Thanks for this link

It has a nice video from intellect on a lot of things.

How their products are unique - iTurmeric - a marketplace of apps (like netflix) - Composability - Low POC time (2/3) won them auto deal in germany where they beat 27 other companies including the likes of temenos.

What is coming next from them etc - w.r.t big data

Disclosure: Invested with small amount - scaling up slowly as I research more.

From magic quadrant for global retail banking report

Strengths

The Gartner Financial Rating improved from Caution to Variable in 2019.

Operations are another bright spot for Intellect, as maintenance fees are the lowest across the examined vendors in this Magic Quadrant, and minor releases (issued twice a year) consolidate patches and services packs.

Intellect Digital Core shows a greater than the average number of exposed microservices, according to the list provided to Gartner, and a moderate commitment to microservices architecture.

Cautions

Intellect Design Arena had the highest decline in overall customer experience across the examined vendors in the evaluation of 2018 through 2019 project deliveries, with a significant drop in the implementation experience.

The cloud offering is very limited for this vendor, which has previously installed its product on some private clouds and a few installations in public cloud.

Intellect’s deployment ecosystem is considered weak by Gartner. The company delivers projects largely autonomously by consultants traveling from its few hubs to clients’ sites and supports them from India.

As mentioned by @kenshin quoting from the magic quadrant for global retail banking report, isn’t the drop in customer experience a significant risk? Given that there is a lot of competition that Intellect faces across all of its product verticals, while switching costs for existing customers may not be low, a reputation of poor customer exerience can be a major hinderence for new customer aquisitions. This against the backdrop of the huge rally and reasonable valuations don’t leave much margin of safety as far as I can make out. The risk-reward doesn’t seem too favourable in comparison to other opportunities in the market for me.

Would love to hear contrary views and am happy to reconsider my thesis.

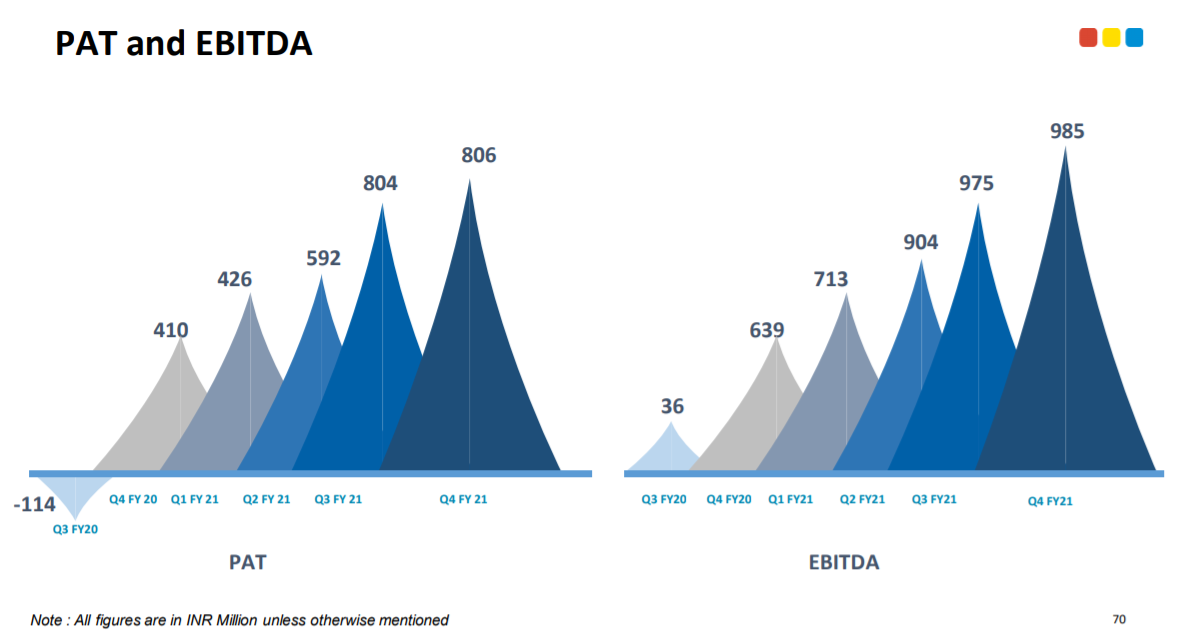

There is an 8 cr. rise in ‘other expenses’ qoq which has offset the decent revenue growth.Company has been guiding for 280-85cr. kind of quarterly costs so this is definitely a -ve surprise.Need to know what led to this and whether this is a non-recurring,one-off.Otherwise business direction remains decent.If I see brokerage reports then no one was building in such margins for FY21 so it seems like a ‘beat’ but given the run up in stock in recent weeks maybe the implicit expectation was of better margins.

I believe the recent run up was mainly because of the recent deals won by the company and the price momentum may continue in the coming days because of the exponential growth expected.

Nothing major. They are broadly in line with company guidance -

Revenue 15% - 20% growth

EBITDA - close to 30% margin

EPS - c.30% growth

For what it’s worth, they estimate Rs.700Cr of net cash by FY23 end. Assuming a 60% EBITDA to FCF conversion (this is the median for OFSS since 2015), we could be looking at FCF yield of +3% on current price levels. In addition to growth, a dividend angle also appears to be gradually developing.

In the very near term, with the stock already at 36x FY21 EPS and 28x FY22 EPS, I doubt the stock will see any dramatic moves on either side before 1Q22 results.

A Destiny Deal will give significant opportunity in terms of revenue and cross sale to IDA in that particular account. And also add as a reference point to sell their solutions in other similar customers/banks in that country.

1)that is valued 40-50 crores contract value ( on mature products like iGTB and intellect core) - this info is gleaned from conf calls over time.

Marquee customer name that is referencable to other clients

Destiny deals for different products (like SEEC vs iGTB )will be different.

Intellect follows a strategy of going after the top 2- 3 customers in their target segment . According to them if you are able to sell to them all the other customers want you too and you can get better pricing.

Long answer to a short question but I hope it helps

I don’t think anyone from India are competing with IDA (maybe TCS or Infosys has one or two products, but no where near the tech capabilities of IDA). But foreign companies like Palantir, Finastra, Mambu, Temenos etc., are their competitors.