In general, Goverment dont think about taking short term benifit from a sector. ( unless it is politically motivated/ election policy, and this doesnt look like one of them ). They always have a broader perspective of their policies. Weather those policies succeed or not is a different subject altogather.

ISTS is till 25, but we dont know, if thats the end to that or govt. gives extension to it.

World is changing at a rapid pace now a days, and we may get a surprise for the sector…

Improvement in the balance sheet is real & only data we have & is visible in certain manufacturers of windmill. ( that too since lat 2-3 years ).

2.Orderbook is rising for sector and we will have to keep close eye on it from sector perspective. Thisbis just first real year from that perspective.( another data that we have at the moment ).

All in all, I personally don’t think that its just a 1.5 year story ( as it will take atleast 1.5/2 years to commission wind mills of such large INITIAL ORDERS )

This sector is like dead/ doesnt exist for investor community. Just for example: in last concall of inox wind: It just lasted 24 minutes and no analyst question / interest from analyst community.

Having said that I will assess results/ other aspects on half yearly basis…

Lets keep learning and share our learnings about this sector…All the best.

Was wondering if there is another way to play this sector via a pick-and-shovel investing. For e.g. Sanghvi Movers caters to this sector. Are there any other listed co’s to play this theme ?

A very interesting and insightful blog on tailwinds and hiccups on Wind Energy Industry. I don’t think this has been shared here yet, so just sharing the link.

@manhar any comments on the Q1 results. It has turned EBITDA positive for first time in five years. With debt repayment, its matter of time that they turn PAT positive.

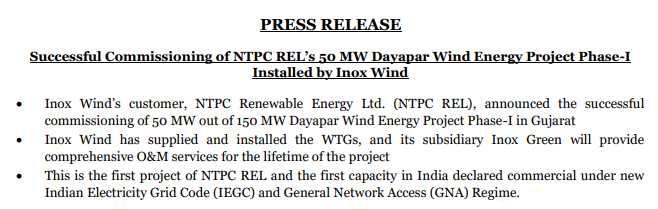

2… They still have 50MW of nani virani to be sold and they have been executing a 150MW NTPC order since august 2022 and it is still under execution so does the recognition happens after 100% execution or some other way. If it happens after 100% then this should reflect in Q2 or max Q3 this is like approx. 700cr.

As of now I can see this 200MW definitely coming up in Q2 or Q3. Now form H2 I have higher expectation and next quarter is monsoon season so I don’t have high expectation for Q2 as well. It would be grate if this 150MW NTPC comes up in Q2.

After con call I will have better understanding and as of now I am confident of them at least doing 2000cr.

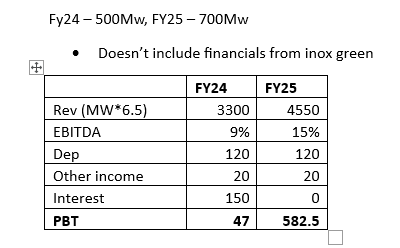

Do you have any fair valuation estimation for Inox Wind in terms of market cap? The real numbers will start from FY25 onwards and continue for next 3-4 years.

500cr block deal happening tomorrow…promoters are selling…Would be very interesting to see who is going to buy…A renowned fund entry will be a very good sign!!!

Reliance AGM announcement of foray into wind energy is a material risk for wind turbine maufacturers.

Apart from tech collaboration, reliance wants to manufacture at scale carbon fibre, which is used in making wind bades

So finally NTPC 50MW has been commissioned this is close to 220cr to 250cr of revenue ( I think this should reflect in Q3)

On one part of the presentation they say that term sheet has been signed so revenue form this should also come up in Q3 but they also say that 50MW SPV has been divested for a consideration of 290cr, so I am confused like if this is recognized or not or there are 2 50MW SPV.

If the 290cr above is yet to be received then next quarter we can see 500cr of revenue, plus they will supply 3.3MW from Q3

For H2 1000cr revenue is now visible to me with better clarity, For Q4 if they can complete the 100MW balance NTPC that would itself be 450cr to 500cr of revenue and on top of the the O&M revenue would add. This year they would execute 350MW to 400MW and their guidance was of 500MW

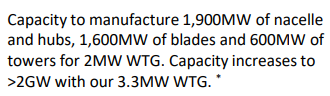

Next year they would only do 3.3MW, so now their capacity is 2GW turbine and 1.6GW blades, So now in H2 I expect them to win some 300MW of order , 1000cr of revenue and debt free

From the day I sold 50% of my Suzlon position and bought INOX ,suzlon has gone up by 120% and inox 40%, I expect INOX to catch up now, lets see

I watched the last few interviews given by Devansh Jain to media houses. One thing that stood out was that he never fails to stress the anticipated growth in the ‘next couple of quarters.’

On one hand, he sounds extremely optimistic about the sector; on the other, he places an overemphasis on just a quarter or two.

Sure, order book visibility will emerge with time, but I just wanted to check with others if I’m missing something. Perhaps I’m reading too much between the lines.

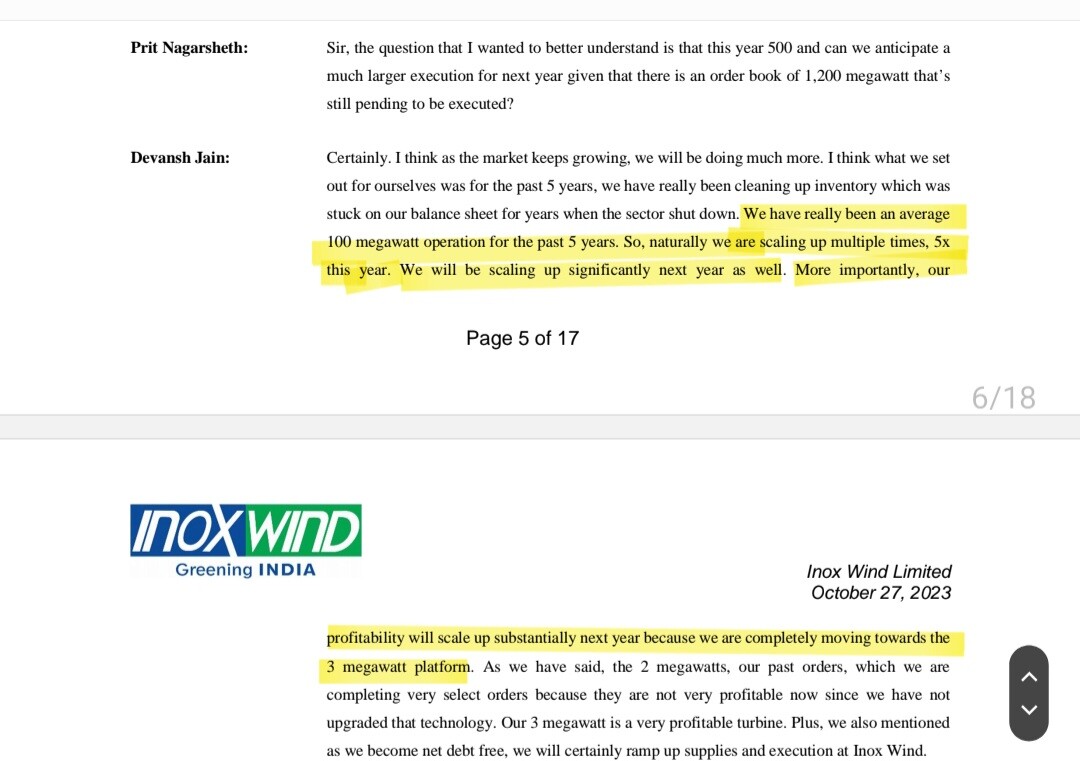

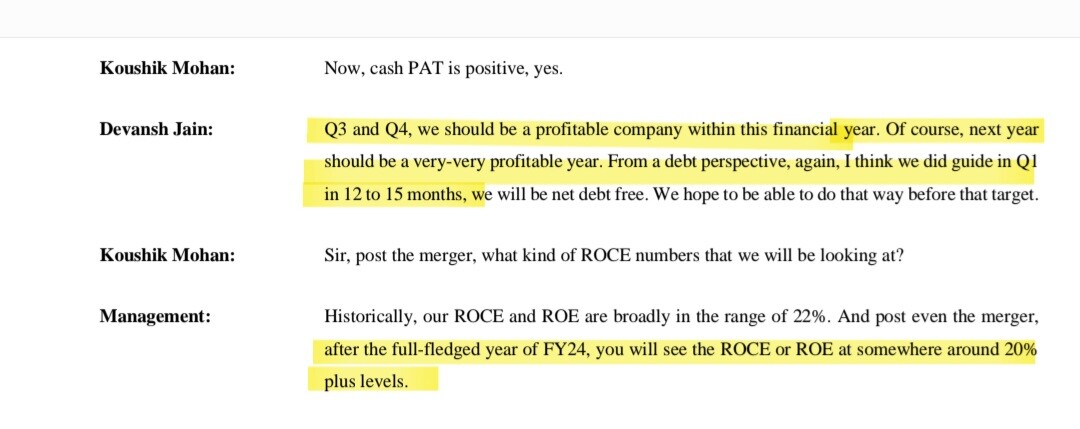

Here Mr. Devansh Jain says that next fy should be very very profitable year, ROE/ ROCE to be at 20% & company should be net debt free in 12- 15 months.

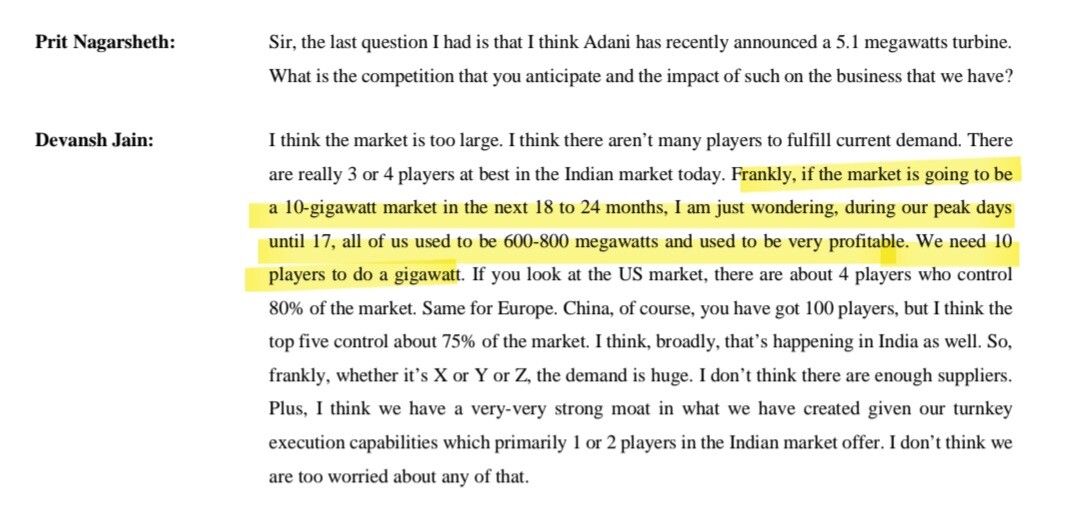

Here, company says that if it is going to be 10 GW market ( IN THE NEXT 18-24 MONTHS ), then we need many big players to execute this projects. And he also says that “In the peak days in past, all players used to be very profitable”

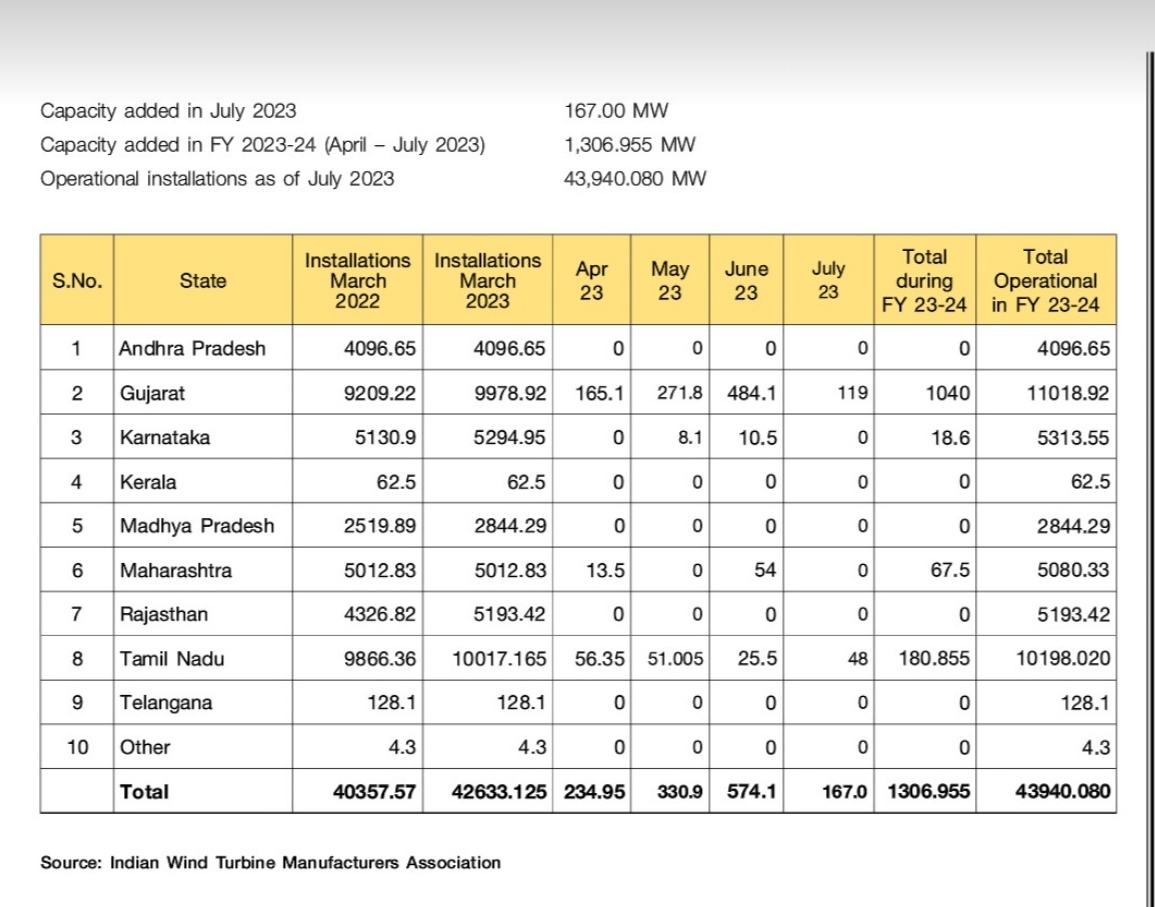

Govt. has come out with a fresh policy for repowering old wind mills below 2MW capacity. The compensation under the scheme is detailed Page 8 onwards. They want to target 25GW worth of old wind mills under this policy. If even 50% of the capacity comes forward for repowering, that can be a great further demand driver for Wind OEMs.

There is a good arbitrage opportunity (around 38%) available between the merger of Inox Wind (IWL) and IWEL (Inox Wind Energy Limited).

The Board has approved swap ratios for the proposed amalgamation as below: - 158 equity shares of face value of Rs. 10/- per share of IWL to be issued for every 10 equity shares of face value of Rs. 10/- per share of IWEL.

The CMP of IWL is around Rs. 394 which works out to Rs. 6225 per share of IWEL.

IWEL is currently trading at 4480 (put in t2t few days back and hence the volumes are low).

The rationale for this merger is the consolidation of wind energy business and streamlining of group structure and operations. The appointed date for the amalgamation is set as July 1, 2023.

Already 4 months passed since the board approved merger. So the approval might be around the corner.

Now the math is 125% Suzlon and 180% INOX, my ultimate goal of selling Suzlon and buying INOX has worked out pretty well

Demand is not a problem at all , total India capacity is like 10GW to 12GW in wind and central government yearly auction is itself 8GW per year on top of this we have demand from state, retail, PSU. The life of a wind mill is like 20yrs and what these guys are doing in repowering is extending the life by 5yrs, repowering is a headache nobody want to do, lets see.

The moment you see any wind player doing capex or any activity which increases the debt that would be the best time to sell them. My take can be wrong