Hi guys,

I think we need to understand what valuations suzlon is getting to evaluate the risk reward.

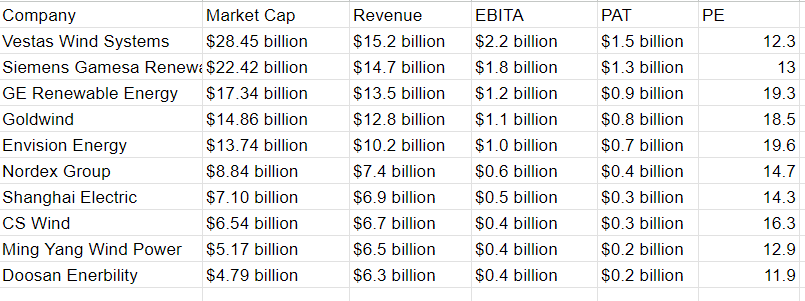

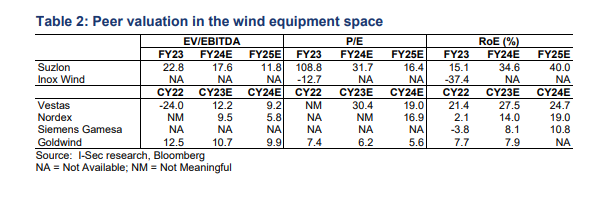

Global Players valuations

Please note this entire thing is from Brad so there might be accuracy issues but the broad picture is visible. The entire data is for 2022.

This is form ICICI so a more credible source and we have 4 international wind companies covered here. we can see that vestas and nordex are being valued at a PE of 16 to 19 for CY24E .

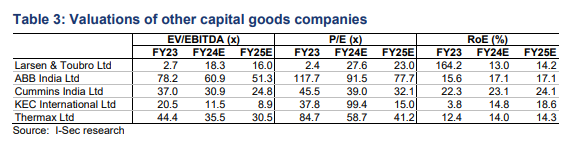

Valuations of some of the capital goods companies

.

.

Current valuation of suzlon

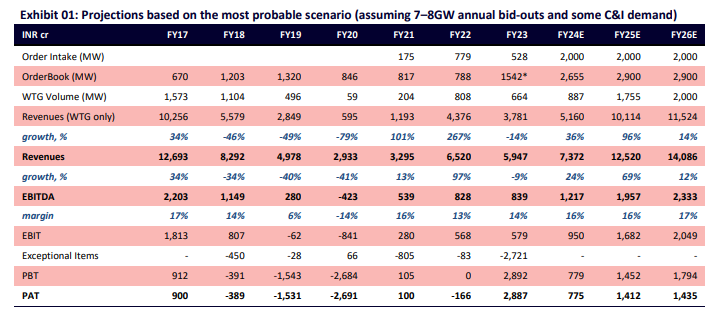

I think FY25 will be the peak for wind. I have explained this in suzlon thread and little bit here as well so after FY25 we wont have growth projections like we have right now.

If suzlon does 2GW in FY25 (doubtful) we can expected an EPS of 1.14 and the based on FY25E current PE is 17.5 times.

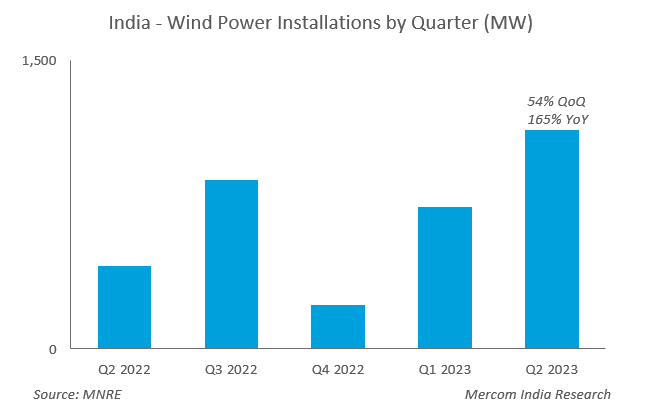

The current run rate is 4GW and I think we would not cross 5GW run rate. Please see the lates auction of 1.2GW where only some 600MW got executed so I believe that we would not execute more than 60% of what is tendered. So if 8GW is tendered each year execution will be of 5GW approx.

If suzlon maintains 30% so they would execute 1.5GW. If the do 1.5GW then they are trading at 24times PE.

Base on all the valuations shared above I don’t think players in this space deserve a PE of more than 20 to 25 times. So suzlon is already at these valuations and please note this is 2 years forward so there is execution risk.

He has take a big bet on it. So I think there is still some juice left but the risk reward is definitely not favorable.

My decision and how I am playing it.

- I am covering wind since December 2022 and I have bought suzlon @8 rs. I have exited 45% of my position form suzlon at 15rs and invested the entire thing on INOX. I think INOX has its own problems (I have written on INOX thread please read it) but the RR is favorable.

I think Inox is at 12 to 15 times FY24 earnings and currently Suzlon is getting 20 to 25 times FY25 earnings.

Suzlon is a technical hold for me because I don’t think any body in this industry deserves anything above 30 times. Even at 24 times it looks expensive.

Thankyou