Combined marketcap post merger will be sum of the marketcap of two companies i.e. 33k + 15k= 48 K CR (as of today)?

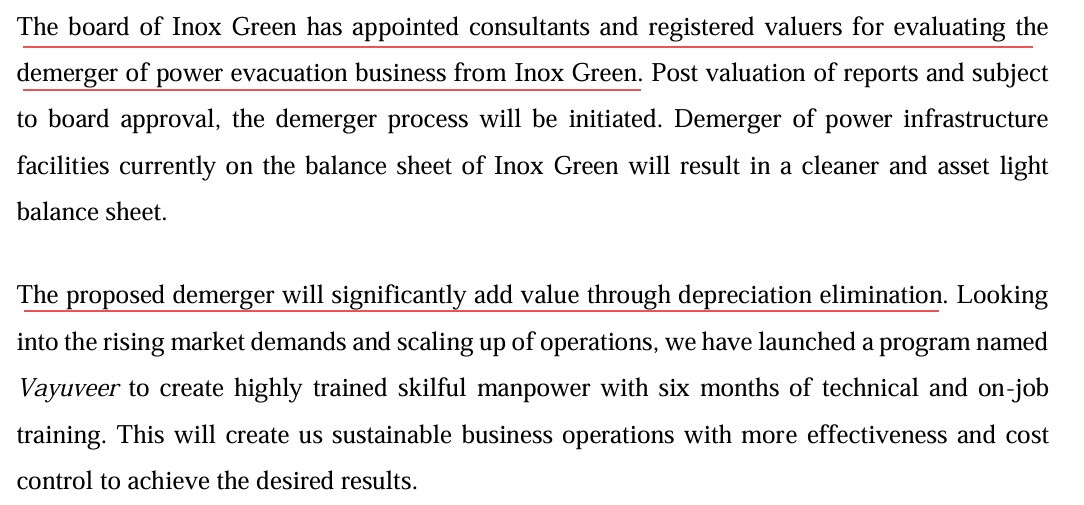

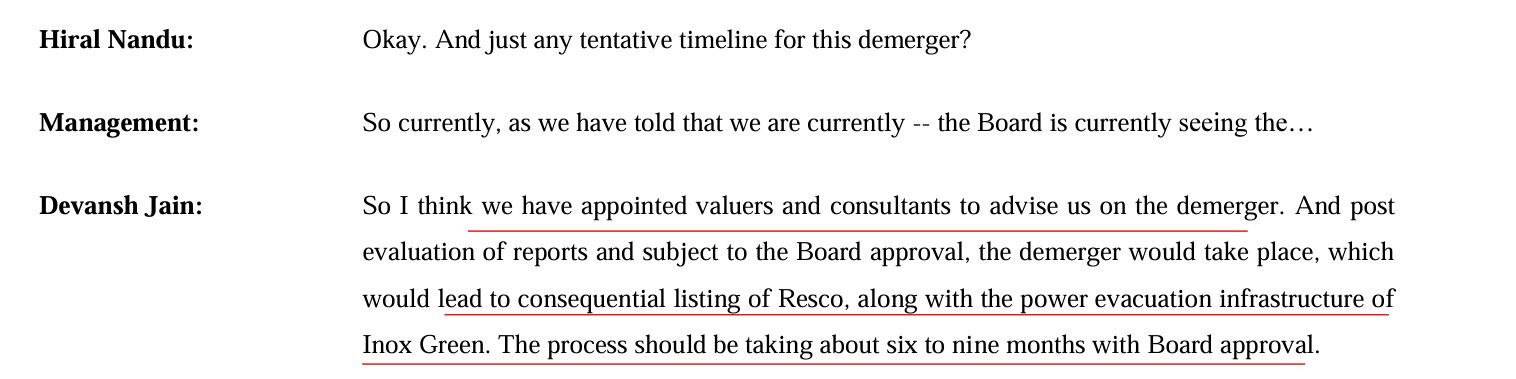

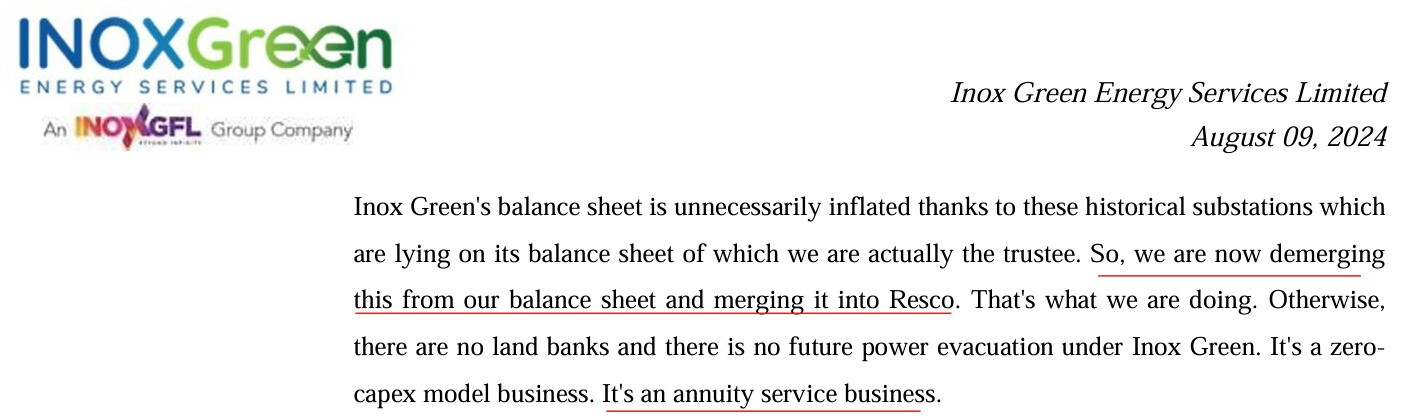

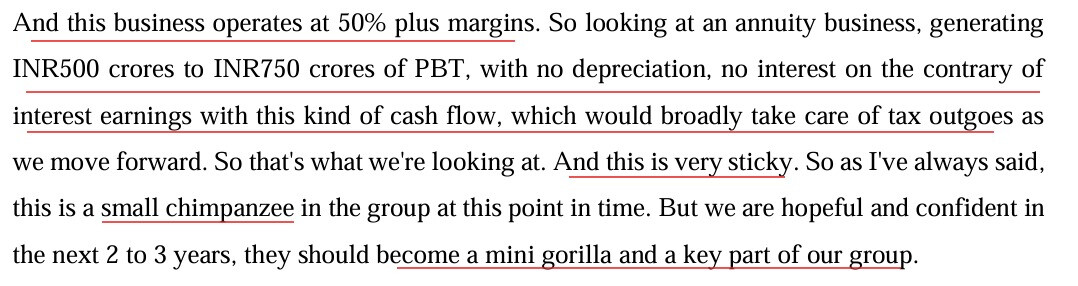

Sharing some snippets from Inox Green Con - call. Listing of Resco seems a certainty which can clean up balance sheet for Inox green making it a cash generating annuity biz with 50%+ margins. Sharing some notes for you all

2 Likes

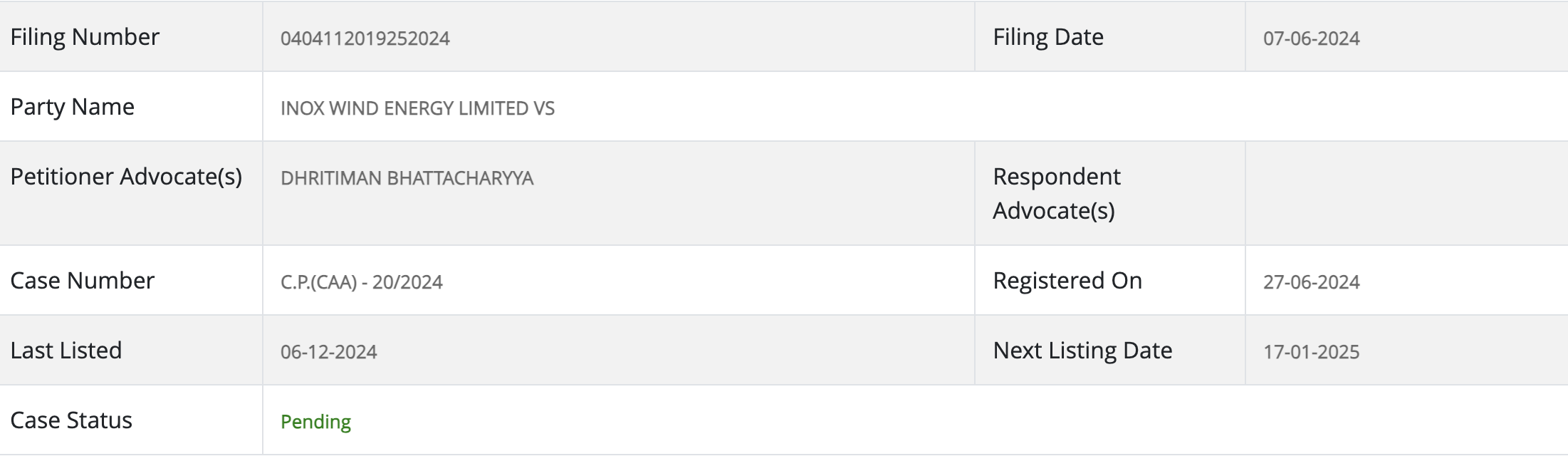

Any guidance from mgmt for the merger?

They had said Dec, but haven’t received any intimation yet.

1 Like

Nclt hearing was supposed to be on 6th December

1 Like

Thanks alot for this! Is this available on any public domain for us to check?

Not sure why the delay in getting the approval.

Inox group forays into Solar modules manufacturing and OEM.

Looks like a desperate move to enter solar when they have not scaled up wind efficiently. Would love to be proven wrong.

1 Like

This is slightly contradictory to what management has been saying in concalls that solar is commoditized and wind is not yet, so not confident.

disc - invested and biased

This is inox gfl group investing in their private capacity through inox solar, a pvt company.

Will indirectly be helping other group companies in hybrid tenders bidding.

Inox wind’s EPC subsidiary resco would be materially impacted (positively) imv. Otherwise, it’s non material for inox wind as such.

2 Likes

Inox Group had their vision day on 2 dec, 24. This is applicable across GFL thread, Inox wind and Inox Green threads. Sharing relevant notes that correspond for this thread

Their presentation: https://www.bseindia.com/xml-data/corpfiling/AttachHis/a76d4539-16b1-4a20-ab68-d5260cd24b2c.pdf

For Inox Wind:

1. 3.5 GW order book.

2. Lot of IPPs have come up - good for sector - earlier only 2-3 used to develop - today 15-20 IPPs, PSUs are trying to develop their own projects.

3. Group foray in to Solar - as customers needs Hybrid and FDRE.

4. we have built up more than a 1 GW supply chain capability and we are now getting ready in a year time to go into a 2 GW supply chain capability.

5. DCR is going to come in a big way in a years time - geared up for that. Have less imports in our supply chain and be cost competitive be it internally with in the country or externally too.

6. we are very low on the OPEX and CAPEX- not looking too make capex - we have the supply chain, the tech - gives a hugeCF generation capabilities over next year to 2.

7. Raised 2200 cr at 25,000 Cr ($3B ) valuation and money has been pumped in to the company - deleveraging the balance sheet

8. Ratings upgraded from BBB to A+ and targeting AA - over time.

9. Successfully created a consortium with private sector banks.

10. ultimate vision of being 2 GW by FY27 - does not imply we stop at 2 GW - as the market moves to 10-12-15 GW we probably will be taking about 25 to 30% of the market share.

11. Foray in to Solar

-

- a. Not taking anything away from wind - already created a moat around wind biz - 2nd largest player in India - intend to scale fur there.

-

- b. Lot of demand for FDRE (Firm and Dispatchable Renewable Power) - dont want to loose the opportunity to competitors.

-

- c. Have come in late - module plant with 2.4 GW capacity will be live in Feb/Mar of 2025.

-

- d. Next 2 years - will set up 5 GW of mfg. capacity or cells and modules

-

- e. Capex cost will be almost 60% of the industry leaders capex cost.

-

- f. Many PSUs need hybrid tenders.

-

- g. Its not a me too policy - there is a thought around this - trying to create a moat around our Wind business.

-

Strategic foray in to important components like Crane - payback period is shorter than the payment period we have for the cranes.

-

Taking the tolling route for Transformers, electrical Control Systems - capture profitability but side step getting in to any non-core areas of our biz.

-

What is the moat per the mgmt:

- Only 2 players in India control the market

- Biggest moat is tech - anyone with 5000 cr to spend and 6 years to invest can obviously come in - but that is a lot of time. Inox spent 2 years, setting up 200 MW of wind and proving it out before they could start selling their WTG.we h

- Connectivity - we have access 5 GW of project site inventory- barring Adani and NTPC.

- Unlike solar where from 2 month of conceptualization of wanting to get into solar to going live with 2.4GW with in a few months is possible only in Solar but not in Wind. Entry barriers.

-

Everybody wants us to do turnkey - our Order book is 50% turnkey - main thing is not only setting up turbines but all the other things that come with it. If we have the ability to do turnkey we could have done 5 GW of turnkey - but we dont have the capability else our order book would have been 10 GW today.

-

We have 5.5 GW of Substation already built with 2.5 GW of wind ready for plug and play.

-

Why venture in to Solar? When wind participates in a lot of tenders right to supply turbines people want hybrid and FDRE projects so they come and say - please join with some solar guys and deliver- I’m not going to with someone else - as he does not have balance sheet. If he comes to halt, I will be at a stand still on that tender - I am not going to give bank guarntees to him - and we saw a lot of that and continuously increasing so we said how do we play this market so he said let’s control our own modules right and then because ALCM is coming in the cell it has to be controlled by you - we said we control the entire solar piece that’s how we got it - second our Private IPP play which is setting about 3 GW is doing, 1500 solar 1500 wind - so it’s not married to wind because when you supply under C&I your job is to maximize power supply - not your wind or solar maximized - so we have an internal requirement of 1500 MW of solar in the next 3 years - so if you put our tenders & observe - we have a GW of book every year already - the largest/ second largest/third largest is not even doing a GW - the largest is exporting those are short-term opportunities we are not looking at that.

Resco Global:

- Customers like the value add of bringing solutions like Crane services to the table in addition to the last 14 years experience of EPC wind turnkey solutions.

- 5 GW of project inventory

- 2 GW is plug and play infra available

- 350 cr raised through primary issue

IGREL renewables

- will leverage here - at competitive rates as the biz is capital intensive. 80:20 ratio - only company that might debt among all the group of companies. No inter corporate guarantees or interdependencies for finance.

- Privately owned by promoters - 3 GW of Wind and Solar hybrid capacity over next 2-3 years

- Ordered 750 MW of wind and 250 MW of Solar - in addition to this 150 MW is currently operational

- PPAs already signed at very competitive rates.

any mistakes above are truly mine.

5 Likes

Initially I also thought this was for Inox wind and this was becoming a case of diworsification. However considering it is via a separate entity, overall this feels very positive for the group and hence Inox wind. I hope there won’t be any investments by Inox wind into the said entity until they have extra cash

1 Like

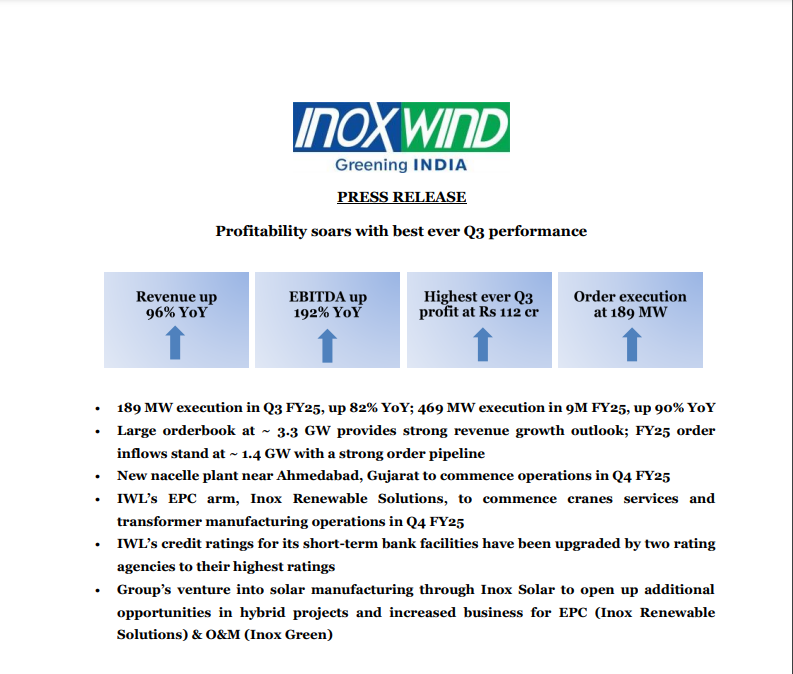

Best ever Q3 performance!

3.3GW orderbook with inflows of 1.4GW

Management is confident is getting bigger orders

4 Likes

Rating outlook revised to ‘Positive’; Ratings Reaffirmed; debt instruments withdrawn :

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/InoxWindLimited_February%2028_%202025_RR_364378.html

1 Like

Is there any update on merger?