Q2 FY2026 Conference call Highlights:

Investor Presentation: https://www.interarchbuildings.com/frontend/pdfs/Investor-Presentation-Q2-FY26.pdf

Conference Call Audio: https://www.interarchbuildings.com/frontend/pdfs/Earning-Cal-Q2-FY26.mp3

How Pre-engineered buildings are different than fabricator, civil contractor?

Customer only give requirements, company design and engineer it in house. It can be semiconductor plant, data centre, li-on battery plan, houses, villas, resorts, airport, Pre engineered building is industry agnostics, geographic agnostic, building agnostic.

It is offered as one lump sump price.

99% items are produced in company’s factory. Each building is unique.

Each component has to produce in factory and transported to site for joint.

It is like capital good company, company design, produce, so whole building become product that perform as intended.

Broadening presence in new age industry.

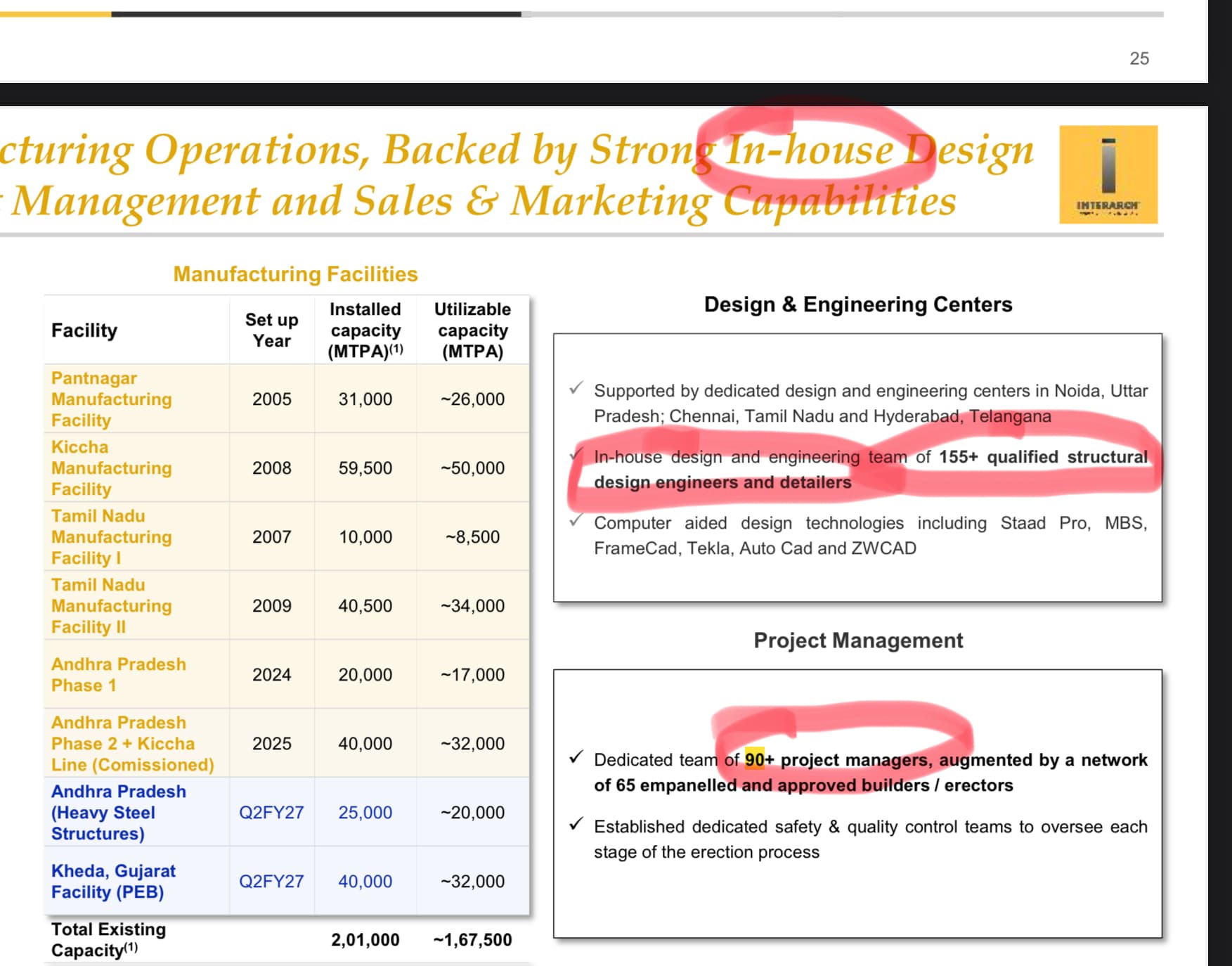

Expansion Plans:

The commissioning of Phase II at our Andhra Pradesh facility making it our fourth fully integrated PEB plant.

Total installed capacity to 2,00,000 MT.

The groundbreaking of our Gujarat facility marks another major step in our journey. this new plant will play a pivotal role in our next phase of capacity expansion and market reach. It can be built in 10 months. Asset turn is same as other plants, 6 times.

Groundbreaking at Athivaram, Andhra Pradesh for our heavy steel structures plant further consolidates Interarch’s leadership in the high-rise steel building segment.

CAPEX will 70 crores this year, 70 crores in next year.

Orderbook:

Total order book on 31 October 2025 is 1634 crores.

463 crores order between 1st August and 31st October.

80-85% repeat customers.

Orderbook shall pick up.

Guidance:

Increase from 17.5% to 20% revenue for this year. Next two years also at 20%.

EBIDTA margin shall reach at double digit. May be next year. Not happy with margin. It can be achieved by absorbing overhead cost, large orders,

Others:

Speed of executions increased. 1st Haft generally is not so fast, as it is this year.

Lot of business and lot of competition.

Adding capacity faster, but engineering, sales, marketing, payment etc also need to move faster.

With new plants, company can do 2000cr+ in revenue in 2026-2027.

Company is careful in picking orders, in prices, scheduling, quality etc.

Margin not improved due to investment in people, export planning etc. It will improve.

TAM is very high. More company comes; it is good for industry.

Volume done in Q2 is 41215 tons. Utilization capacity at 80-90% in industry. Some work done by satellite plants, based on need.

Mold-tek is collaborating on export order. No order as of now. Inquires are there.

Heavy structure unit

It is not only for high rise building, but it can also be used in power, oil & gas sector. It can be used in very heavy structure require. Margin will be at 9 to 10%, similar to pre engineered building. Turn around time is also similar to pre engineered building. Requirement for company is less in this segment. Volume is higher, but commoditized building, not niche like pre engineering building. Asset turn can be higher.

Disclosure: Invested