A interesting read for the weekend ![]()

According to BSE filings, there was supposed to be an analyst meeting with Morgan Stanley on 20th July. How can we see the details discussed ?

Hollywood is delaying releases of movies, will Bollywood do the same???

I think the current prices in both INOX and PVR are unsustainable. Reason being

- COVID19 is a watershed moment in the history of human lives. It will induce definitive changes in consumer preferences and behaviors in ways in which we cannot imagine now. Just because the lock down gets over doesn’t mean the people start going over to malls or theatres. No one knows how this behaviour will affect the patterns of entertainment consumption in the future and when the things are so uncertain there is no way a company operating on this theme can get even a “Bad” valuation. The valuations may turn “Ugly” in the event of such uncertainty.

- Theatres dont own the product and with the sporadic lockdowns in different parts of the country and world, it is just not possible for filmmakers to realistically shoot a film. A film set has >100 people at a time and the right now the lockdowns are not uniform which means that maybe the shooting can happen in one place but for the next scene the shooting is not possible without compromising on something. This will delay all FY20 and beyond projects which are already hearing. Some projects may just die owing to financial constraint or some projects may be modified to suit a direct OTT premier. If this is indeed the case then there is a product shortage for INOX or PVR for atleast the next 1.5 years.

- Force Majeure is going to have a major financial impact on the owners of the malls/theatre space. While 2-3 months of the clause is okay but if the clause stays for the next 4-5 months I’m sure the real estate owner is going to be in a major financial soup. Who knows what will happen if the owner goes bankrupt and needs to liquidate the mall building to meet liabilities. What happens to INOX/PVR then?

Right now I feel the market is just making plain assumption that once things become normal, everything will become normal. But in an uncertain business and health environment we are looking at 2 potentially bankrupt businesses in INOX and PVR. They can raise all the money they want but the the changes that are happening are not only superficial economics but major behavioral changes.

In this regards, I feel that an erosion of 80%-90% of business value (compared to 50% now from peak) is very much possible.

12 Likes

A meeting of the Board of Directors of the Company is

scheduled to be held on Wednesday, 5th August, 2020, inter alia:

- To consider and approve Unaudited Standalone and Consolidated Financial Results of the Company

for the quarter ended 30th June, 2020;- To consider a proposal for obtaining an enabling approval from the shareholders at the forthcoming

Annual General Meeting of the Company regarding the proposal of raising of funds through issue of

securities either by way of a public issue or by way of rights issue or by way of a private placement

(including but not limited through a qualified institutional placement) in accordance with the

provisions of the applicable law.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2e18aa0f-9022-4148-abfb-36c02d784ff8.pdf

So a rights issue like PVR might be on the anvil.

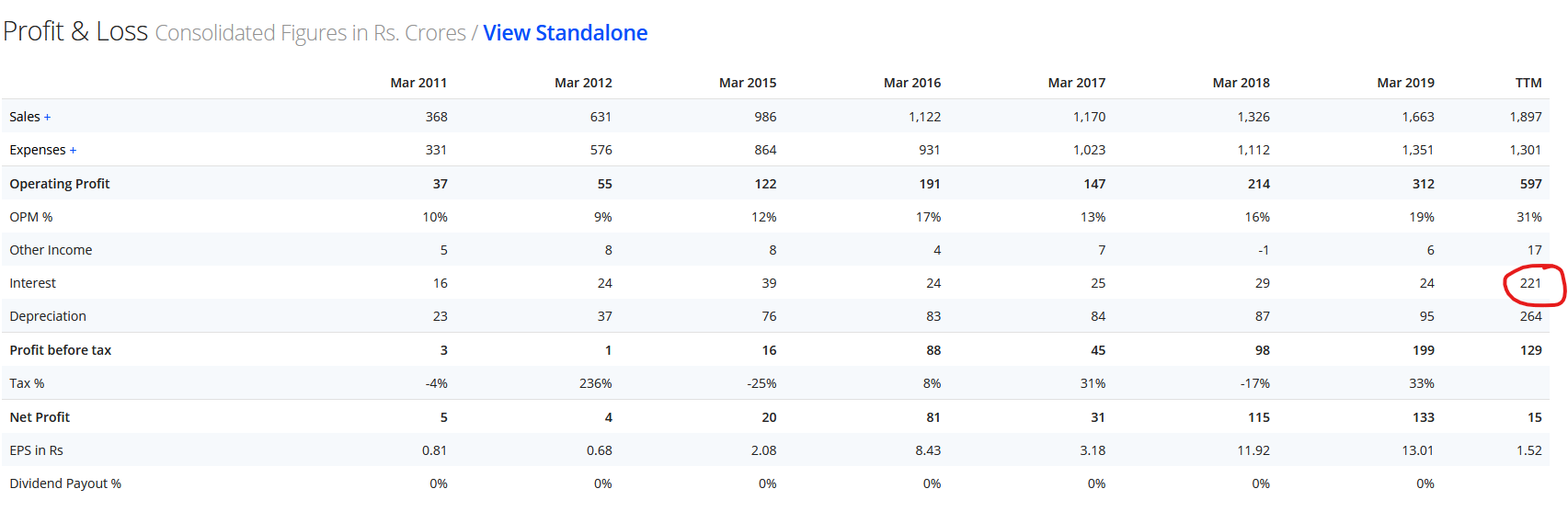

Can someone help me understand why Screener is reporting a very high interest expense of 221 cr in FY2020? I do not see any new borrowings by the company.

2 Likes

Company liquidated all its holding in INOX leisure through its trust entity. In the process, 101.36 cr. was raised which will aid liquidity for the company.

The liquidation is actually surprising considering that the ceo did not indicate any active consideration of this means during the investor call. This ws one of the possible ways but the management were looking at raising only 30-40 crores in addition to the existing cash balance.

This caught me in surprise

2 Likes

1 Like

It won’t be easy to get the crowd back unless there is a block buster release

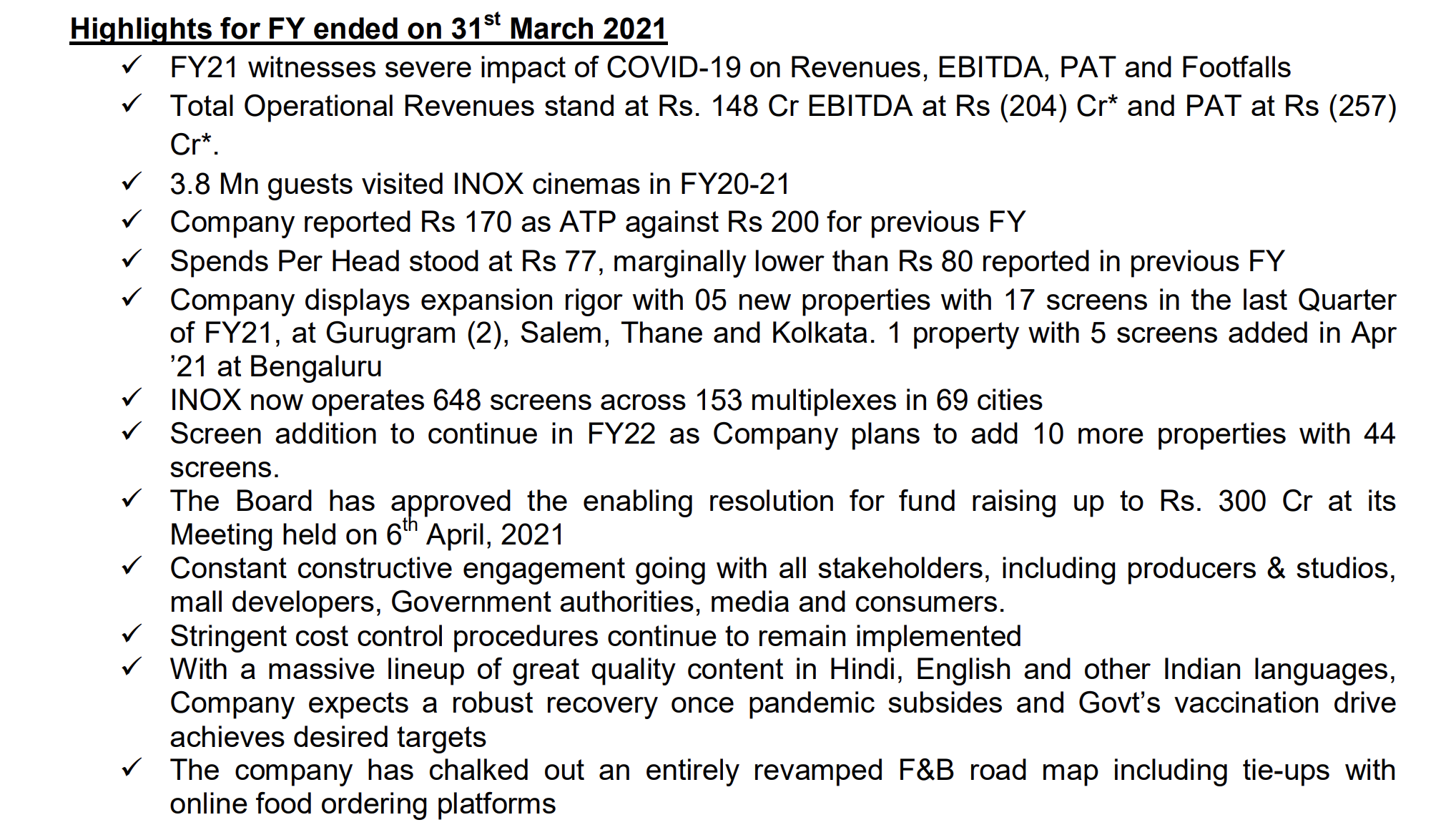

Another bad quarter for INOX, result summary is below

Here are the detailed business metrics over the last 12 years. One silver lining is spend per head deteriorated marginally in FY21 (77 vs 80 in FY20). Average ticket prices went down from 200 in FY20 to 170 in FY21.

| FY09 | FY10 | FY11 | FY12 | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY15-20 Incr | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Screen count | 91.00 | 119.00 | 239.00 | 257.00 | 279.00 | 310.00 | 377.00 | 420.00 | 476.00 | 492.00 | 574.00 | 626.00 | 648.00 | 10.67% |

| Properties | 26.00 | 32.00 | 63.00 | 68.00 | 72.00 | 79.00 | 97.00 | 107.00 | 119.00 | 123.00 | 139.00 | 147.00 | 153.00 | 8.67% |

| Number of seats | 99’429.00 | 109’406.00 | 119’395.00 | 121’573.00 | 135’586.00 | 144’467.00 | 147’436.00 | 7.76% | ||||||

| Average occupancy | 25% | 28% | 28% | 25% | 29% | 28% | 26% | 28% | 28% | 8% | 2.29% | |||

| Average ticket price | 156.00 | 160.00 | 156.00 | 164.00 | 170.00 | 178.00 | 193.00 | 197.00 | 200.00 | 170.00 | 4.05% | |||

| Footfalls (cr.) | 3.90 | 4.30 | 5.34 | 5.37 | 5.33 | 6.25 | 6.60 | 0.38 | 8.95% | |||||

| Net box office collections (cr.) | 490.50 | 551.60 | 712.80 | 748.10 | 802.20 | 975.00 | 1’105.00 | 54.00 | 14.91% | |||||

| Food and beverages (cr.) | 141.76 | 162.30 | 191.00 | 265.60 | 284.10 | 306.00 | 436.00 | 497.00 | 28.00 | 21.08% | ||||

| Advertising (cr.) | 32.44 | 49.50 | 81.50 | 91.00 | 96.20 | 138.90 | 177.00 | 179.00 | 3.00 | 17.04% | ||||

| Others (cr.) | 60.40 | 71.20 | 91.10 | 92.30 | 101.00 | 104.00 | 134.00 | 63.00 | 13.48% | |||||

| Spends per head (Rs.) | 41.00 | 44.00 | 47.00 | 49.00 | 55.00 | 58.00 | 62.00 | 66.00 | 74.00 | 80.00 | 77.00 | 7.78% |

Disclosure: Invested (position size here)

2 Likes

This could be amazing if it happens. No crash crunch, will help establish boundary between OTT and multiplexes.

edit: https://www.bseindia.com/xml-data/corpfiling/AttachLive/449b7135-1e91-4b22-af10-678ac03796ce.pdf

Inox clarified that there was no such discussion between inox and amazon.

barring another severe covid wave(s), the cinema business seems to be on track to normalcy. It seems the current market price already has priced in the same.

I feel the next opportunity to create alpha in this space will come from the non movie exhibition revenue opportunities - F&B, gaming etc; The bid to establish movie theatres as something more than just a movie watching destination.

1 Like

The merger has been confirmed By Inox now.

• Share Exchange Ratio of 3 shares of PVR for 10 shares of INOX

Share swap ratio is offering a 15% arbitrage opportunity for Inox shareholders at CMP.

I believe that’s a minimum premium that Inox deserves due to the better quality of balance sheet and minimal debt.

As an Inox shareholder, I was kind of hopeful that Inox could get premium multiples over PVR in the next couple of years with strong expected demand post the Pandemic and great balance sheet strength.

Overall, I think it’s a decent outcome for Inox shareholders as PVR is undoubtedly the no.1 cinema brand and the share swap is also giving the additional arbitrage due to Inox’s balance sheet strength.

The amalgamation is subject to the approval of the shareholders of PVR and INOX respectively, stock exchanges, SEBI, and such other regulatory approvals as may be required.

I wonder whether CCI would approve the merger as the merged entity will be a clear leader with 1527 screens compared to Cinepolis with 400 screens.

1 Like