Is ofss not their competitor? It operates in a similar space.

1 Like

List of competitors for each of its products. From a twitter link shared by one of the posters above

That thread has more info.

8 Likes

6 Likes

Annual report - https://www.bseindia.com/xml-data/corpfiling/AttachLive/81b3065d-cb0a-4e12-9352-20423f3a9312.pdf

1 Like

This insider trade case seems to have closed now.

In summary, Aarushi will have to pay ₹40.93 lakh, which included ₹22.31 lakh as settlement, ₹13.78 lakh as disgorgement of alleged ill-gotten gains along with interest of ₹4.84 lakh. Arun Jain has agreed to pay ₹1.35 crore. Both had filed separate settlement applications in terms of the SEBI proposing to settle, without admitting or denying the findings of fact and conclusions of law, through a settlement order.

Disc: - Invested & Biased

8 Likes

Webinar: Safeguard your customers’ Aadhaar data and your business, with Magic Aadhaar

4 Likes

Q1 Results news share

1 Like

Another quarter of sequential EBITDA margin contraction.

Not good.

Best case scenario, stock remains rangebound for 3 more months until 2Q results. Worst case scenario, stock starts to de-rate.

Management just cant seem to deliver on predictability.

4 Likes

So, downward reset to targets. Who would have thought that would happen in the midst of all this digital hype.

30% EBITDA margins by FY22 end is out. 30% EPS CAGR is out (25%-30% range now).

They were honest enough to admit that the hit to margins is from employee cost. Attrition has shot up last quarter.

Management also tried to spin the lower margins as a trade off between profitability and growth. But that is not really true because revenue guidance remains at mid to high teens.

On a Rs.25 EPS for FY22, the stock is trading on 30x P/E. I wonder what the right multiple should be.

2 Likes

Currently attending the Concall(its at the tail end right now so I’m just penning my thoughts).

To start with this is one of the best Concalls I’ve ever attended. Hopefully more and more companies shift to zoom. The presentation was fantastic and the Q&A was smooth and it feels more like a full on analysts meet rather than a normal concall. The presentation being used is published on bse… I think its too big to upload here so downloading it from bse would be the best option.

Management spoke for 35 minutes using the ppt and gave clear drivers for growth(this is the first time I can remember where their entire strategy has been fully laid out) and explained the financials perfectly. All of this is covered in the presentation for anyones perusal. The Q&A made me realise that this is a company that investors yet don’t understand and showed the confidence of the management. They answered every question asked(even some hilarious ones) and even extended the Concall.

Anyway,

In short… Don’t expect steady growth every quarter. The business can be lumpy due to deal signings taking even upto 18 months to complete. However YOY is how to compare it and they are confident of atleast 20 percent growth YOY or atleast mid to high teens. Ebidta margins long term should be 30 percent but currently expect 25 percent during this growth phase. One of the main issues is predictability of revenue… Well, license linked revenue is now 58 percent up from 50 percent. They are targeting atleast 60 percent and this will give quality revenue growth and more predictability and gross margins can even go upto 60 percent from current 56. Saas has doubled this quarter too. Eps growth is projected to be 30 percent for next 3 years but don’t expect it every quarter and exactly within 12 months since deals get delayed etc. A few more destiny deal wins and this can happen even earlier in a year(and they’ve won some pretty impressive deals this quarter). Attrition has increased but at the same time they have increased hiring and are building bench strength now too. So overall, the gradient will continue upwards for the next 3+years but it won’t be in a straight line. For eg Some long term projects needs investment upfront which will show a loss in a quarter but will provide steady revenues for a decade. They can’t make projections and guidance and have to readjust due to the inherent deal like nature of the business. Hence this business may not be for everyone in its Current form(as license linked revenues and destiny deals ramp up there should be more predictability soon enough )

Side note: The JV that led to a loss this quarter will show profits last 2 quarters of this fiscal. Tax now at 16 to 18 percent rate. No need for m and a and dividends at present with such huge growth opportunities. Rise in other income was due to sale of unused flats.

Also, Mr arun jain also answered the question about insider trading directly at the end! I am convinced with the answer but il leave that upto each one to decide after listening to it

Overall I’m seeing a clear disconnect between the understanding of the company by the investors in the call vs the confidence of the management(similar to what one may see in a complex company like deepak Nitrite) and it may take a few more quarters for people to get convinced regards the predictability and trajectory and quality of the growth and feels like a company that is still in flux and is about to hit its stride.

Disc: Invested since lower levels. Added more Today post results in the crash and will add even more next few weeks if the opportunity presents itself again. Not a sebi advisor.

Note: watch the conference call recording for your self once out and don’t rely on my random summary on a forum since I am biased as an investor and have my own level of conviction. I’m assuming this result and the business model in general will lead to a lot of conflicting opinions amongst Investors so its better to build one’s own conviction.

20 Likes

Thanks for for the summary.

I think the disconnect is due to the fact that Intellect is not a ‘IT-Services’ company but a Product company. IT services is more linear hence easy to make longer term projections. In the case of product companies, license/deployment/professional services drives the revenue, while licensing revenue itself may repeat yearly but the other type of revenues are one-time in nature and can create bumps. The larger strategy of intellect is to increase the SaaS component, I see the SaaS revenue is almost similar to License revenue in Q1 FY22 (in contrast license used be 2x of SaaS in Q1 FY21), this is very encouraging.

Disclosure: Invested

6 Likes

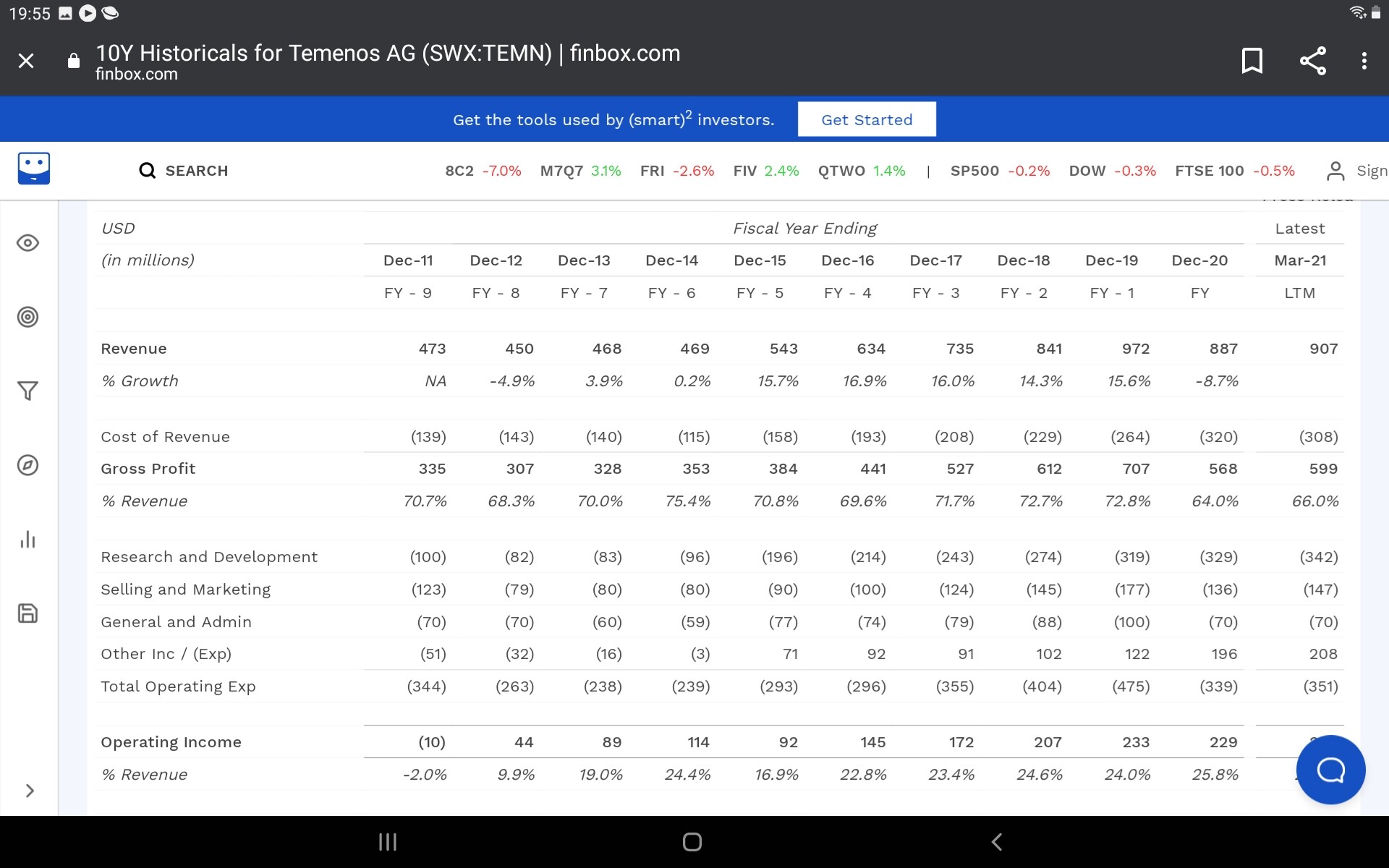

Temenos growth story( which Intellect compares as key competition) -

What it tells us is

- leader in space - Tamenos also grows at mid to high teen rate, FY21/22 may have some spikes with Digital push due to covid but sustainable rates seems mid teens over last many years - what Intellect has been guiding out too even at a lower base - can potentially do higher growth

- EBDITA margins in last few years for Tenemos have been in and around 25% over last few years, given they have base in developed countries hence higher cost base, ideally an India base player should deliver much higher margins given cost arbitrage - interesting that Intellect has suggested similar type 25% margins in near future, down from 30% earlier), suggests undercutting price is key lever for Intellect to win

Con call qualitative insights

-

$50M run rate per quarter/ $200M is what current organization structure can support/deliver, they are currently pursuing two $50M+ deals but feels organization size need to be around $400M and dedicated management bandwidth to close out such deals - rightly so, reputed financial institutions for larger mandate will look at history/balance sheet size/leadership commitment etc.

-

They can continue to deliver 15% revenue, slightly higher profit/EPS (20%+) growth rate at sub 30% type EBDITA over near term

-

Management team is seasoned ( most came with IT service legacy)with most of folks in 50+ age bracket, smart and risk taker - Arun deserves credits for building a pure play product otganization with aggressive investment required in initial few years, they will need next set of leaders sooner than later to drive Intellect 3.0 - this could be WIP but not reflected in call

-

SaaS product organization are highly valued anywhere between 10X to 20X sales but need to demonstrate high growth rates

-

Valuations- FY 22 they are likely going to do a 1800 -1900 cr revenue, about 300 - 320 cr profits- half of this is SaaS/license revenue( sticky and long term visibility) - Tamenos is valued at 12X revenue and 60+PE with similar growth and margin trajectory ( but has a longer history and much larger scale of operations)

-

Arun did mention on call about interest from institutional investors from Japan and EU, as well some of existing institutional investors suggesting accelerate growth even at cost of lower EBDITA - however they do not want to take eyes off from profitability thus 25% EBDITA stays intact

-

Valuations has potential to catch up with Tamenos eventually with consistent performance, need some more marquee global investors coming on board - Ironic that FII hold near 28%+ ( increasing consistently) and DII hardly at 2%( decreasing consistently) in a true product DNA organization from India with global success and local funds not keen on it

Invested and adding

8 Likes

expect the company to post 19-20 per topline growth overall… expecting 85-87 crs pat for q2…full year pat growth of 25 per at around 330 crores. average ebitda margin of around 26-26.5 per for the full year.

3 Likes

Best case for intellect for fy22-

Topline - 240.7 million dollars

Ebitda margin ( excluding other income ) - 25.5 per

Ebitda - 454 crs ( dollar rupee at 74 )

Other income - 16 crs q1 plus assuming 15 crs in total for next three quarters equals 31 crs

Share of jv profit net of tax - 9 crs ( same as fy21)

Dep- 100 crs for the full year

Pbt - 385 crs

Tax rate - 17 per

Pat excluding jv- 320 crs

Total pat - 329 crs (26 per eps growth over last year )

3 Likes

Hi, can anyone please guide me to some source where I can learn more about Intellect’s products. I am trying to understand the products from a user’s point-of-view, that is to say what is the use case of their products or what problems are they solving. I have gone through Intellect’s reports and website, but they are just filled with jargon words (and same is true for Temenos as well). I just want to get a feel of what these products actually do (I want to go a level deeper than “With a rich suite of transaction banking products, we are an authority on vertical and integrated products that enable banks to meet their ambition to be the Principal Banker to their corporate customers”), and have been struggling to find resources.

Any guidance as to how to go about it will be appreciated.

3 Likes

2 Likes

Quick notes I had captured while attending the IDA conf call. management body language was positive as usual, but they have always been on the more optimistic side, and in the past also we have seen investors getting too gung ho based on management projections.

Highlights I captured from the Conf call

1. License growth - Licenses are now 58 % of revenue now compared to 50 % last year. It will be lumpy given the elongated sales cycle, and big deals.

-

Sales Cycle- takes 18 Months to close a deal, 14 signatures -

Implementations - Faster ~ 4 months compared to 12-16 months earlier due to Remote, Agile methodology. Win rates are high once we reach POC stage. Margins on Implementations are 20-25 %, sometimes up to 35 % too. Revenue recognition is on phase completion. -

Geos- One Win in Canada, nothing in US this qtr. Canada seeing significant traction and getting market leadership there now for Transaction Banking, like Middle East earlier.Making Product investments in Islamic banking. Europe- Targeting iKredit360 for BNPL kind of flows. Setup of Cloud offering via AWS Germany and Azure. India- GEM is profitable, but DSO's are high, looking to reduce that. -

Product- CBX- headless solution, with end customer/ SI partner defining the User Interface and IDA providing the core flow -

Outlook - Revenue: expect Mid-high teens revenue growth in coming year, earlier targeting 20 % -

Outlook - EBITDA expect 25 - 30 % , earlier were guiding for 30 %, largely driven by increase in Employee salaries, Attrition increased substantially in last quarter, hiring for replacement, plus increasing headcount. -

Growth vs Profitability- Strive for a balance, dont want to let go of growth opportunity in trying to get to the 30 % EBITDA margin -

Cloud Revenue - currently 16 %, target 25 % -

Three year outlook- Still target 20 % revenue growth and 30 % Earnings growth -

Outlook- Tax- Expect tax rates to increase as profitability grows and the old losses get wiped out - Expect 16-18 this year % -

Dividend policy- No tangible plans yet, board will consider -

Competition- Temenos is very strong in Legacy, not agile in new opportunities. Architecture/New technology is a differentiator for IDA. We are winning against them in Europe in some deals. OFSS- is there in some deals as competitor. Mambu- face them in Digital Banking. -

Large Deals of 50 Mn + : Have two pursuits currently, may look at IBM partnership to drive it. -

Implementation partners: Not yet, want to retain customer ownership. Partnering for selling. Looking for partners for the Composable flow. Eg Otto germany was Partner driven. CBX deals would be primarily partner driven. -

Investor outreach- Speaking to Japanese and European investors -

Insider Trading Fine- Arun Gifted shares to his daughter of 100 K shares via his family office, on the same day the IBM alliance was announced, it did not have any major material impact on the business in the near future ,this was one of 50 announcements. SEBI took it as insider trading due to 5 % increase the same day. Decided to settle, instead of litigation. Arun has never sold any shares in the last 30 years.

Disc: Invested from before the Polaris demerger, holding and adding whenever valuations look reasonable. This product story still has a long runway ahead. But like any product journey, this will have a lot of speed bumps.

13 Likes

I did back-of-the-envelope revenue (2020/21) per employee comparison for IDA with Mastek (more or less is similar size). How come a service company fairs better than IDA which being a product-centric company, should be showing some non-linear growth?

| IDA | MASTEK | |

|---|---|---|

| # of Emplyees | 4260 | 3792 |

| Sales (in Crs) | 1497 | 1722 |

| Revenue (in Cr.) /Employee | 0.35 | 0.45 |

1 Like

My thinking is as follows:

- Intellect does a lot of services work as well - for eg implementation and annual maintenance

- With scale, Rev / employee should become even better. At the end of FY16, they had 4k employees - so # employees has remained flattish. Revenue has grown from INR 900 Cr in FY17 to current run rate of ~INR 1,600 Cr.

2 Likes