Great thread !

Had I not read this thread while understanding Interarch or EPACK, I would have missed so many perspectives. I think, inside the commodity business someone with a large Staying Power, Big Capacity and Design Engineering strength will become from small=>mid=>large. In my opinion as well, the valuations of 30-40x of earnings are pretty high and I will personally wait for infrastructure slowdown; giving lower growth to PEB sector and hence lower multiples to wait for an entry.

I am also assuming, what happened with RCC and Cement sector in the last decade, would also happen with PEBs in the long run, consolidation in the sector, great volume growth, might not result in equivalent revenue and profit growth, also a well diversified / distributed player with factories/assembling units would win the race as even though logistics cost might not be a great challenge (like Cement) but quick availability would give the large player/ well distributed player some edge.

pardon my ignorance/lesser knowledge.

Thank you for such an insight. I had just a small query, you said 30-40X PE is high for these companies, then what according to you shall be a reasonable PE ?

Secondly, when you say infra slowdown, can u highlight basic traits of such a slowdown, so that we can understand its actually a slowdown, because when we see private capex, it already saw a dip in fy25 (CY2024 Post- election). At that time people said that earnings of companies were not transformed into a capex of same level. Since then we have seen government has been pushing hard to revive economy ( and even capex, though indirectly) , don’t you think we can see a growth in infra in upcoming time ?

Well this was just my view, would love to hear yours.

Thank you

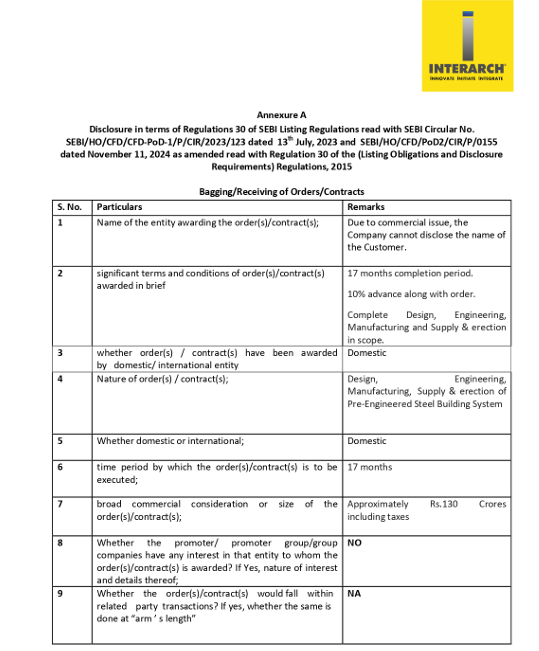

Is it common to not disclose client name?

yes. its totally as per the contract between the 2 companies.

Indian steel prices are increasing in early January 2026, driven by the government’s recent imposition of a safeguard duty (12% for the first year) on steel imports, making domestic steel more competitive and boosting producers’ margins. Will this affect interarch and other PEB companies in the long run?