size, Air India had 55 wide-body aircraft post-privatization, offering significant international capacity. There are also rumors of Air India acquiring six 777s from their JV partner, Singapore Airlines.

In my opinion, money in Indian aviation will be made in international operations. Air India has had a massive head start in this area, while Indigo is still playing catch-up.