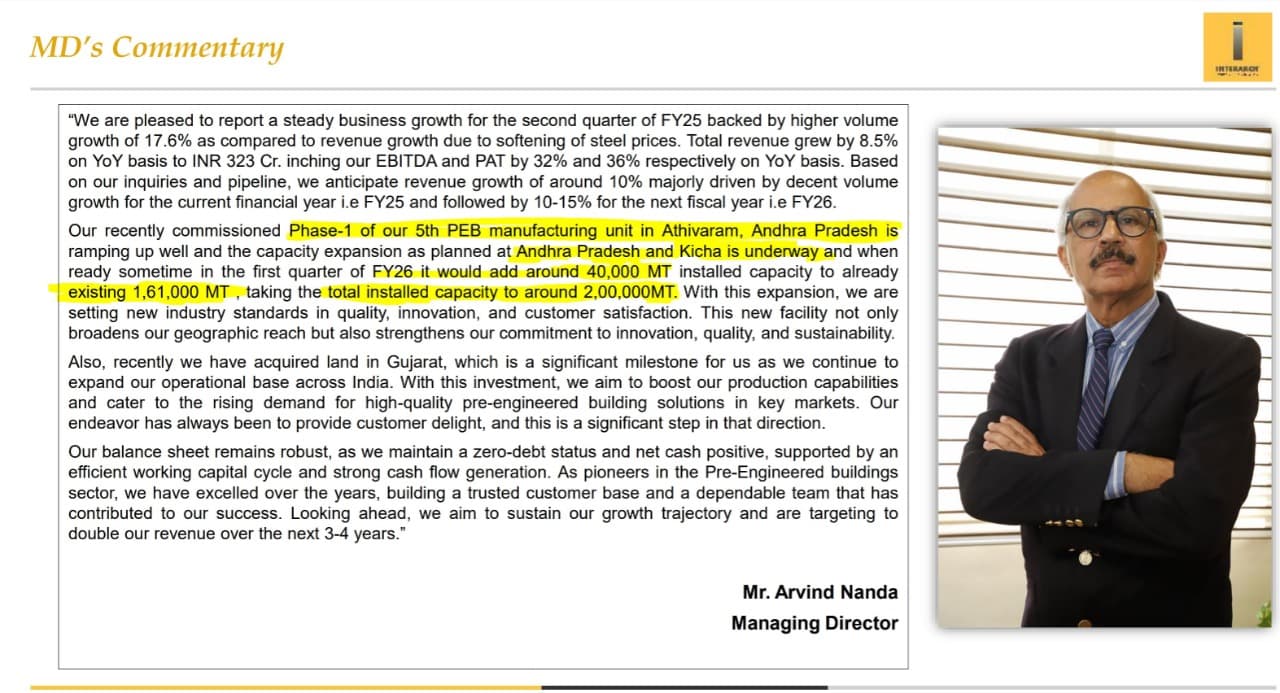

Interarch is undergoing expansion in two new facilities as well as upgradation of existing facilities + zero debt status (not so for pennar ind) + their debt to equity is going out of control (as per concall)

5 Likes

Concal Notes

Order Book

- Current Order Book: INR 1305 crores (as of January 31, 2025)

- Recent Secured Orders: INR 405 crores secured between October 28, 2024, and January 31, 2025

- Key Clients: Projects include Tata Semiconductor and Tata Agratas Energy (lithium battery plant in Gujarat), Order related to the Birla Copper project (Hindalco), Vikram Solar (currently not included in the order book)

- Over 70% of orders are repeat orders, underlining strong customer retention

Bid Pipeline

- Total Pipeline Value: Approximately INR 4000 crores

- 2500 crores already submitted (Confirmed Bids)

- 1500 crores under active bidding discussions (project in discussion)

Constraints

- Large orders that previously took 10-12 months are now expected to finish in 8-9 months

- The current ability to take on new orders is limited by the company’s execution capacity. This has led to them loosing on some orders.

- To overcome this issue, they are exploring production outsourcing to overcome in-house capacity limitations. They are partnering with companies that have spare capacity to expedite project completion.

Export

- There is an increased export focused, from completing one export building per quarter to one per month

- Emerging export markets include Africa, Sri Lanka, and Nepal and opportunities in countries seeking to reduce dependence on China. USA is also a huge opportunity.

Capex

- Greenfield Expansion (Gujarat Facility)

- Facility development to begin post-monsoon and to start operations in the third quarter of the next financial year.

- It has an estimated cost of INR 80-90 crores

- The capacity is of 40,000 MTPA and 500 crores sales

- Initial utilization estimated at 75% in the first year (ramping up to 100% subsequently)

- Brownfield Expansion

- Andhra Pradesh – Phase 2 and Kichha – Phase 3

- Anticipated to be operational in the first quarter of FY26

- Also, enhancements in existing facilities at Tamil Nadu and Pantnagar

- Current Average Order Value: INR 12 crores (up from INR 4 crores three years ago), this growth is driven by larger orders (50+ crores), which support faster business expansion

JSW Partnership

- The collaboration is with the Naveen Jindal Group, not the entirety of JSPL.

- JSPL offers advanced heavy fabrication facilities used in high-rise structures, data centers, girders, and metro/road projects.

- It is a joint marketing and bidding activities which combines Interarch’s engineering and design strengths with JSPL’s production capabilities

- The tie-up is designed to cater to contracts where 20%-30% of the building requirements are for heavy structures—such as microchip plants, data centers, or lithium battery plants.

- There is no commodity purchase arrangement between the two

Disc: Tracking very closely

3 Likes

Tracking Interarch for sometime and invested some amount but i have a few areas of concerns and would like to understand the views from fellow members

-

What is the expansion in PEB space and what percentage of that is moving into organized segment ?

-

Company has highlighted that they are not turnkey player since they also design. I dont think they are selling design as an independent service. Does it really count as differentiator and will they be able to command any premium margin ? Any other player who provide these type of consulting or high end service generally command a premium on their service.

-

Company has almost 70pc of their revenue in fixed revenue projects. I believe this exposes them to significant cost risk which may be raw material price risk or delay in execution. I understand that they do maintain inventory of 3 months to protect against price increases but average duration of mid sized project execution is around 6 months. Large size projects - they did highlight that they go for variable pricing but is it always the case since almost 50 pc of revenue is from large projects and only 30 pc of revenue is variable pricing. I see margin compression as a key possible risk

Thus i am not sure what is their exact differentiator

- Expertise : This does not seem to be the case since margin is not great and they are largely dependent on smaller size projects to build their order book.

- Cost control : This also doesnt seem to be the scenario since margin has expanded only in recent years and before this they were operating at low single digit margins.

I agree that Growth in the industry can drive their business growth and thus looking to understand the industry growth itself. Since they are big player in the segment, they will benefit from tailwinds.

Sincerely appreciate your views on growth and margin.

5 Likes

On a related note, given this is a heavily commodity-dependent business without a huge amount of technological differentiation, is the project management part of the business sufficient to create entry barriers. If not, it’s a matter of time before JSPL (for example) enters this space directly. The capacities are quite meaningful. JSPL steel capacity is 1.32 MTPA while IBL’s capacity is 300 ktpa, so almost 25%. I understand that not all the steel that JSPL produces may be of a good enough grade for PEBs, but just wanted to lay out the relative sizes for context. Since steel manufacturers go through their own cycles and pricing volatility, this will be a nice forward integration to dampen this volatility somewhat unless there is meaningful operational complexity that makes it challenging for them to enter this business.

7 Likes

Moats are not always obvious. High ROCE, ROE compared to competitors is a good indication of an existing moat. I think their design and delivery capability is a huge moat in this sort of industry.

Interarch has tons of experience in the industry, just because it got listed recently does not mean there is no track record. There are a lot of structural tailwinds. The gap between the top 3-4 players and the rest of the smaller players in terms of experience and network if clients is huge. Additionally, none of the top players are competing too heavily with each others, as there are more orders than anyone can execute.

The only reasons why this is not a mouthwatering investment idea for me is the valuation (margin of safety is a bit low) and the supply side is constrained. I am open to discussion and to change my mind.

12 Likes

Ratings update:

IMP Points:

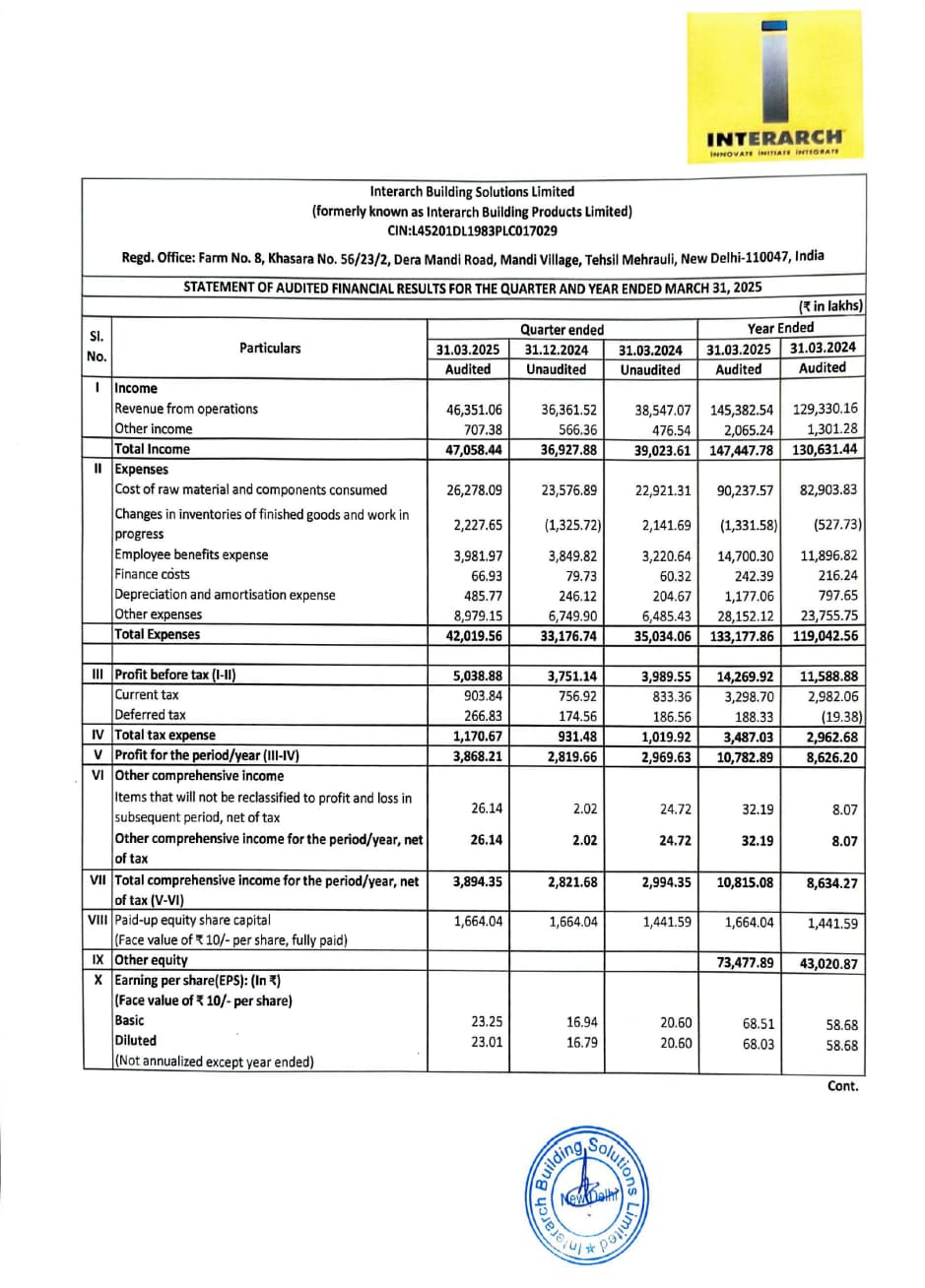

Crisil Ratings has upgraded its ratings on the bank loan facilities of Interarch Building Products Limited (IBPL) to ‘Crisil A/Stable/Crisil A1’ from 'Crisil A-/Stable/Crisil A2+’.

The upgrade in the ratings reflects improvement in the business risk profile of IBPL as witnessed in healthy revenue growth and improvement in the operating profitability in fiscal 2024 and first nine months of fiscal 2025.

The operating income grew ~15% to Rs 1,294 crore in fiscal 2024 compared to Rs 1124 crore in fiscal 2023. The revenue further improved 9.2% to Rs 990 crore in the nine months ended December 31, 2024, compared to Rs 908 crores in similar period last fiscal owing to strong order book, and better execution capabilities.

The operating margin has also improved to 9.4% in nine months ended December 31, 2024, from 8.1% in similar period last fiscal due to operating leverage benefits with increase in scale of operations.

Disc: Invested

4 Likes

Risks-

- RM volatility- Steel Prices.Steel is 60-70% of their total cost.

- Slowdown in private capex

- Competition - KP Green Engineering foray into PEB - KP PLant

- Delay in ramp up of new capacities

- Requirement of skilled manpower.

- Operating de-leverage, if revenue growth does not come, because of delay in order execution.

- The components are made off site, hence transportation and logistics are very crucial in the industry.

6 Likes

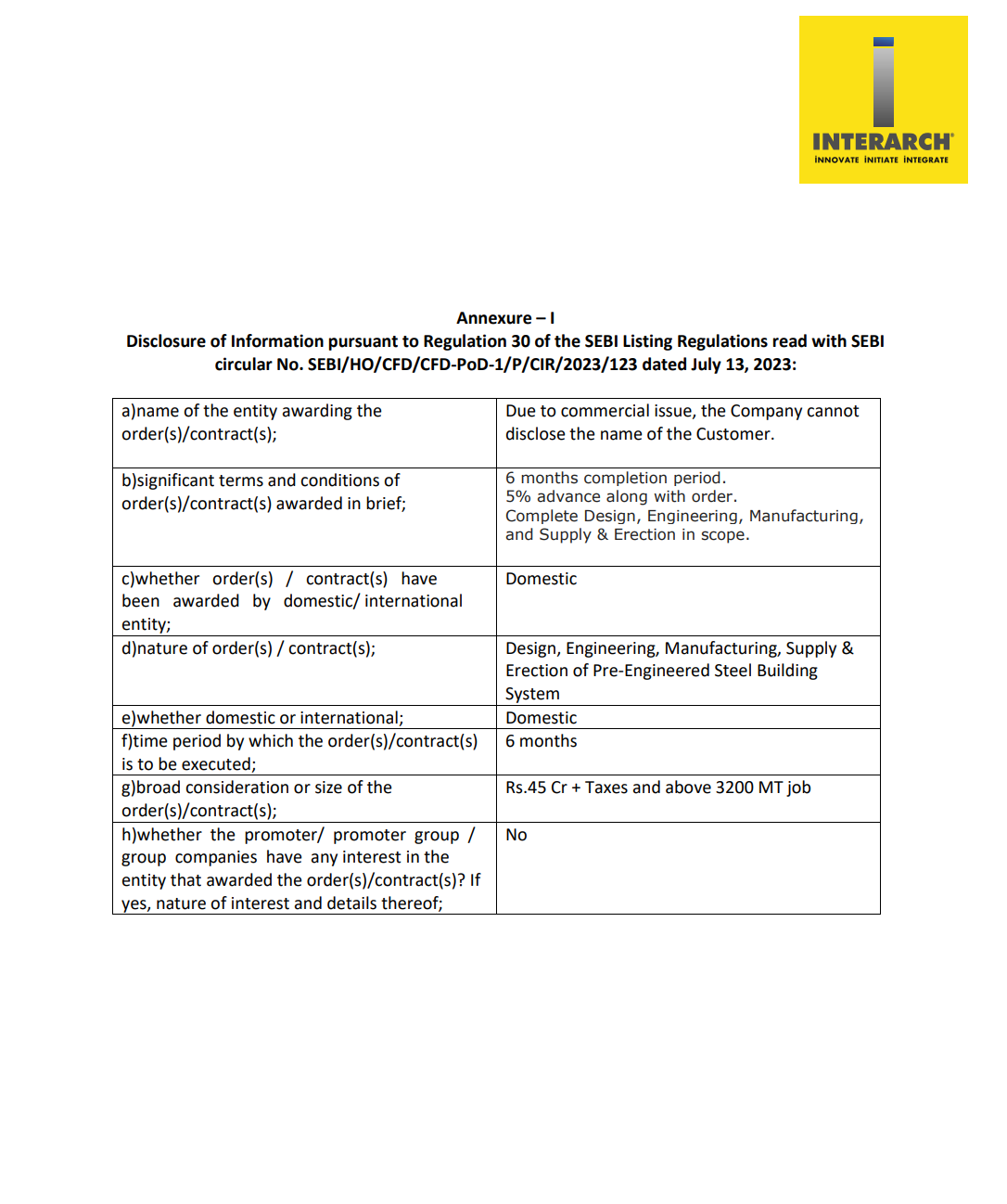

Interarch secures India’s largest ever single PEB order in public domain worth 300cr.

5 Likes

![]() Leadership Shake-up at Interarch Building

Leadership Shake-up at Interarch Building ![]()

![]() Sr. GM (Purchase) terminated – May 24

Sr. GM (Purchase) terminated – May 24

![]() VP – HR resigned – June 3

VP – HR resigned – June 3

![]() GM – EHS resigned – June 3

GM – EHS resigned – June 3

3 senior exits in 10 days.

![]() Raises serious questions on internal stability and clear red flag.

Raises serious questions on internal stability and clear red flag.

![]() Need to track closely.

Need to track closely.

10 Likes

Such a resignation letter is rare, as it openly uses strong words. But it’s good because it gives investors a clearer understanding of the real reason behind the resignation.

12 Likes

power of pre-engineered construction

5 Likes

Interach has grown from company selling false ceiling to one of the largest listed PEB Company. The major challenges facing in my opinion are the quality of the design which is required to design timely optimum structures so that they are competative in tonnage. They have tied with Mold Teck Technology for designs implying that they are feeling shortage of qualified people inhouse.

Kirby one of the unlisted companies is the biggest PEBvendor in company and has presently superior technical staff also.

The quality of steel fabrication is better in PEB and hence all larger buildings are going for PEB structures.

Interach has good leadership and they can ddeliver on promises.

They are working on exports and that may be a growth engine for future. They need to work on the design, fabrication, erection of multistoried housing to come upto the expectations.

wish them Best of luck. I am invested in the stock at 950 levels

12 Likes

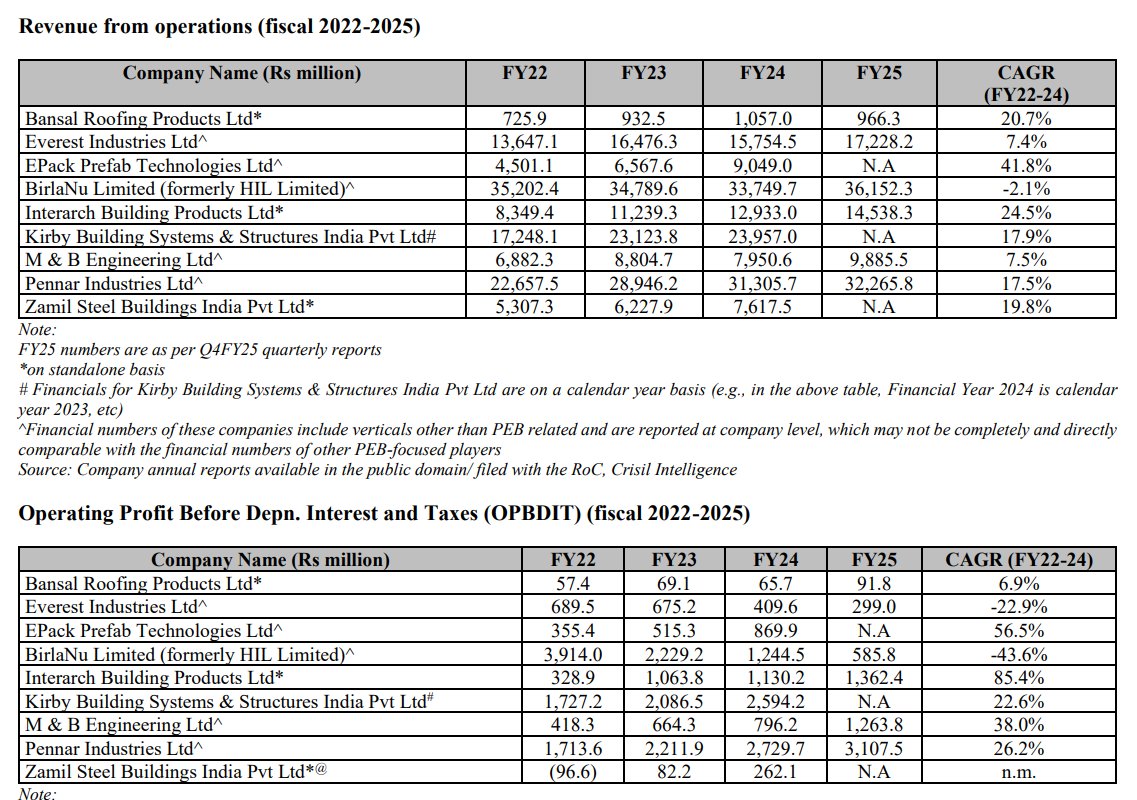

Key competitors in PEB segment:

Kirby: A foreign company from Kuwait

Zamil Steel: A competitor in the simpler building segment

M&B Engineering: Recently listed in India

Pennar: was listed then merged with parent - no longer listed (credit rating link)

Everest: Listed India, similar topline but valued at 1/3rd - interesting

Phoenix: Private player

See, our moat and our USP has always been the way we have worked with every company…The relationship, every job that we do, we concentrate fully on it, finish it to customers delight. I think that has been our moat. And that is very difficult to copy. M&B is newly listed. It is not a new company. We compete with Phoenix in many, many cases all over the country. But they have built up their own niche. Everest, I do not think has done very well. Pennar has done reasonably well, again, in its own niche… we call ourselves the Mercedes of the PEB industry… that 1s our moat…I do not have any magic formula or any magic technology in which I can say that I am ahead of these companies

8 Likes

The Income tax department has initiated a search at company’s manufacturing unit at Pantnagar and corporate office in Noida.

According to the Company, they have not received any written communication from the tax department regarding this search and company is in process to gather more information regarding the same. Company is Cooperating with the tax officials and has voluntarily made this disclosure

Interarch Building Products has good prospects with healthy orders and very good execution, thier margins are also good and are planing to expand geographical, a new plant was to be commissioned soon which would have added to thier capacities and accelerated growth.

This IT search will impact negatively to companies goodwill and growth, it will be interesting to know what the tax dept have found and to what extend and how the management is responding

Disc : Not sebi registered. This is not a buy or sell recommendation. I am invested so keeping fingers crossed ![]()

8 Likes

I hope this is another opportunity like Polycab so that i could buy some more. :)

11 Likes

Such back-to-back resignations, in quick succession (involving not just 2 but 3 people), can’t help but seem to be correlated to some underlying cause , rather than just being sheer coincidence.

Experienced boarders can please comment how to read between the lines?

Does it or does it not give an eery resemblance to all-is-not-well? Or it is merely an operational, internal stuff without no strategic ramifications?

3 Likes