Should we assume that this merger is not happening? Inox wind issued a 3:1 bonus while the amalgamation scheme was ongoing and stayed mum on how it would affect the proposed swap ratio of 158:10. Wouldn’t promoters take advantage of the arbitrage instead of sale of equity shares via block deals?

I don’t see a reason why merger ratio wouldn’t change proportionally. Sure a communication would have helped but I wouldn’t worry much about it.

1 Like

The merger ratio will be adjusted by taking into account, the bonus shares. Please see the attached communication. The revised ratio is 632 shares of Inox Wind for 10 shares of Inox Wind energy limited.

Inox wind bonus announcement.pdf (821.5 KB)

2 Likes

There is an arbitrage of around 33% at Cmp between Inox wind and Iwel. Wondering why would someone buy Inox wind at cmp rather than Iwel. Is it market thinks that merger might not go through Or its a futuristic event and hence not certain which is leading retail, institutions to still buy Inox wind and NOT Iwel

Well the aelrbitage has ranged from 30% - 60% so definitely on the lower end now. I myself have asked this question many times. I think one thing is that liquidity in IWEL is much lower, so if there is an adverse event, big players won’t be able to exit on account of lower circuits. Other thing is that merger is still maybe 2 quarters away at least so may take time. There is no question on merger itself from company’s pov and the nclt process is continuing.

2 Likes

Have the given any timeline for when the merger will happen?

Last i heard, mgmt said they should do it by March '24 but we are way past that. Are they just waiting for the nod to go ahead or is it some other hiccup?

The long-term aim is make Inox GFL renewable arm a $10Billion company(i think it might includes unlisted companies also) as they see huge order visibility and sector tailwinds. Devansh Jain

2 Likes

Share holders approval was done on 1st of June-2024. secured creditors, debenture holders and unsecured creditors approvals were also done. It looks like merger is not very far.

2 Likes

Inox Wind secures large wind energy order.

Inox Wind has won a significant 201 MW wind turbine order from Integrum Energy. This order includes the supply of 3 MW wind turbines and subsequent long-term maintenance services. The project will be spread across multiple Indian states.

2 Likes

Q1FY25 quarter conf call was very interesting for me.

A few key takeaways from the conf call, from my perspective:

-

Infusion of 900 crores by IW Energy Ltd. = parent company. Makes company net cash +ve.

-

(Tender) Tariffs have been healthy and quantitative ranging between:

a. INR 3.4 to INR3.5 per unit for central sector wind solar hybrid project,

b. INR 3.6 to INR3.68 for plain vanilla wind

c. around INR 5 per unit for FDRE -

Lease on a rental basis for Nacelle hub manufacturing in Ahmedabad. Cost = 4 crores per annum. Substantial savings on Capex. No capex and only minimal rental payments.

-

Current year execution target is 800 MW for current year and next year is 1200 MW (might revise upwards too).

-

- No changes for FY25 guidance wise.

-

- FY26 might see margin improvements due to cost optimization, operating leverage, a better product mix & no finance cost.

a. From Q2 onwards, if you see, so we will have interest earnings (on the cash balance which we have in our balance sheet today) also, which will negate the interest expenses. So, we’ll have a negligible interest outgo from Q2 onwards.

b. Tax loss carry forward: So, FY’25 and '26, we’ll be actually paying no taxes on our profits.

- FY26 might see margin improvements due to cost optimization, operating leverage, a better product mix & no finance cost.

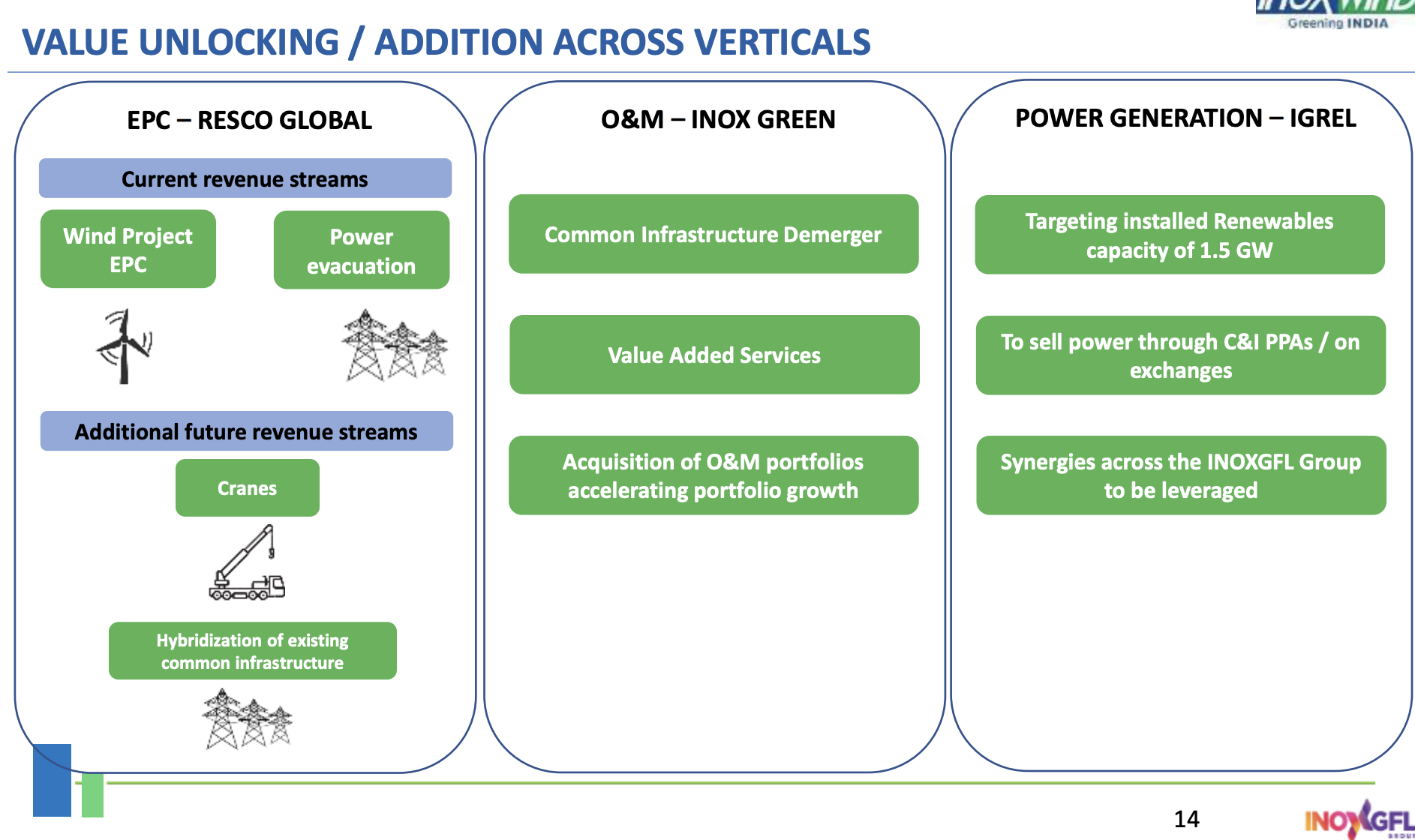

Demerger/ Spinoff:

We are evaluating value unlocking through our EPC arm and also value enhancement through our hybridization of the existing common infrastructure.

Per mgmt, given the multi decadal opportunity ahead:

- at RESCO, it plans to hybridize the common infrastructure like Wind Project EPC, the power evacuation like the substations.

- “backward integrating” - we are getting our own cranes. The returns are phenomenal (30%+)

- (what)we are now doing is given the massive multi-decade opportunity we have ahead of us. We are if I may say so backward integrating into capturing more value within the EPC arm. So we are getting our own cranes. The returns are phenomenal. The payback periods are phenomenal. We are evaluating various other assets to be added within the EPC arm where returns are phenomenal. For example, we buy transformers, our transformers and cable procurement is almost INR400 crores to INR500 crores in a year, given the run rate which we would be on in the coming financial year. We are evaluating whether it makes sense to buy out some of these things to get into it, to manufacture that in-house. Cranes, as I mentioned, is one key area we are anyways moving into internally

- I think we sit on over 5 gigawatts of project site inventory and land bank, which frankly is not given any due importance of value in reality terms, and that’s worth a few couple of INR1000 crores, honestly. So by shunting out the power evacuation from INOX Green, not only do we make the INOX Green balance sheet very light and eliminate the depreciation line, which impacts profitability. But by merging that into the Resco, which is our EPC arm, it leads to automatic listing and creating tremendous incremental value for the larger Inox Wind group. Of course, it’s subject to board approval, but that’s what we are thinking of.

- The company is planning to provide crane services to their existing EPC clients and also rent them to 3rd parties.

7 Likes

Great results and guidance from INOX Wind. One thing that concerns me is the equity dilution that will happen when IWEL merger happens. From ~28K MCap to ~40K Cr MCap - has someone done a scenario analysis based on that?

I’m holding IWL stock and the stocks were bought more than a year ago, but after bonus 3:1, my 75% stock shows holding period is 88 days. If I sell stocks now do i need to pay STGC for bonus stocks ? If that is the case , Why bonus considered as good if it actually loss for share holders if they need to pay STGC for longterm holding stock ?

yes, as per my understanding, you will have to pay Short term Capital gains tax on it.

In my opinion (I might be wrong) you received the bonus shares/dividends at a later point in time. imagine if you owned the stock from 2010, as you get dividends every year, you will get taxed for that based on the year of receipt. it does not mean that its* long-term holding so you* will not be charged taxes (hypothetically)… similarly, bonus shares, will be treated based on the year of receipt.

Thus, if you received bonus shares or the company underwent a stock split, the holding period for these new shares starts from the date of the bonus or split allocation. If you sell them within 12 months, they will be subject to STCG tax, even if your original shares were held under the long-term category.

1 Like

makes sense, thanks much Ganesh for the details.

Recent interview of Devansh Jain with ET Now:

Parts pertaining to INOX WIND:

- Inox wind, just started. Planning much larger things - ambitions are larger - we are backward integrating.

-

- even for low lying products, incrementally we easily add a 100 cr of profitability (bottom line) and can take margins beyond our stated 15-16%.

- We don’t like debt.; averse to debt. If we need to scale biz and have working capital, happy to take a bit of short-term debt.

- Interested in only niche biz which can run on high margin biz. they can be low on top line but can add strongly to the bottom line and Strong Cash flows.

- at Inox wind, a 2 GW run rate will be a ~14000 Cr revenue (15% margins = 2100 Cr)

- family office owned IPP (Independent Power producer) - IGREL(?) renewables. - next 2 years - 1 billion USD worth unlocking possible, will be the fastest.

-

- initially thought only for captive consumption. then thought why not set up and use for us and sell to various customers too.

- in Inox wind: we transitioned to the 3.3 MW turbine within 2 quarters.

- 3.3 and 4 MW are going to be the tech for the next decade in Wind turbines, for India.

GFL:

- GFCL EV is going to be the biggest among the group.

- Battery chemicals: GFCL EV will be another value unlocking potential along with Green Hydrogen.

- lot of global investors are approaching only for this EV pie. Financial investors want to get a piece of this pie. They are not looking for technology. We have the technology tie ups already in place and have been silently executing on this, for past few years.

4 Likes

Considering the date of the merger (Nov-Dec), there is a gap of 10-11% between IWEL and InoxWind.

As a strategy, can we switch more towards IWEL until the merger?

Maybe 75:25. Current allocation is 40:60 (IWEL:Inox)

1 Like

LTP on friday (NSE)- INOXWIND - 221, IWEL- 12016

Value of 632 INOXWIND = 139672, (Ratio of 632:10)

Correct me if i am wrong, if u invest 120160 in IWEL, u get 139672 in INOXWIND, which is upside of 16.23%

1 Like

Don’t expect the gap to go below 10% for long. There isn’t much arbitrage left IMO. This is because after the merger, credit of shares of Inox Wind to IWEL holders and their subsequent listing will take at least a month. During this period, you won’t be able to sell your shares even if there is a market fall. This lack of liquidity will be compensated by a slight arbitrage in IWEL shares on the merger date. Same happened in previous mergers like Equitas.

4 Likes

True, but you won’t be able to make the entire 16% hence I took 10-11%

any reason for that? is it LTCG u taking into account?