I understand from the article that the share swap ratio/proposal is applicable only for promoters and large institutional investors who infused capital into the co’ at various points in the recent past. The same would not be applicable to Retail Investors.

Does anyone know what is the case for retails investors? Or am i reading/understanding this wrongly? By the way, the IWEL shares also hitting upper ckts recently. Not sure if there will be any discount for IWL by the time it actually merges or if there will any premium is being paid by the investors of IWEL.

Mr. Devansh Jain’s recent interview where he shares tranaformation journey and way forward for Inox wind…

Good discussion. Must watch.

● Windpower is not an industry in which you can overnight invest in and come in. It’s a complex supply chain. Certification, design, testing, licence, credibility ( of turbine ) takes atleast 3 years to build.So, its 4-5 years journey before Anybody else comes in and takes market share.

● Foreign MNCs can’t compete with our cost structure. Inox wind has lowest cost structure in Wind industry.

● If FY 26 is 7-8 GW market, then we are priming ourself to be

1.5 - 2 GW player.

● planning to make inox green 10 GW O&M company (500 Cr. Ebitda)

● We can increase capacity within 8-9 months, if required.

That is fine but this is quite important to know. It is not like Suzlon and Inox can overnight decide to do these kind of big turbines (15 MW). It will take years of R&D and certifications. Hence I didn’t think the post was relevant in this thread. Happy to be corrected.

In Earlier interviews Inox Wind’s Devansh Jain said, he may not be looking for Offshore Wind as they have enough work in onshore Projects… They are focusing on profitability, Cash flow generation but not focusing on exports or offahore wind Projects

In interviews management mentioned that, they are trying for inorganic growth also in O&M…so 6GW for Inox green may not translate in to similar growth for Inox wind

It is kind of a puzzler. Even DII FII stake has been increasing in Inox wind but not IWEL. The only explanation seems like IWEL having less liquidity. So while a fund can accumulate slowly, they sure can’t exit in a panic.

~ order book of 2.6GW with large pipeline (if LOI of adani green is incuded then OB will be 3.1GW)

~ Current Capacity > 2.5GW (Sufficient land bank to install ~5000 MW capacity)

~ Owns 61% in inox green with Portfolio 3.2GW (Targeting to reach 6 GW portfolio by FY26)

Just beginning of the massive growth journey.

In India total current capacity : 45GW and plan is to add another 100GW over the next decade.

Current orderbook 2600MW.

About 350MW is for 2MW and rest is for 3.3MW.

Will be net debt free by H1 next year.

Interest bearing debt is 450-500cr.

Interest cost will be 30-35cr from Q4 excluding one off charges.

Even these 30crs will become zero in 3 quarters.

Signed agreement for 4MW wind turbines in India, will be commercially available in 2-3 years.

Company is gearing up for 1000MW annual execution.

Numbers will be significantly larger in FY25 and FY26 than the guidance.

Capacity is 2.5GW no need to expand unless we get closer to that number.

Focus is on profitability, historically have been 14-15% EBIT business barring FY17-23 and aiming to get there from FY25.

Expecting to get approval from NCLT in next 2-3 quarters for IWEL merger.

Please ignore any typos and points which I might have missed. Thanks.

Disclosure : Invested

We may have to wait for commentary from management but may not have impact on top/bottom line numbers in the near future as management said earlier they focus on the cash flow, also no wind players bid aggressively for projects as all the players have plenty of projects. Earlier (2017-2020/21) many companies bid aggressively since many players want to liquidate as they want to moved out/exit the business.

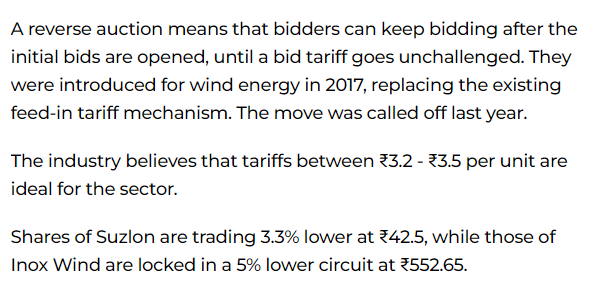

So for the benefit of everybody I would breifely explain the two type of auction and then maybe share my view, just to let everybody now I am sharing opinion which might not be factual so please verify.

So currently the closed envelope auctions are being followed so what happens is every body bids privately and nobody knows what others have bid. It is like suzlon sends their bid in a closed envelope to SECI.

Since currently the demand is very high, every body is bidding higher and auctions are going half subscribed + prices are increasing.

Now think about it this way, government is burning their money so that OEM can make more profit. I also think this way government has an X target of green energy which is very critical, so they want to reach there regardless of the composition. If wind is doing good they will allocate more capital to wind if solar is doing good they will allocate more capital there.

This is one of the auction from last year out of 1.2GW only 600MW got qualified, so the problem is real, and government will definitely try to find a solution to it

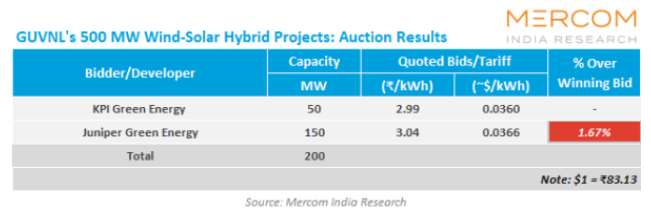

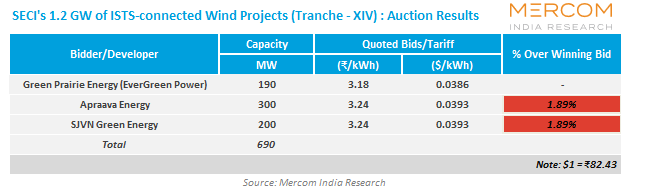

Here I posted a real reverse bidding example, just go through the two images in the beginning of the post. So everybody can see what others are bidding, you bid once, then you rebind, so the competition becomes intense and everybody has FOMO to get the project.

This was the biggest reason for the underperformance of wind industry post 2016-17

@Nafas_Muhammad you made a valid point, but post 2025 we will have the ISTS cost coming and will increase slowly, so the retail market right now is in a hurry to complete their projects prior to 2025, hece you can see good composition of retail in wind players order book

Another major positive from 2016 is debt for wind OEM

But I have a theory government has to do good capital allocation so till now their focus was on wind so the demand was huge but if solar does good they can shift their focus, like initially they can do more of hybrid projects and then maybe once storage cost is low they can even stop hybrid. Anyway if government does more hybrid that mean standalone projects would be decreasing.

This is from an article today, so another way of thinking is why would government want to put this industry again into trouble after they have put so much effort on reviving it.

Quite confusing, just check the risk reward of wind right now and take a call

Suzlon does not participate in bidding with SECI. Power producer players do that and they in turn reach out to companies like Suzlon, Inox etc for setting up the wind energy turbine and infrastructure.

If the mandate from Govt is indeed to bring back reverse auction then it can in theory result in many more power producer players jumping in with unviable bids that then do not get converted into actual on-ground infrastructure setup which in turn means Suzlon, Inox etc may not get orders commensurate to the bids awarded by SECI.

Rest of your response content is spot on (as always)!

I exited Suzlon today and Inox a few weeks earlier. Whether that purported letter is true or rumour, given the sky high valuations (both for the market and wind turbine companies in particular), the sentiment damage has been done. Unless we get clear clarification from Govt denying the letter and its content or some major positive news comes in, these shares will continue to trade in a range. Might play upper circuit/lower circuit game for some time. To make any more substantial gains (like doubling from this price point), we need a fresh gush of liquidity to come in, which looks unlikely in short run given that election overhang is also there.

I hope I am wrong in my thought process, but past experience makes me think otherwise! Hence exited for now (was painful to let go) to protect the profits.