Very detailed analysis and many thanks for the same. If I may add a few more thoughts - would be great to get any thoughts you may have on this

a. The exciting part of the business is that it has an increasing share of revenues from predictable revenues (SaaS or AMC). However, the growth driver for the business is new business - either through license revenues or new SaaS contracts (which then converts to predictable revenues). While they described the new growth areas in their Technology Day, I am not competent enough to understand whether this can translate to the required growth in license revenues over time and have to rely on the managements view of low teen revenue growth

b. The one additional area that gives comfort is that as per the annual report, Arun Jain does not take a salary - and his ‘remuneration’ is based on share price appreciation - therefore our interests are aligned. He also seems to have a very long track record in Banking product development - so credentials are strong.

I went through their insurance product(Fabric) technical architecture . Their architecture is at par with industry standards. Goes on to show that their technical talent pool is good.

One of the risk ( IDA themselves has called out as well)that seems to be playing out is much higher growth in subscription deals and slower than anticipated growth in license/on-premise deals.( e.g. Concerta deal as well)

While there is a possible impact in short term( QoQ sales growth) but solid for long term ( stickiness, long duration contracts, higher margins…) and most of All higher valuations in line with product and SaaS organizations. (20X sales being a yardstick for pure play SaaS),

the way New deals are being won, subscription model will likely become larger pie , especially post covid era demand scenarios.

Out of YTD 1100 cr revenue, YTD revenue split Licence 250Cr, AMC 210 cr , SaaS 115 cr.( close to 60%), rest will be services which will be lower margin.

Fy22 they will likely do 2000cr+ revenue, 30%+ ebidta and as explained by them cost being relatively constant nowin Q3 at 280 cr/ Qtr I.e 1200 cr for fy22, PAT will be 500 cr+, has some serious re rating potential.

Winning against global biggies is definitely a testimony to their product capabilities.

a) Yes, agree license revenue growth is harder to predict and can be more volatile especially if one looks on a quarterly basis. In general what we can see is that licese based deals are getting larger. Co has been able to win larger deals. Other than iGTB, iGCB business unit should be able to give a mix of license deals and subscription. I do understand that there is a risk of license based deals getting substituted by SAAS based but if that happens that will create a good long term predictability. Also, as far as numbers are concerned, I am not building a high license revenue growth. For ex in the base case for next 3 years, I have only built a 12% CAGR on license revenue growth. Much of the growth I expect to come from AMC and SAAS. In last 3 years, license based revenue has grown by 16% CAGR. So there is some conservatism in the numbers. I dont mind being deliberately conservative on items where predictability is less as when I see valuations are reasonable on my conservative numbers, I am able to average up with more conviction if I see qualitative factors improving.

b. Agree with your point on credentials. That is one point I highlight in my notes. This was an observation at the time of first buying. Based on their track record in financial domain, the management has the DNA of coming up with software products in BFSI.

GTB is probably around 2/3rd of total revenue. In the Zee Business interview above, Arun Jain suggests 12% - 18% revenue CAGR for this vertical.

Against this backdrop it is very difficult to model 30% type of topline growth profile for the company. With the kind of commentary we have from management, I think 20% type growth is more realistic for the topline.

Agree on possibilities around top line growth in mid teens for short term, however with operating leverage bottomline will deliver meaningful expansion ( 30% EPS growth mgmt themselves have called out for). TTM EPS is around 17 and a 30% on top of it( although I believe they will deliver better with higher deal conversion and demand than anticipated), A 24+ EPS range is very likely.

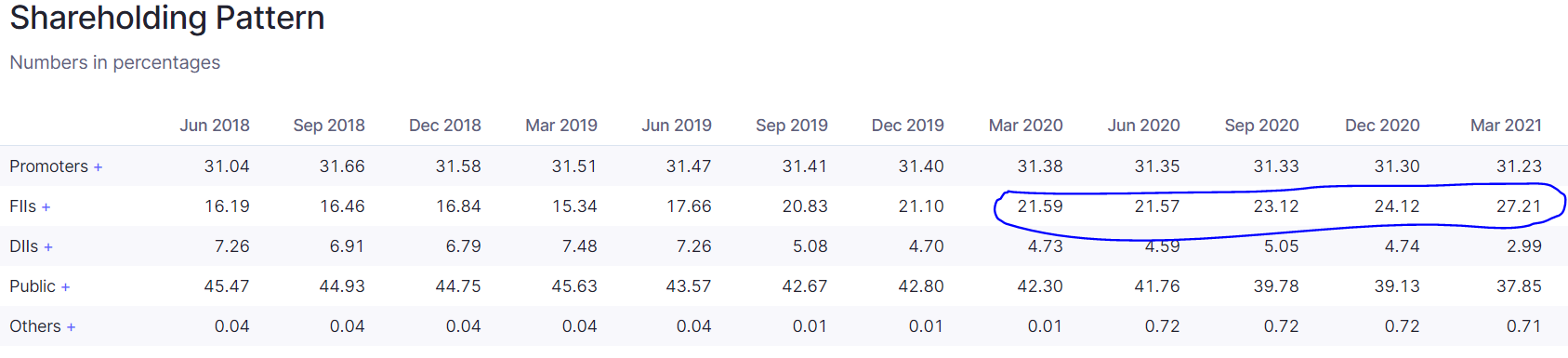

Markets are usually forward looking and this sector has tailwind, and a mid teen top line and 2 times bottomline growth , healthy OCF and operating leverage visibility, good pipeline and strong mgmt team, no of levers at play to help in rerating. If we see FII stake over last 3 Qtrs, marquee names continue to increase position.

Am being optimistic, let’s see trajectory over next 1-2 Qtrs.

NOVARICA FEATURES INTELLECT SEEC’S MAGIC SUBMISSIONS - A HYPER-AUTOMATION AI DATA EXTRACTION PLATFORM AMONG PROMINENT PROVIDERS OF INTELLIGENT TEXT INGESTION (ITI) TOOLS.

Dear Sirs,

Sub: Media Release - Intellect bags a large destiny deal win.

SocieteGenerale chooses iGTB for its world-leading Liquidity Management System (LMS). Intellect Global Transaction Banking (iGTB), the transaction banking specialist from Intellect Design Arena Limited, ranked #1 in the world for Transaction Banking by IBS Intelligence, today announced it will support SocieteGenerale, a major player in the economy for over 150 years, supporting 29 million clients every day with 138,000 staff in 62 countries, in implementing the world’s #1 Liquidity Management solution.

While 2020 was a year of great resilience, it has highlighted the urgent need for banks to deliver to their corporate clients significantly increased sophistication in corporate Treasury and Liquidity Management through automation and digitalisation. New capabilities are required to meet the combined challenges presented by negative interest rates, restrictions on cross-currency and cross-border cash pooling, increasing expectations for self-service and delivering cross-functional efficiencies to corporate treasurers. At the same time, financial institutions have been carefully shoring up balance sheets and driving operational efficiencies to ensure appropriate levels of strength to contend with an uncertain economic environment. In this context, SocieteGenerale has chosen Intellect iGTB for its world-leading Liquidity Management System (LMS). Please find enclosed herewith a copy of proposed Media Release dated 3 rd May, 2021 titled as, “Intellect Global Transaction Banking (iGTB) brings SocieteGenerale new solutions to help its clients optimise their Liquidity Management”.

Market is awaiting for guidance like how much revenue will generate. What would be the margin and duration of contract and all that.

Intellect is ticking all ticks for being a multibagger.

I am seriously considering adding to my position.